Introduction

All Government departments, including Revenue, are obliged to prepare Statements of Strategy at regular intervals. In January 2021 Revenue published its Statement of Strategy for the period 2021 to 2023, the twin pillars of which were “Service for Compliance” and “Confronting Non-Compliance”. One of the primary areas of focus was maximising timely compliance, and reference was made to the proposed introduction of a revised framework of compliance interventions:

“We will further enhance our real-time engagement and response to risk, building on the segmentation of our customer base. We will leverage our data holdings and capacity for advanced analytics. We will continue to encourage self-review and correction by taxpayers. We will implement a revised framework of compliance interventions that supports early and effective engagement to address non-compliance, based on the level of risk and taxpayer behaviour.”

New Code

On 11 February 2022 Revenue published its new Code of Practice for Revenue Compliance Interventions (“the new Code”).1 The new Code will come into effect on 1 May 2022 and replace the Code of Practice for Revenue Audits and Other Compliance Interventions issued in 2019 (“the existing Code”). It has been published almost three months before its “go-live” date to give both Revenue officials and practitioners an opportunity to familiarise themselves with its content and the changes in the approach to Revenue compliance interventions that it will introduce.

The new Code features Revenue’s “Compliance Intervention Framework”, which was signalled in its Statement of Strategy. This represents a significant departure from the approach to Revenue audits and interventions under the existing Code. This edition of Irish Tax Review features an article by Revenue setting out in detail how the new Compliance Intervention Framework is intended to operate, and I would encourage all readers to take the time to review it. (See also article by Irish Tax Institute, in this issue).

Risk Review

The Compliance Intervention Framework provides a graduated response to risk and continued non-compliance. This response ranges from self-correction opportunities through to tax audits and investigations, across three “levels” (Level 1, 2 and 3). Perhaps the most significant aspect of the new framework is the introduction of a new type of intervention, the “risk review”, at Level 2.

A risk review is a Revenue inquiry for the purposes of s1077F TCA 1997 and is a focused intervention to examine a risk or a small number of risks on a tax return where a full audit is not warranted. Once notified of a risk review, a taxpayer will no longer be afforded the opportunity to make an unprompted qualifying disclosure, and any disclosure will be treated as a prompted qualifying disclosure. This results in a reduction in the mitigation of penalties that is currently available for unprompted qualifying disclosures which are made before receiving a Revenue audit notification.

It would appear that the risk review was introduced to address a view held in some quarters that taxpayers were not necessarily incentivised to regularise their tax affairs unless prompted to do so. Under the existing Code, a taxpayer has an opportunity to make an unprompted qualifying disclosure at any point before the notification of a Revenue audit. Therefore any intervention by Revenue via phone, email, letter, MyEnquiries etc. that raises queries but does not constitute a notification of a Revenue audit provides a taxpayer a chance to avail of the benefits of an unprompted qualifying disclosure and obtain greater mitigation of penalties.

As the number of non-audit interventions carried out by Revenue has increased in recent years, taxpayers who had concerns over tax-related issues may have considered postponing a potential tax issue until first contact was made by Revenue. The “risk review” is intended to address this perceived weakness in the existing Code. The lead-in time to the new Code’s becoming operational on 1 May should therefore be used by taxpayers and their advisers to consider whether there are any matters that would best be dealt with by means of an unprompted qualifying disclosure, before risk review letters can be issued.

The other type of intervention at Level 2 is a Revenue audit. Section 3 of the new Code contains an overview of both risk reviews and Revenue audits and includes details on location, conduct and escalation of these types of intervention.

Institute’s Response

The Institute’s TaxFax of 11 February 2022 sets out a response to the publication of the new Code. It contains:

• an outline of the main features of the Compliance Intervention Framework,

• a note of the Institute’s representations to Revenue before the publication of the Code and

• a summary of the ways in which members will be kept informed by the Institute of the issues arising from the implementation of the new Code over the coming weeks and months.

It is recommended that all members familiarise themselves with these key changes and the timing of their implementation.

Finance Act 2021

The introduction of the new Code necessitated a number of changes to the legislation governing penalties for tax defaults and the publication regime. We will now consider these legislative changes and how they are reflected in the Code .

Sections 74, 75 and 76 Finance Act 2021: Penalties.

Section 74 Finance Act 2021 provides that s1077E TCA 1997,2 which sets out the penalty regime for deliberately or carelessly making incorrect returns etc., shall not apply in respect of any disclosure made, act done or omission made after 21 December 2021 (the date of the passing of Finance Act 2021). Similarly, s76.

Finance Act 2021 provides that s116 VATCA 2010, which contains the penalty regime for deliberately or carelessly making incorrect VAT returns etc., shall not apply in respect of any disclosure made, act done or omission made after 21 December 2021.

Section 75 Finance Act 2021 inserts a new s1077F in TCA 1997. Section 1077F substantially reproduces the provisions previously contained in s1077E but contains the following notable changes:

• Penalties will not be charged for technical adjustments, innocent errors and cases where total tax defaults are less than €6,000 and are in the careless rather than deliberate behaviour category of default. This provides a legislative basis for the administrative practice that applies under the existing Code.

• The calculation of the tax-geared penalty where no return has been filed will be based on the tax paid before the notification of a Revenue inquiry or investigation rather than before the commencement of a Revenue inquiry or investigation.3

• The prohibition on mitigation of penalties in offshore cases has been removed.

Section 75 also inserts a new s116A VATCA 2010 and makes amendments to s134A SDCA 1999 and s58 CATCA 2003, which mirror the changes in s1077F.

Offshore Matters

Although it does not represent a shift in Revenue practice, the legislative change in the application of the penalty regime to technical adjustments and innocent errors is to be welcomed. Of more significance, however, is the removal of restrictions on mitigation of penalties in offshore matters.

Many readers will recall the strong reaction generated by the changes to s1077E that were introduced by s56 Finance Act 2016. These changes set out certain circumstances where a disclosure would not be a qualifying disclosure and would lead to unavoidable publication on the list of tax defaulters and unmitigated tax-geared penalties. In particular, a disclosure made on or after 1 May 2017 was not treated as a qualifying disclosure (1) where any matters contained in the disclosure related directly or indirectly to “offshore matters” (essentially meaning any income, gains, accounts or assets accruing, arising, situated or located outside of the State) and (2) in any other case where a disclosure was not made but the person had a tax liability resulting from offshore matters that were known or became known to Revenue at any time. There was a carve-out in relation to (2) in that the disclosure may still have been qualifying if (a) the penalty was less than 15% of the total correct tax due or (b) the behaviour was careless but not deliberate.

Revenue policy on interventions, as enshrined in Codes of Practice over the years, has been to encourage and facilitate taxpayers to come forward and regularise their tax affairs when they become aware of tax underpayments or defaults. When advising clients, tax practitioners can point to incentives such as protection from prosecution, mitigation of penalties, avoiding publication etc. and highlight the benefits associated with making a disclosure. This approach is generally seen to be a “win–win” for taxpayers and the Exchequer.

By introducing a blanket ban on the benefits of disclosures for offshore matters after 1 May 2017, the incentive for taxpayers to come forward and regularise their tax affairs was effectively removed. For practitioners, it was difficult to highlight to clients the benefits (apart from restricting a potential exposure to interest on non-payment of tax) of notifying Revenue of an offshore matter. As a policy, it did not appear to be in the interest of fostering a culture of compliance that an individual who identified an offshore matter was not going to materially benefit from voluntarily addressing it with Revenue.

The introduction of this legislation, as a precursor to the implementation of the new Code, is a very welcome change in policy.

Sections 77 and 78 Finance Act 2021: Publication of Tax Defaulters

Section 1086 TCA 1997 requires Revenue to compile lists of certain tax defaulters on a quarterly basis and publish such lists in Iris Oifigiúil within three months of the end of the particular quarter. Lists of defaulters may also be publicised or reproduced by Revenue in any manner that it considers appropriate. Section 77 Finance Act 2021 provides for the ending of the current publication regime in s1086 TCA 1997 with effect from 31 December 2021.

Section 78 Finance Act 2021 inserted a new s1086A in TCA 1997, replacing s1086. The new section makes a number of amendments to the criteria for publication and the details to be published, which include:

• A settlement will not be published when the tax underpayment made or refund incorrectly claimed is less than €50,000. Under s1086, any settlement where the combined tax, interest and penalty exceeded €35,000 was publishable. However, where a settlement is published, the full amount, including interest and penalties, will be published.

• Where any part of a settlement is not subject to a penalty, such part will not be published.

These amendments are to be welcomed and had been the subject of extensive representations by the ITI.

Other amendments are:

• Surcharges and any fixed penalties will be publishable, where applicable.

• Settlements will be published where refunds have been incorrectly claimed.

• The details in relation to a tax defaulter’s name have been expanded to include any trading name or previous name. This is with a view to preventing a defaulter from avoiding recognition by using an alternative name.

The new provisions apply to “relevant periods”, a relevant period being the period beginning on 1 January 2022 and ending on 31 March 2022, and each subsequent period of three months beginning with the period ending on 30 June 2022.

In a Committee Stage amendment, the definition of “qualifying disclosure” was updated to include settlements in relation to excise matters. This ensures that the same.

Next Steps

A good working knowledge of the operation of the new Code will be an essential tool for tax practitioners. As set out in the Institute’s TaxFax of 11 February 2022, the following actions will be taken to inform and assist members in the transition to the new Code:

• Stream 3 of the Annual Tax Summit on 1 April 2022 will include an update on the Compliance Intervention Framework and the revised Code from Aidan Lucey, PwC, who will be joined by a Revenue speaker for the Q&A session.

• Before 1 May, the Institute will advise on practical aspects of the notification treatment will apply to such disclosures as apply in relation to other taxes, that is, a qualifying disclosure will not be published but a settlement may be published if the tax is not paid in accordance with the terms of the qualifying disclosure.

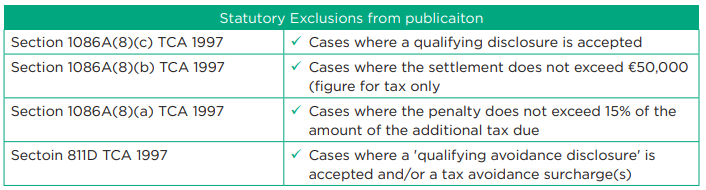

Chapter 5 of the new Code: Publication in List of Tax Defaulters

Chapter 5 of the new Code (pages 64 and 65) sets out the rules governing the obligation to publish, exclusions from publication and determining the publication figure.4 It includes the following table, which is a useful summary of the statutory exclusions from publication:

procedures, such as the format of the notification letters, the channels for issue to taxpayers and their agents (i.e. paperbased/electronic) and the issue of reminder notifications on risk reviews.

• The Irish Tax Series 2022 will include publication of a third edition of Revenue Audits and Investigations – The Professional’s Handbook, to be released later in 2022.

• The Institute will monitor members’ experiences of the practical implementation of the new Framework and the revised Code during 2022, to draw any emerging issues causing difficulty or requiring clarity to the attention of Revenue’s compliance policy personnel at an early stage.