Introduction

Real estate is a significant sector in the UAE but the new corporate tax law was initially silent on many aspects of the real estate businesses. A recent cabinet decision has clarified the taxation of revenue deriving from real estate for companies and individuals.

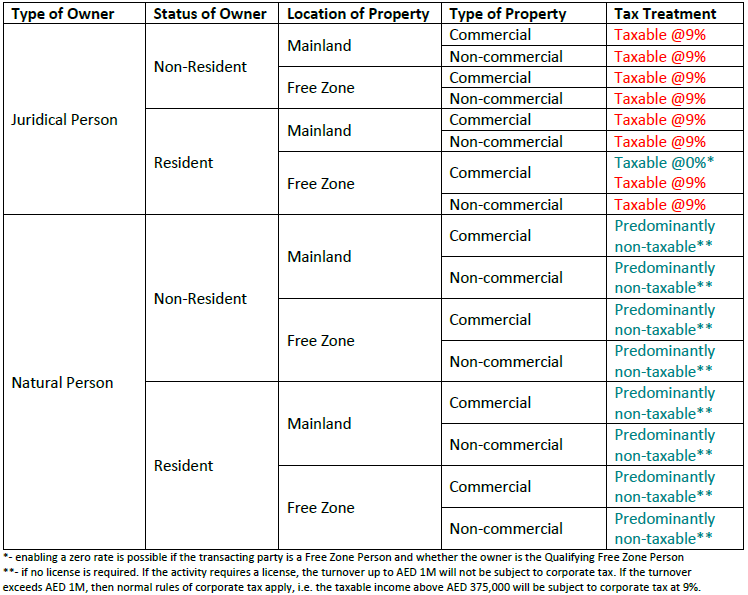

Tax Treatment of the property held by a natural person

A natural person who owns property in the UAE may be subject to taxation under the provisions of Cabinet Decision No. 49 of 2023 if the activity is related to any licensed commercial activity.

According to this decision, businesses or business activity of a natural person, be it a resident or a non-resident, are subject to corporate tax if the turnover derived from such activities exceeds AED 1M within a calendar year.

However, if the activity of the natural person is investment activity that can be conducted without a commercial license that relates to (directly or indirectly) the sale, leasing, sub-leasing, and renting of the real estate, then the income from such activity is non-taxable. However, if the activity requires a license, such as the management of real estate, then the income is subject to corporate tax with the application of the above threshold of AED 1M.

Each Emirate has its own laws in regard to real estate business. Hence, natural persons should monitor closely business licensing laws in the Emirates where they hold their properties to properly assess tax implications on the income received from the real estate.

Tax Treatment of the property held by a company

For a company that owns real estate, there are three categories of property that are treated differently:

- - Non-commercial property

- Commercial property inside a free zone

- Commercial property outside a free zone (on the ‘mainland’)

For non-commercial properties, which includes real estate that is used non-exclusively as a place of residence or accommodation including hotels, motels, bed and breakfast establishments, serviced apartments and the like, the income attributable to such property will be subject to corporate tax at 9% as a rule.

If the property is commercial and in the free zone, then the treatment will be different for owners that have the status of a Qualifying Free Zone Person (QFZP) to those that are treated as typical taxpayers. If the owner has the status of the QFZP (as explained in our previous alert) and the other transacting party is also established in the Free Zone, then income sourced from such activity will be considered as the Qualifying Income and subject to corporate tax at 0%.

In any other case, i.e., transacting party is established outside the Free Zone, or the owner does not meet conditions for the QFZP (or made an election to be a regular taxpayer despite meeting conditions for the QFZP status), the income sourced from the commercial property located in the Free Zone will be subject to corporate tax at 9%.

The above is summarized in the below table for ease of reference: