The Taskforce on Innovation, Growth and Regulatory Reform (TIGRR) submitted its report on the UK’s approach to regulation after its withdrawal from the EU to the Prime Minister on 15 June 2021. TIGRR was commissioned by the Prime Minister in February 2021 to explore ways in which UK can reshape its approach to regulation and create new opportunities in light of Brexit. The report makes recommendations covering a new UK regulatory framework based on core principles of UK law as well as regulatory reforms in specific sectors. The Prime Minister has welcomed the report. The government will consider and respond to the report’s recommendations in due course.

A summary of the key reform recommendations relevant to financial services are set out below.

Financial services

1. Restore a common law principles based approach to financial services regulation

The report welcomes the work being carried out by HM Treasury in the Financial Services Framework (FRF) Review – see our blog post on the FRF here – and provides two examples of specific changes that could be made under this approach:

2. Deliver a regulatory framework that supports UK global leadership in FinTech and digitalisation of financial services infrastructure.

The Taskforce believes Fintech to be a core driver of UK economic growth and prosperity – in 2020, £4.1bn was invested into UK Fintech, more than the next five European countries combined. It recommends that the government ensures its policy and regulatory approach continues not only to protect consumers but also creates an enabling environment that encourages growth and competition.

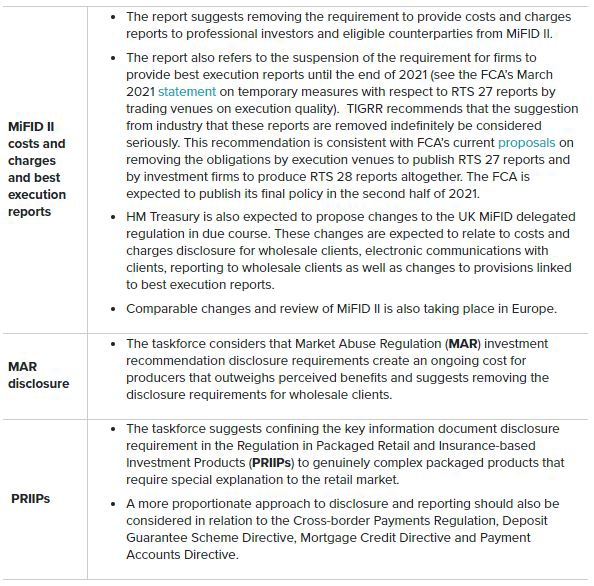

3. Amend disclosure and transparency requirements for financial services products to make them more proportionate and less burdensome.

The report finds many aspects of the EU’s transparency and disclosure regime for financial services to be onerous. To illustrate this, the report refers to MiFID II transparency and disclosure regime which are designed to capture data on all EU member state markets and is therefore disproportionate for the UK outside the EU. Disclosure requirements should be proportionate for business, incentivise bespoke information provision to consumers rather than excessive reports laid out in prescriptive templates.

Although reform of disclosure requirements is beyond the scope of the report given the extensiveness of a such a review, the report suggests certain topics as areas for potential changes.

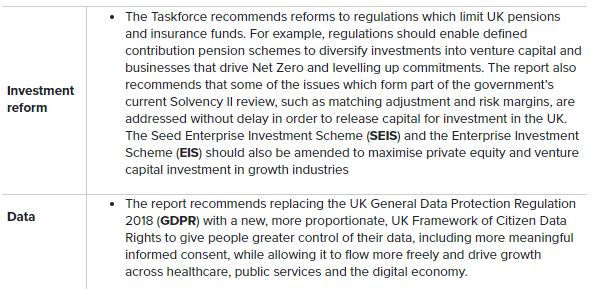

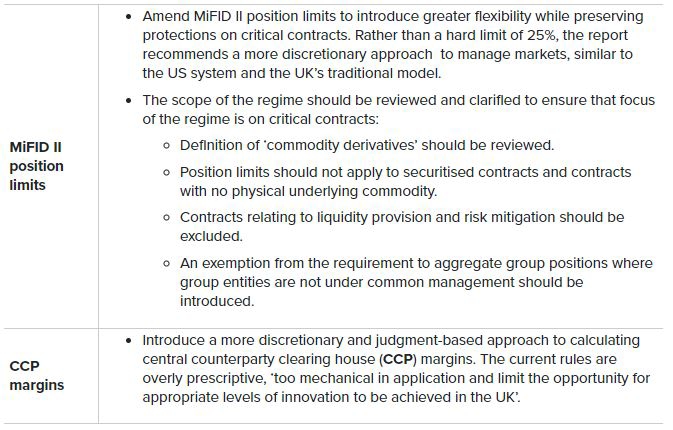

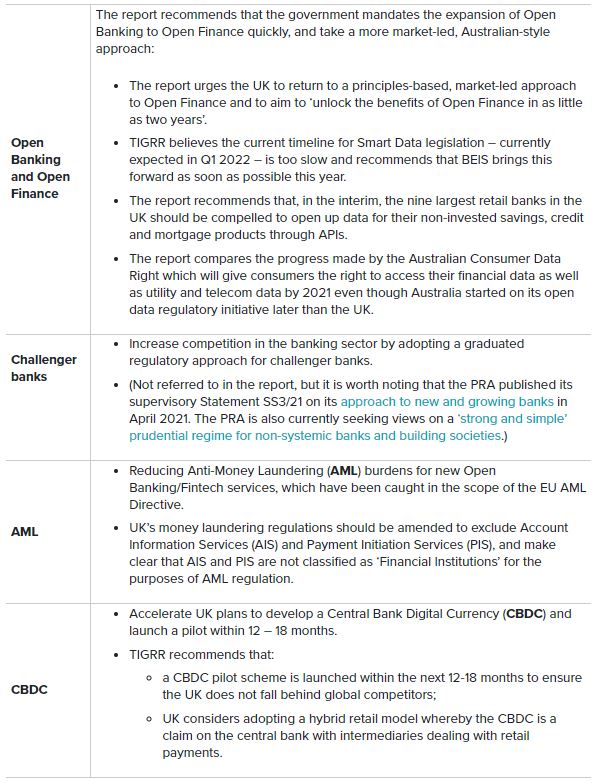

Other recommendations relevant to financial services