A. INTRODUCTION

Since 2004, Cyprus is a full Member State of the European Union. This fact, along with its good strategic location, highly skilled human capital, excellent infrastructure, reliable communications, relatively low cost of living, sound and stable legal system, warm climate and hospitality of its people, are some of the advantages which contribute to Cyprus’ continuous development as a competitive international financial, tourist, retirement and relocation centre.

The Government of Cyprus has for many years implemented policies to attract foreign investments and foreigners to Cyprus. One of the most important policies is the newly introduced notion of resident but not domicile which puts Cyprus in the map of jurisdictions that are considered ideal for HNWI to reside in.

We present herein below an outline of the main tax issues an individual wishing to relocate or retire in Cyprus will encounter.

This outline does not deal with the tax aspects applicable to legal person but refers only to physical persons. For relevant information on legal persons kindly refer to our publication, “Cyprus Tax Legislation on Companies (The Foreign Investors’ Approach)”.

B. TAXATION IN GENERAL

The Cyprus tax system may impose taxes only to tax residents of Cyprus or persons who have income from sources in Cyprus.

I. Tax Residents in Cyprus:

Tax resident of Cyprus, in the case of a physical person, means:

a. Any individual who resides in Cyprus for one or more periods which exceed in total 183 days in the financial year, or

b. Any individual who stays in Cyprus for at least 60 days in the year of assessment, provided that:

1) He/she is not tax resident in another country (i.e. does not spend more than 183 days in any other jurisdiction) 2) He /she maintains a permanent residence in Cyprus which can be owned or rented 3) He/she conducts any business or is employed in Cyprus or is a director in a Cyprus company as at the 31st of December in the year of assessment.

All Cyprus tax residents, as identified above, either Cypriots or foreign nationals, are taxed in Cyprus on their worldwide income accrued or derived from all sources in Cyprus and abroad.

A person who is a tax resident of Cyprus but his/her place of domicile is outside Cyprus can enjoy significant tax benefits as analysed in section D below.

A tax resident of Cyprus may be subject to the following type of taxes or deductions on income:

1) Income Tax (Analysed in Section C) 2) Special Defence Tax (Analysed in Section D) 3) Social Insurance Contributions (Analysed in Section E) 4) Contributions to the General Healthcare System (Analysed in Section F) 5) Capital Gains Tax (Analysed in Section G)

II. Non-Tax Residents in Cyprus:

Individuals who are not tax residents of Cyprus are taxed on income accrued or derived only from sources in Cyprus, if any.

C. INCOME TAX

Income tax is imposed on the chargeable income. Chargeable income includes the following types of income:

1) Employment Income 2) Benefits in Kind (for more information refer to our publication “The Taxation of Benefits in Kind in Cyprus”) 3) Deemed benefit of 9% per annum on the balance of any amount granted by a company (as a loan or any other financial facility) to its individual shareholders or directors or their spouses or relatives up to the second degree for non-business purposes. 4) Business Income (as a sole trader) 5) Royalty Income from Intellectual Property 6) Active Interest Income 7) Pension and Annuities 8) Rental Income from Property 9) Trading Goodwill

I. Obligation for preparation and submission of Audited Financial Statements by individuals:

Cyprus or Non Cyprus tax residents, who generate gross income in Cyprus from the carrying out of a business activity (i.e. having Business Income as sole traders) which equals or is in excess of EURO 70.000 per annum, are obliged to prepare and submit annual audited Financial Statements to the Tax Department and issue invoices and receipts in connection with the transactions and collections.

Cyprus or Non Cyprus tax residents, generating total gross income less than EURO 70.000 per annum, are not required to prepare and submit audited financial statements, but are obliged to maintain books and records.

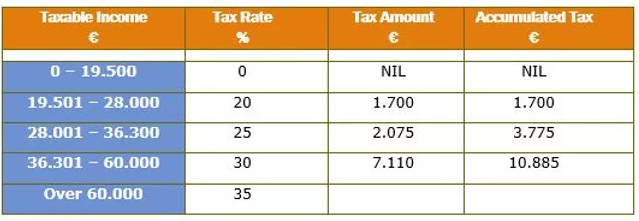

Individual Tax Rates:

The following tax rates apply for physical persons who are tax residents of Cyprus:

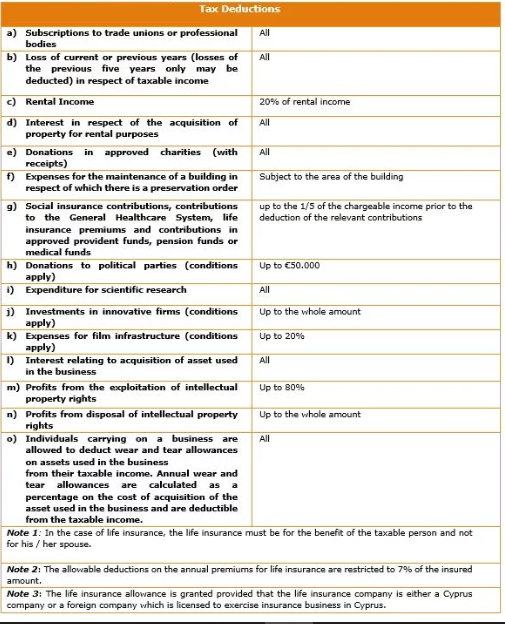

The law provides for some expenses to be deductible from a physical person’s taxable income. The list of such expenses can be found in Schedule 1 of this publication.

Further, there are some types of income which are exempted from taxation which can be found in Schedule 2 of this publication.

Tax credit relief is granted under conditions, if on a particular income, taxation has already been paid abroad provided that the taxpayer provides the tax authorities with the original tax receipts evidencing the payment of such foreign tax.

Special Taxation Treatment of specific types of Income

i) Cyprus Tax Residents

Pension income generated from abroad - Cyprus tax residents generating pension income from services rendered abroad are liable for 5% tax on the income exceeding €3.420 per annum. The taxpayer has the right to choose to be taxed either in accordance with the special treatment of taxation mentioned above, or under the individual income tax rates as indicated on the above table.

Individuals employed in the fund industry – Cyprus Tax resident employees who operates in the fund industry and generates variable remuneration connected to a carried interest, may be taxed at a flat rate of 8% on amounts constituting carried interest with a minimum tax liability of €10.000 per annum (conditions apply). Qualifying employees have the option to choose to be taxed under this special treatment of taxation on an annual basis for a 10-year period or otherwise to be taxed under the individual income tax rates as indicated in the above table.

ii) Non-Cyprus Tax Residents

Income generated from intellectual property rights – A non-Cyprus tax resident generating gross income arising from intellectual property rights or other similar income from sources within Cyprus, is subject to a 10% withholding tax (unless a tax treaty provides for a lower tax rate).

Profits of entertainers – The Gross income derived by an individual who is not resident in Cyprus from entertainment events (i.e. musical/theatrical performances, football clubs’ performances etc) executed in Cyprus and which does not arise from a permanent establishment in Cyprus, is subject to a 10% withholding tax (unless a tax treaty provides for a lower tax rate).

Income from Oil & Gas related activities – The Gross income derived by an individual who is not resident in Cyprus from Oil & Gas related activities carried out in Cyprus (i.e. exploration or exploitation of the continental shelf, subsoil or natural resources, installation and exploitation of pipelines etc) and which does not arise from a permanent establishment in Cyprus, is subject to tax at the rate of 5% (unless a tax treaty provides for a lower tax rate).

Income from technical assistance - The gross income derived by an individual who is not resident in Cyprus from technical assistance services provided in Cyprus is subject to a 10% withholding tax. The withholding tax does not apply if the services are provided by a permanent establishment in Cyprus.

D. SPECIAL DEFENCE CONTRIBUTION TAX (SDCT)

In 2015 the notion of Domicile was introduced into the Special Defence Contribution Tax. With this introduction Cyprus tax resident individuals are classified either as Resident and Domiciled in Cyprus or as Resident but not Domiciled in Cyprus. The term “Domiciled in Cyprus” is defined as an individual who has a Domicile of Origin, in accordance with the Wills and Succession Law, in Cyprus but it does not include:

1) An individual who has obtained and maintains a Domicile of Choice outside Cyprus in accordance with the Wills and Succession Law, provided that the individual was not a Cyprus tax resident for a period of 20 consecutive years preceding the tax year under examination.

2) An individual who has not been a Cyprus tax resident for a period of at least 20 consecutive years before the commencement of the law. A physical person who is considered as Cyprus tax resident as defined by the Income Tax Law for at least 17 years out of 20 years period preceding the year of assessment is considered as “Domiciled in Cyprus” for SDCT purposes and will therefore be subject to the relevant taxation if and when this condition will be met. In other words, the benefits granted to Resident but Non-Domiciled individuals can only be enjoyed for 17 years.

I. Cyprus “domiciled” tax resident individuals:

Such physical persons will be subject to SDCT. The tax rates are as follows:

1) Dividends 17%; 2) Passive interest 30%; 3) Trading Interest – Nil (this type of interest is subject to income tax at the above indicated rates mentioned in section C.); 4) Rental income 3% on the 75% of the total rental income; 5) Interest received by an individual from Government Savings Certificates, Government Bonds and Corporate Bonds 3%; 6) Interest earned by an approved provident fund 3%; 7) Interest earned by the Social Insurance fund 3%;

Tax credit relief is granted under conditions, if on the particular income, taxation has already been paid abroad provided that the taxpayer provides the tax authorities with the original tax receipts, as above.

II. Cyprus “non - domiciled” tax resident individuals:

Such physical persons will be EXEMPTED from Special Defence Tax. Therefore, dividend, passive interest and rental income received, is exempt from such taxation.

E. SOCIAL INSURANCE CONTRIBUTIONS

Employed and self-employed persons who obtain employment income in Cyprus, are subject to Social Insurance Contributions. The Social Insurance Contributions deducted from the emoluments of the employee/self-employed person comprises the following:

I. For Employees:

• Social Insurance at 8.3%

The Social Insurance Contributions are applicable on the amount of the annual gross employment income of the employee, up to a maximum annual insurable income of EUR 54.864, EUR 4.572 per month for monthly paid employees and EUR 1.055 per week for weekly paid employees.

The contributions are withheld by the employer on a monthly basis, and are paid on behalf of the employee to the Social Insurance Office, at the end of the following month in which the deduction is made.

II. For Self Employed persons:

• Social Insurance at 15.6%

The Social Insurance Contributions are applicable on the fixed insurable earnings, in accordance to the category of business income of the self-employed person, subject to a compulsory minimum and a maximum insurable income, as defined by the Social Insurance Office.

The self-employed person is responsible for the calculation and payment of the Social Insurance Contribution, directly to the Social Insurance Office, on a quarterly basis.

III. For the Employer:

The employer is liable to pay contributions for every employee on a monthly basis, to the Social Insurance Office, at the end of the following month in which the contribution relates to.

The contributions that an employer must pay for each employee, and the applicable rates are as follows:

• Social Insurance at 8.3% • Redundancy Fund at 1.2% • Industrial training Fund at 0.5% • Social Cohesion Fund at 2.0% • Central Holiday Fund at 8% (if not exempt)

The Contributions are applicable on the amount of the annual gross employment income of the employee, up to the maximum annual insurable income of EUR 54.864, except for contributions to the Social Cohesion Fund. The contributions to Social Cohesion Fund are applicable on the amount of the annual gross employment income.

The employer can get an exemption from the Central Holiday Fund, if he offers paid leave benefits.

F. CONTRIBUTIONS TO THE GENERAL HEALTHCARE SYSTEM

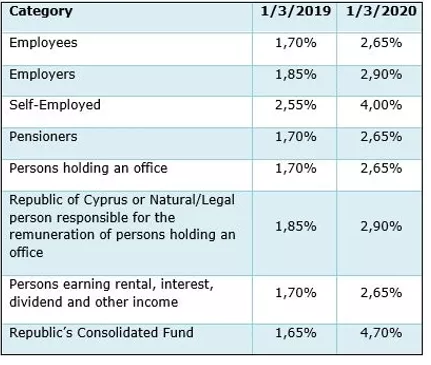

As from 1st of March 2019 individuals who obtain income in Cyprus, may have the obligation to contribute to the General Healthcare System (“GHS”), and benefit from the health care services provided.

Contributions are calculated and paid as a percentage on emoluments/pensions, as follows:

Contribution Threshold

The contributions will be deducted from the entire earnings of the individuals (including dividends, rental income, interest income) up to a maximum of EUR 180.000. For more information you may refer to our dedicated tax update on the matter.

G. CAPITAL GAINS TAX

There is a 20% tax on gains from the disposal of immovable property situated in Cyprus, including gains from the disposal of shares in non- listed companies which directly or indirectly own immovable property in Cyprus and derive at least 50% of their market value from such immovable property.

Disposal of shares of listed companies does not impose any capital gains tax even if the listed company owns immovable property in Cyprus.

The taxable gain is estimated taking into consideration various factors as it is specified in detail in the relevant Capital Gains Law.

Any profit made from the sale of immovable property abroad is not taxable in Cyprus. This means that residents of a country that does not impose capital gains tax to non-residents may benefit from selling property after immigrating to Cyprus and upon acquiring tax residency in Cyprus.

The following transactions are exempt from capital gains tax:

-

Transfers arising on death;

-

Gifts made from parent to child or between husband and wife or between relatives up to the third degree;

-

Gifts to a limited liability company where the company’s shareholders are members of the donor’s family and the shareholders continue to be members of the donor’s family for five years after the day of the transfer;

-

Gifts by a limited liability company to its shareholders, whose shareholders belong to the same family, provided such property was originally acquired by the company by way of donation/gift. The property must be kept by the donee for at least three years;

-

Gifts to charities and the Government;

-

Exchange or disposal under the Agricultural Land (Consolidation) Laws;

-

Exchange, provided the gain is used for the acquisition of new property. The gain derived from the exchange reduces the cost of the new property and the tax is paid when the latter is disposed;

-

Expropriations;

-

Transfer ownership or share transfers in the event of company reorganisations;

-

Transfer of property of a missing person under administration;

-

Transfer of ownership between spouses that their marriage has been dissolved by a court order or in case of transfer ownership between the same persons for the purpose of settling their property according to the Settlement of Property Relationships between Spouses Law;

Lifetime Exemptions:

Every physical person is eligible to receive lifetime exemptions when disposing immovable property in Cyprus. Lifetime exemptions are deducted from the chargeable capital gain, hence reduce the capital gains tax.

The lifetime exemptions available are as follows:

-

Sale of own residence EURO 85.430 (subject to conditions);

-

Sale of agriculture land by a farmer EURO 25.629 (subject to conditions);

-

Other sales EURO 17.086;

The lifetime exemptions are granted over the lifetime of the physical person until fully exhausted. The combination of the lifetime exemptions cannot exceed the amount of EURO 85.430

H. INDIRECT TAX

Types of indirect taxes include VAT, excise tax and customs duty (import duty and export duty).

VAT is imposed on the provision of goods or services in Cyprus, on the acquisition of goods in Cyprus from other Member States and on the importation of goods in Cyprus from any place outside the EU countries.

The current VAT rates are as follows:

-

0% Zero rate

-

5% Reduced rate

-

9% Reduced rate

-

19% Standard rate

I. OTHER TAXES

Other type of taxes comprises the Wealth Tax, Inheritance Tax and Succession Law, and Immovable Property Tax, none of which is applicable in Cyprus.

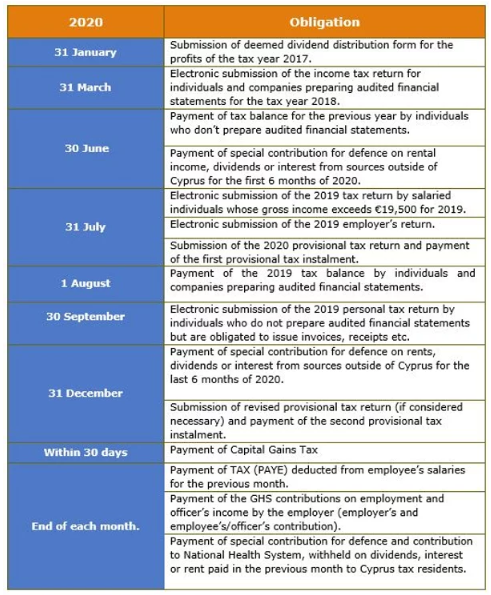

J. TAX CALENDAR

Note: In case of late submission of the relevant tax forms and late payment of the tax due, penalties will apply.

K. HOW KINANIS CAN ASSIST

-

Preparation, completion and submission of Permanent Residency or Citizenship application and relevant supporting documentation

-

Introduction of real estate agents in Cyprus

-

Registration with Migration department

-

Registration with the Tax Department as a resident but non domicile individual

-

Completion and submission of annual tax returns

-

Obtaining tax residency certificate

-

Opening of Bank accounts in Cyprus

-

Assistance to tax and legal related matters

-

Accounting and Payroll Services

L. CONCLUSION

Immigrating to any country is not an easy decision to make, various considerations must be taken into account. With this publication we try to give a brief outline of the possible tax aspects and effects of such immigration on the income of individuals.

With careful pre-immigration tax planning any adverse taxation effect might be reduced or even eliminated. One though must consider very carefully his/her personal aspects and factual situation and decide on the appropriate tax planning steps.

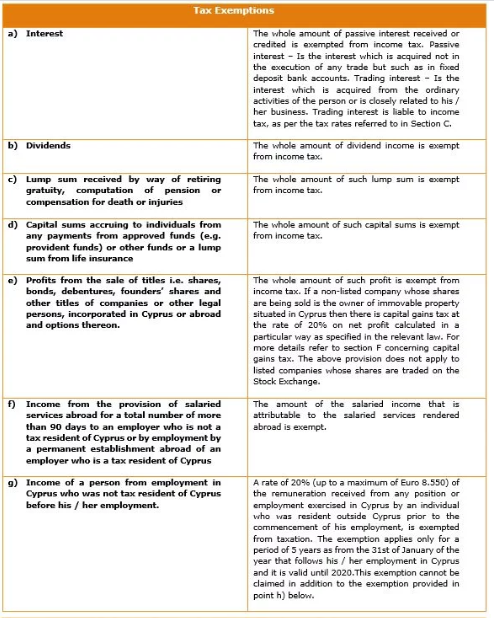

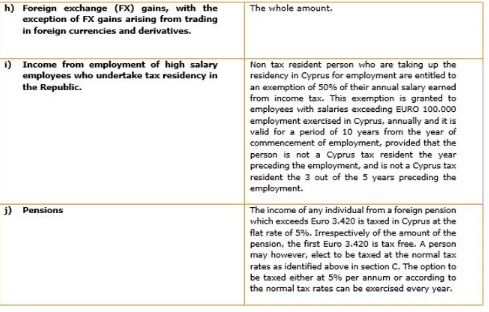

Schedule 2 – Tax exemptions