The abolition of SDLT for some first-time buyers will no doubt grab all the headlines on tomorrow's front pages, but we predict that people will look back on today as the day on which the starting pistol was fired on codification of employment status. This will have a significant impact on all areas of the economy in the years to come.

If you would like to discuss any issues arising from today's Budget, please let me know (my details are below).

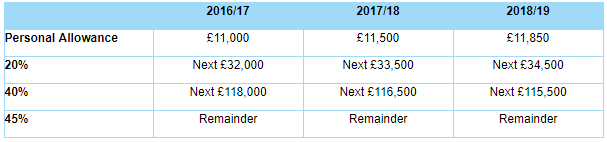

Income tax rates

The personal allowance will increase, rising from £11,500 in 2017-18 to £11,850 in 2018-19. The government aims to raise the personal allowance to £12,500 by 2020. The various rates are shown in the table below.

The personal allowance is still withdrawn by £1 for every £2 of net income beyond £100,000. Net income between £100,000 and £123,700 (in 2018/19) is therefore effectively taxed at 60%. An individual's net income is still reduced by pension payments and charitable donations.

Stamp duty land tax - relief for first-time buyers

The government is reintroducing a relief for first-time buyers of dwellings (we had one between 2010 and 2012).

A purchase for £300,000 or less will be wholly exempt. If the price is between £300,001 and £500,000 the first £300,000 is exempt and the excess over £300,000 is taxed at 5%. At £500,001 full rates kick in, so that on a price of £500,000 the SDLT would be £10,000 but on a price of £500,001 it would be £15,000.

This applies to purchases on or after 22 November 2017, even if contracts were exchanged before that date.

The buyer must never have owned any other dwelling anywhere in the world, even if acquired by gift or inheritance, or even if let out. The buyer must intend the property to be his or her principal private residence. Where the purchase is a joint one, each buyer must fulfil these conditions. However, the fact that the buyer owns commercial property does not matter.

The fact that the buyer owns or has owned a lease of a dwelling where the lease had less than 21 years to run does not disentitle him to the relief.

Stamp duty land tax - 3% surcharge - minor amendments

There some minor changes to the 3% surcharge rule. This has applied since April 2016, essentially to the purchase of additional dwellings where the buyer already owns a dwelling, unless he is replacing a principal private residence.

The surcharge will not apply in certain cases, including:

-

where a divorce-related court order has prevented someone from disposing of their interest in the main residence;

-

where a spouse or civil partner buys property from another spouse or civil partner, or

-

where a purchaser adds to his or her interest in his or her current main residence (such as buying the freehold reversion).

To obtain replacement of main residence treatment the purchaser must dispose of the whole of his or her former main residence and must do so to someone who is not his or her spouse or civil partner.

These changes apply in relation to purchases on or after 22 November 2017, even if contracts were exchanged before then.

Stamp duty land tax - filing date

It was announced some time ago the government planned to reduce the period by which the SDLT return and payment must be made from 30 days to 14 days. It has been announced that this will happen for property transactions taking place on or after 1 March 2019.

Am I an employee?

There has been a whole range of decisions recently on employment status both from the employment and tax point of view as well as union arguments relating to workers (just a few recent ones being Pimlico Plumbers, Uber and only last week Deliveroo). This is against the backdrop of public sector engagers being forced since 6 April 2017 to look through personal service companies when applying this test and therefore more frequently being required to operate PAYE.

It was announced today that there would be two reviews: first as to whether the private sector engagers should follow where the public sector has led (and our best guess is this will happen to 'iron out unfairness' with effect from April 2019 or 2020); and second to explore a way to make the employment status tests for both employment rights and tax clearer. This is not an impossible task but will certainly not be an easy one. We await with interest how they will deal with mutuality of obligations, substitution rights and the underlying worker's financial risk.

In the meantime, we expect HMRC's interest in the area of employment status to pick up substantially but each and every case is very fact heavy and it is imperative for businesses to have a clear understanding of their own fact pattern (with a review very helpful to understand risk areas).

CGT (the hidden surprise)

Buried half way through the Red Book is an announcement that all gains accruing to non-residents on UK commercial property will be brought within the scope of UK tax with effect from April 2019. This aligns the position with residential property but is still a shock.

EIS etc.

Individuals who subscribe for shares in a qualifying EIS company receive tax relief of 30% of the cost of the shares. The maximum qualifying annual investment that an individual could make was previously £1 million. This annual limit has now been increased to £2 million provided everything over the initial £1 million is invested in knowledge intensive companies (basically this is a company that spends at least 10% of its expenditure on R&D activities).

The annual limit on the amount of EIS investments that a knowledge-intensive company can receive is to be increased from £5 million to £10 million.

Tax motivated

A new condition is to be introduced to the EIS, SEIS and VCT rules. This additional restriction is intended to exclude limited risk or low risk investments which are intended to preserve the investor's original capital.

This restriction is intended to apply if most of the investor's return on the proposed investment is intended to be generated by the tax relief that would be obtained through EIS/SEIS/VCT with limited risk to the original investment and weighed against the company's objectives to grow and develop.

VAT

Notwithstanding some press commentary to the contrary, the Office of Tax Simplification in its recent report on VAT did not recommend the lowering of the VAT Registration Threshold to £20,000. However, it was today announced that this threshold, which can create cliff edges, will be frozen for two years at its current level of £85,000. (Once your annual VATable turnover goes over this threshold you must register and charge VAT to all your customers, perversely making it sometimes competitive to close a shop to stay below the threshold.) A review is to be undertaken to essentially soften this cliff edge whilst not over-complicating VAT further.

Under current rules, if a non-UK business sells UK-located goods to UK customers it must register for VAT straight away and start charging its customers (the VAT registration threshold noted above does not apply to these types of overseas businesses). Currently, if an overseas trader is selling goods to UK customers via an online marketplace such as eBay and fails to charge / pay VAT over to HMRC, HMRC can notify such online marketplace that it (i.e. the online marketplace) is from that point essentially guaranteeing the payment of the VAT. In practice, no online marketplace will want to take on this responsibility so this stick ensures they remove the trader or ensure proper compliance.

From Royal Assent to the Finance Bill, this is being extended so that HMRC can give notices to online marketplaces relating to UK businesses (who do benefit from the VAT registration threshold). Also if an online marketplace knows or ought to have known that a particular overseas trader is not registered for VAT but should be registered, the online marketplace has 60 days to stop that trader from selling to the UK or the online marketplace will in effect be guaranteeing their VAT obligations.

Increase in research and development expenditure credit

Research and development expenditure credit is available to companies engaged in a broad range of qualifying activities. The cost of certain expenses such as qualifying staff costs or consumables can be enhanced and then "surrendered" in return for a tax refund. Companies have the alternative option of offsetting the enhanced cost against profits if they are profitable. This change, below, helps loss making companies who claim the credit as opposed to profitable companies who offset the enhanced cost against their profits.

Currently this credit is set at 11% of the enhanced "surrendered" loss; that figure is to increase to 12% in respect of expenditure incurred from 1 January 2018 (increasing the value of the credit).

The end of indexation

Indexation is a mechanism for reducing the capital gain a company makes when selling a capital asset. Indexation works by allowing a further deduction when calculating the gain. This deduction is calculated by reference to the time the asset has been held and its base cost, it broadly can be thought of as an uplift in the purchase price of the asset in line with inflation.

Indexation was abolished for individuals in 2008 and now this tax advantage is to be taken away for companies, aligning company tax treatment with that of individuals. The measure will take effect from 1 January 2018. For disposals after this date, indexation will still be allowed up to 1 January 2018. The impact of this measure will increase with time; the government anticipates it generating an extra £500million in tax in 2022-23.