In response to Proposition 111, which amends Colorado's Deferred Deposit Loan Act by capping the annual percentage rate for deferred deposit loans and payday loans at 36% effective February 1, 2019, creditors currently offering loans under the DDLA have expressed an interest in offering loans attracting the alternative charges allowed by Colo. Rev. Stat. § 5-2-214. On January 4, 2019, the Administrator of the Colorado Uniform Consumer Credit Code published a memo providing introductory guidance on the ability to charge the alternative loan charges.

Colo. Rev. Stat. § 5-2-214 allows the following alternative loan charges:

- An acquisition charge for making the original loan, not to exceed 10% of the amount financed.

- An acquisition charge for making any refinanced loan, not to exceed 7.5% of the amount financed.

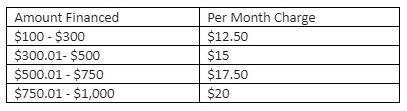

- A monthly installment account handling charge, not to exceed the following amounts:

- Delinquency charges as provided for in Colo. Rev. Stat. § 5-2-203.

- Reasonable attorney fees provided for in Colo. Rev. Stat. § 5-5-112.

- Dishonored check charges as provided for in Colo. Rev. Stat. § 5-2-202(1)(e)(II).

The alternative loan charges may be charged only if:

- The amount financed is $1,000 or less;

- The minimum loan term is 90 days, and the maximum loan term is 12 months;

- Installment payments are scheduled in substantially equal periodic intervals;

- The loan is unsecured (i.e., the creditor has not taken any collateral - including a post-dated check or certain ACH authorization - as security for the loan); and

- The creditor has not refinanced such a loan more than three times in one year.

Per the UCCC Administrator's memo, any ACH agreement must be voluntary and may not be a requirement of the loan. If the consumer voluntarily consents to scheduled ACH installment payments, that agreement must be revocable by the consumer at any time. An ACH payment authorization that allows for the acceleration of any loan payments is impermissible collateral.

Because the UCCC imposes other requirements that may impact a creditor's ability to attract the alternative loan charges (e.g., rebate requirements and prohibitions against minimum charges and unconscionable agreements), the UCCC Administrator advises creditors to review the UCCC and associated rules and consult with their own counsel before offering such alternative loans.

Prior Alert: Colorado Ballot Initiative to Cap Payday Loan APRs at 36%