Background

On 10 January 2025, the Registrar of the Companies Commission of Malaysia (“Registrar”) issued the following revised documents:

- Guidelines for the Reporting Framework for Beneficial Ownership of Companies (Revised 10 January 2025) (“Revised Guidelines”); and

- Case Studies and Illustrations of the Guidelines for the Reporting Framework for Beneficial Ownership of Companies (Revised 10 January 2025) (“Revised Case Studies”).

The Revised Guidelines supersede, inter alia, the Guidelines for the Reporting Framework for Beneficial Ownership of Companies issued on 1 April 2024 (“Superseded Guidelines”), while the Revised Case Studies supersede the Case Studies and Illustrations of the Guidelines for the Reporting Framework for Beneficial Ownership of Companies issued on 1 April 2024 (“Superseded Case Studies”).

The Superseded Guidelines were issued to assist companies to understand and fully comply with the beneficial ownership reporting requirements under the new Division 8A that were introduced into the Companies Act 2016 (“CA 2016”) on 1 April 2024. In particular, the Superseded Guidelines set out the criteria for determining a beneficial owner, the obligations of the directors and the secretary to ascertain the beneficial owners of the company, specimen enquiry and response forms that may be used to ascertain details of the beneficial owners of the company and the requirement to provide the details of a senior management personnel where the company has no beneficial owner or the beneficial owner cannot be identified. The Revised Guidelines serve the same purposes and are essentially an update of the Superseded Guidelines.

The Superseded Case Studies complement the Superseded Guidelines and provide case studies and illustrations to facilitate the understanding of the Superseded Guidelines. The Revised Case Studies serve the same purposes in relation to the Revised Guidelines and are essentially an update of the Superseded Case Studies.

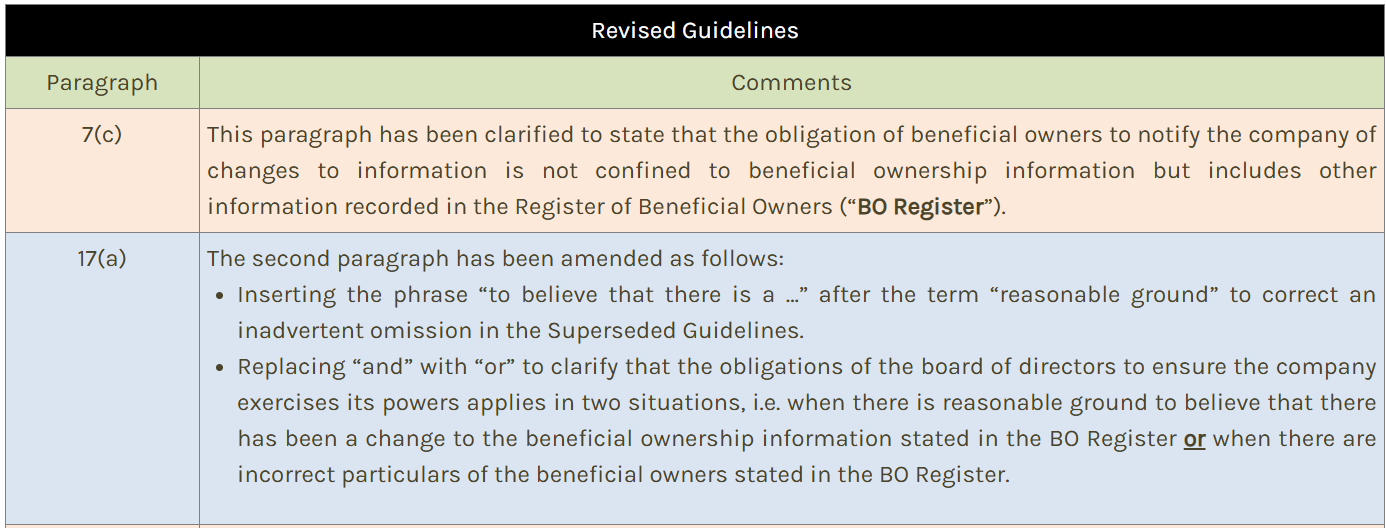

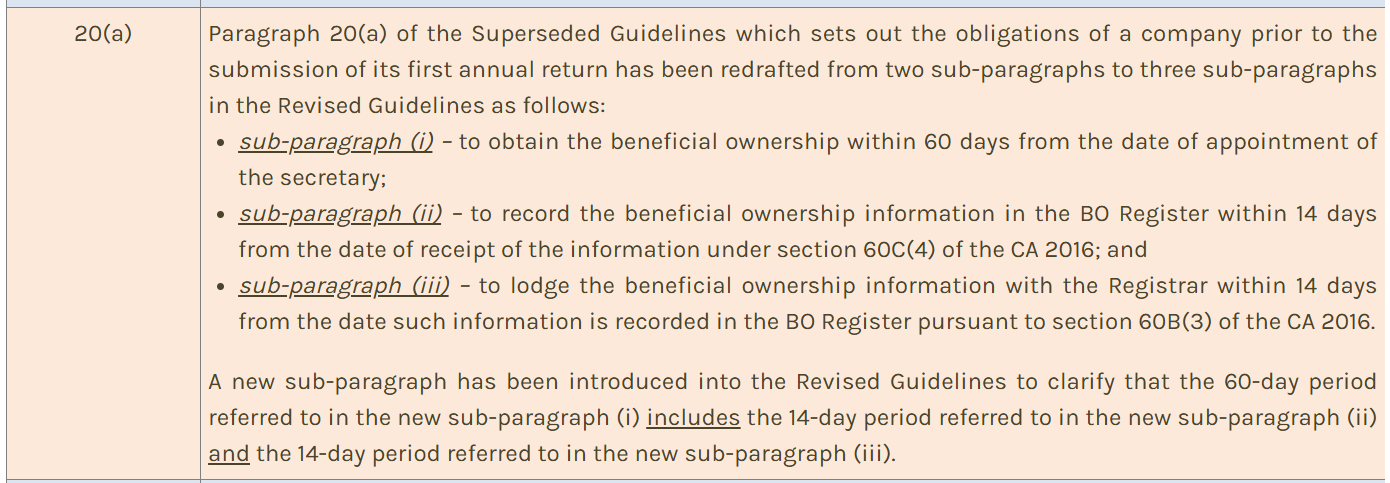

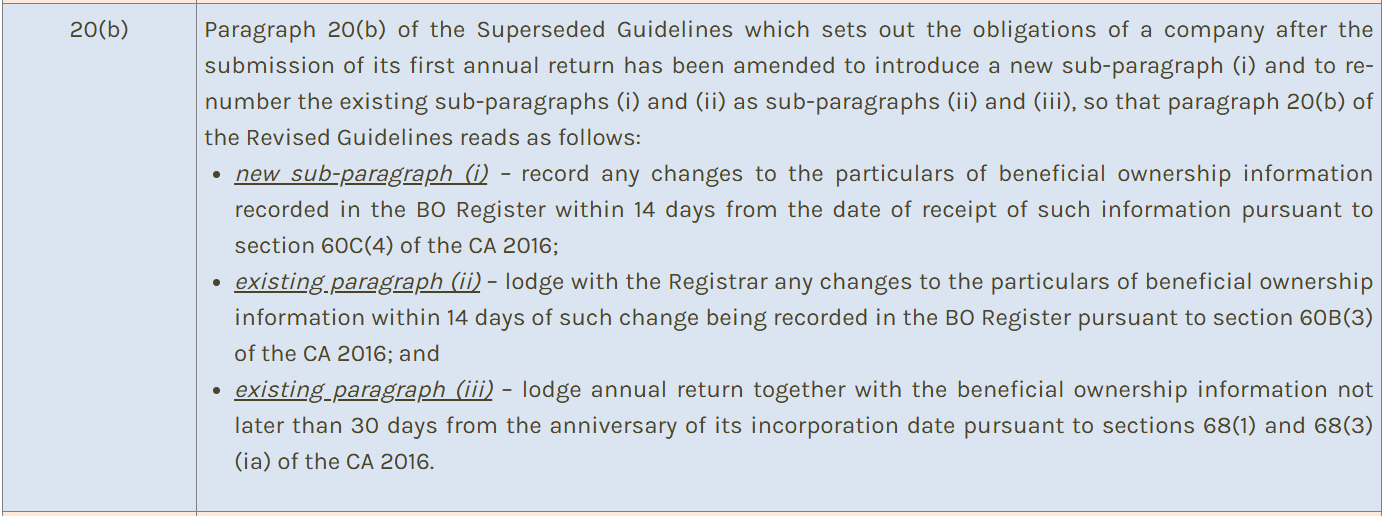

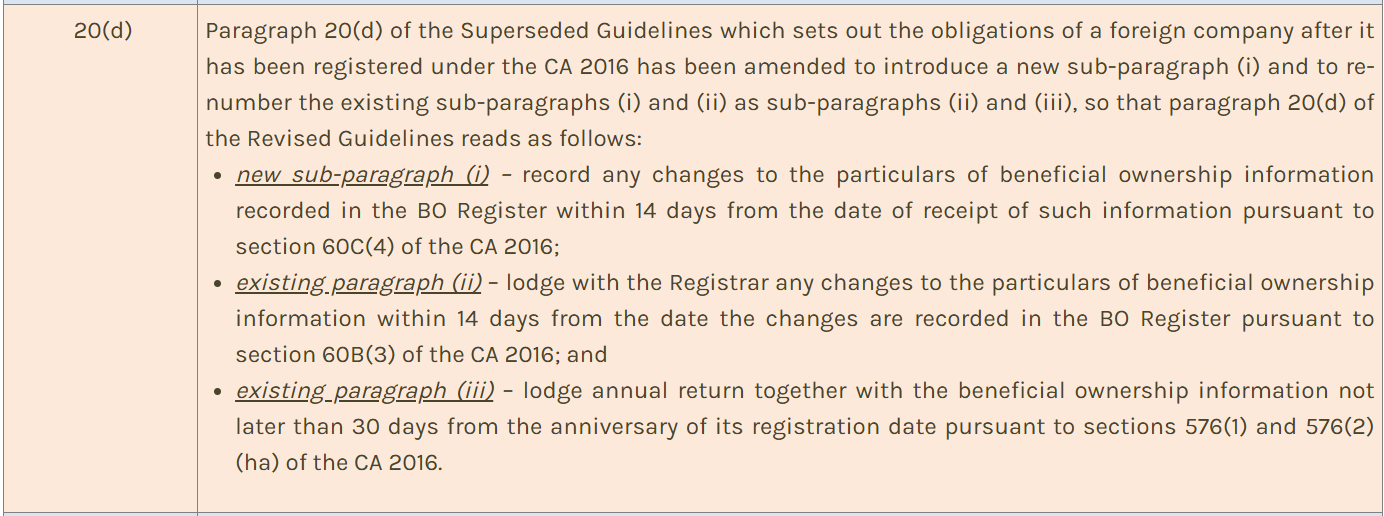

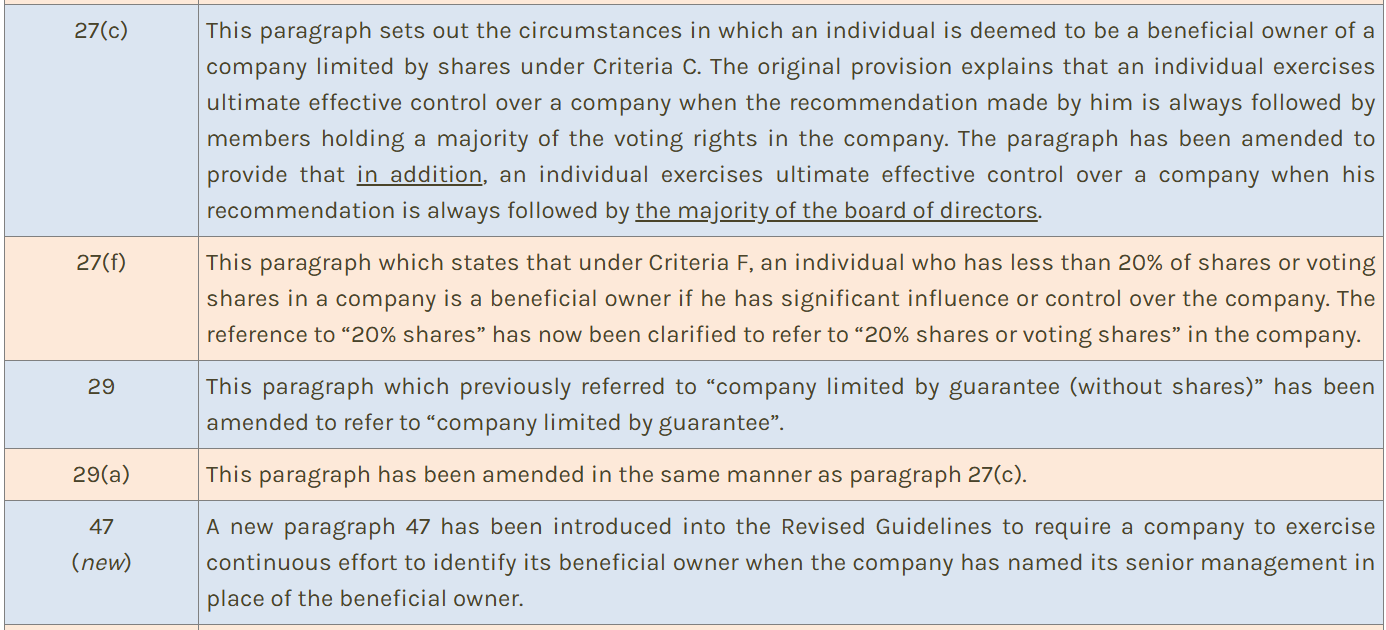

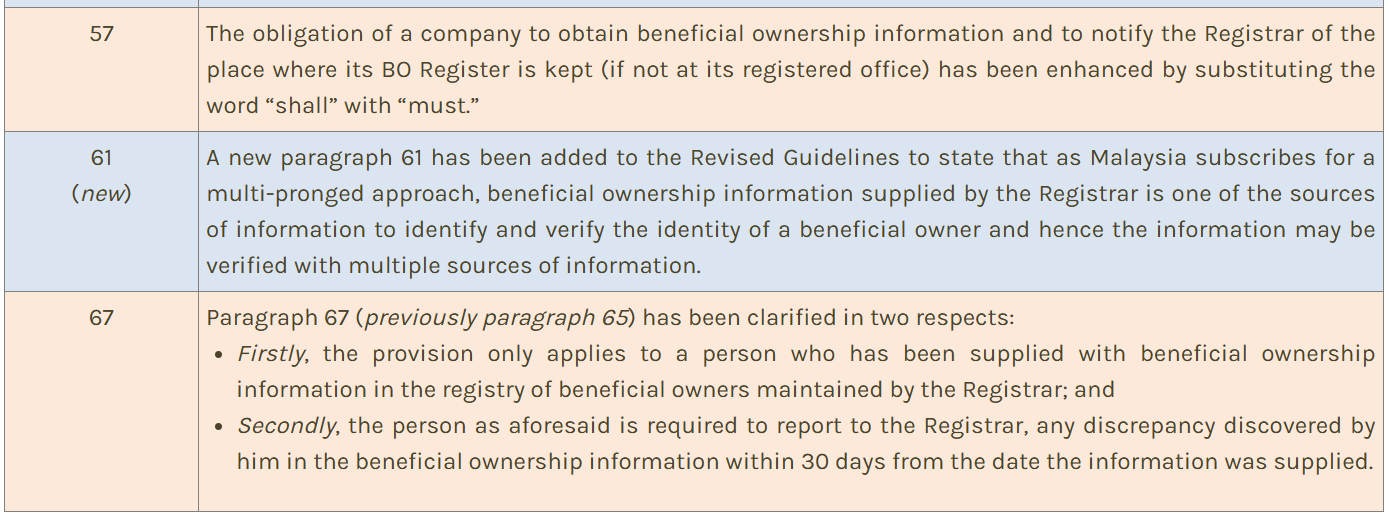

Key changes in the Revised Guidelines

The key changes introduced under the Revised Guidelines are as follows:

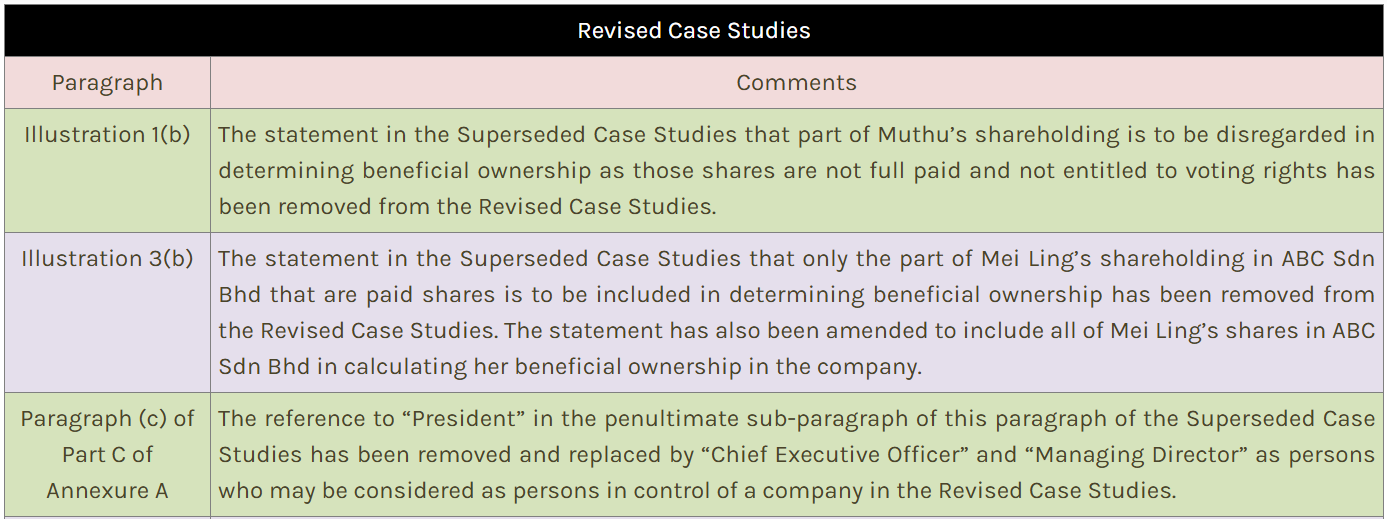

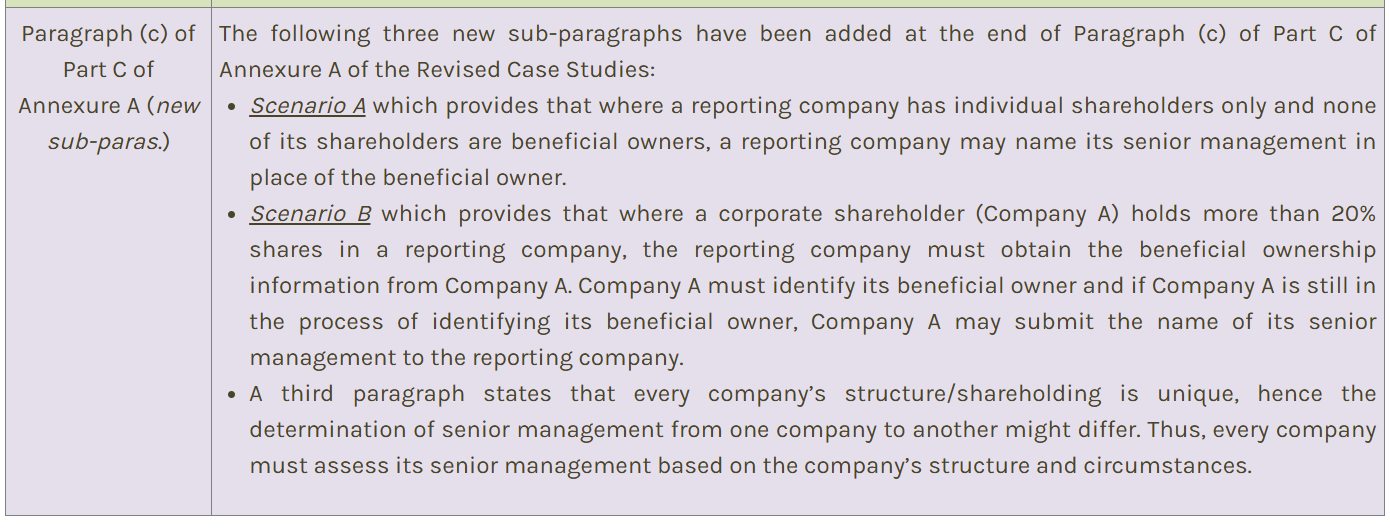

Key changes in the Revised Case Studies

The key changes introduced under the Revised Case Studies are as follows:

Comments

As mentioned earlier, the Revised Guidelines update the Superseded Guidelines, and the Revised Case Studies update the Superseded Case Studies. In addition to the above revisions, a number of drafting amendments have been made in the Revised Guidelines to clarify the provisions in the Superseded Guidelines.