|

Fast Facts

|

|

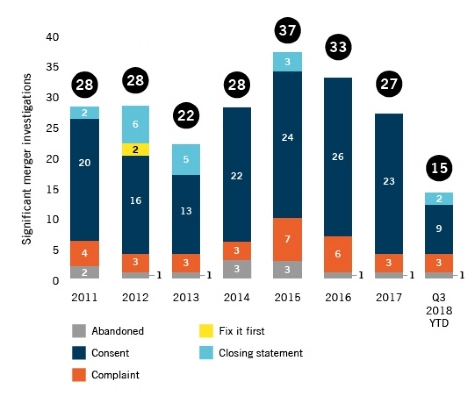

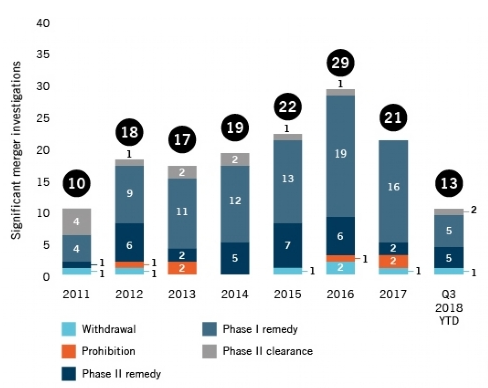

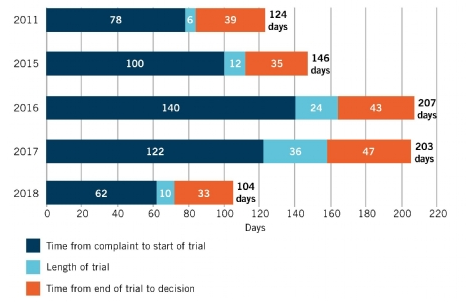

Citing findings from the Dechert Antitrust Merger Investigation Timing Tracker (DAMITT) that have demonstrated a marked increase in the duration of significant merger investigations in recent years, DOJ Assistant Attorney General Makan Delrahim and FTC Chairman Joseph Simons recently announced reforms to the U.S. antitrust merger review process. Beyond these process reforms, which appear to be significant, there is little to report on Q3 2018 significant antitrust merger investigations in either the United States or European Union, but there were some intriguing developments in U.S. merger litigation. Through the first three quarters of 2018, the number of significant investigations is down compared to 2017 in both the U.S. and EU, with Q3 2018 representing a particularly slow quarter. In the U.S., only two significant investigations concluded during the quarter, averaging only 6.9 months from announcement to clearance — the lowest average for any quarter in the past four years. In the EU, three significant investigations — all Phase II proceedings — concluded during the quarter. These three EU cases averaged 13.5 months from announcement to clearance, which is faster than the 15.1-month average for 2017. Two U.S. FTC merger litigations filed in 2018 (Wilhelmsen/Drew Marine and Tronox/Cristal) were concluded during Q3 2018, both resulting in preliminary injunctions blocking proposed transactions. These two litigations were decided an average of 3.5 months after the filing of the district court complaint, a pace nearly half as long as the almost seven-month average observed for complaints filed during 2016 and 2017. However, the Tronox case presented a unique procedural posture that contributed to the faster pace and may not be representative of the duration of future litigations, which is likely to remain closer to the 5-7 month range observed in the Wilhelmsen litigation and in recent years.

|