Every transaction is different, but transactions involving behavioral health facilities and services share particular similarities with respect to regulatory issues that are important for any potential investor to understand. We have set forth below several common issues that investors should consider when contemplating the acquisition of a behavioral health business.

Diligence

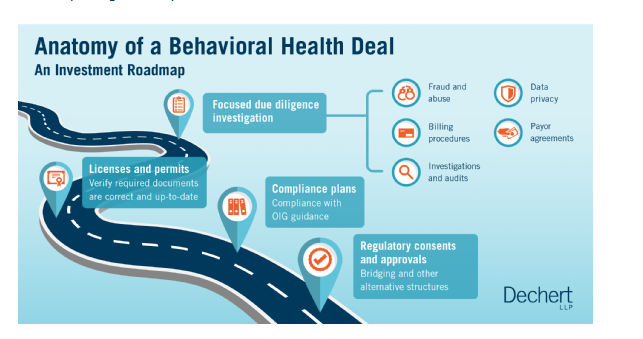

Regulatory diligence of behavioral health facilities requires a specific review of the seller’s compliance with various federal and state health care regulations. For any deal involving a behavioral health facility or service licensed by a state regulatory body or accredited by an accrediting body, diligence should be conducted to verify that:

-

Licenses and permits required to operate the facility are issued to the correct entity.

-

Both the effective and expiration dates are confirmed.

-

The correct license type for the service level of care has been obtained.

Accreditation may be voluntary or effectively required if a state licensing authority cedes its review to such a body (often referred to as “deemed states”). Buyers should conduct diligence to review at least the past three years of the seller’s inspection and enforcement history to understand the seller’s track record regarding regulatory compliance with licensing standards. Such diligence would include a review of operational deficiencies cited against the facility, correction plans and any penalties assessed against the facility.

Also, diligence should be conducted with regards to the behavioral health facility’s compliance plan. A strong compliance plan would comply with guidance provided by the Office of Inspector General (OIG) and would address policies and procedures related to referral arrangements, data privacy, billing and coding procedures, compliance history with respect to government payor programs and third-party insurance payor agreements, and external and internal investigations of the operator, its principals and its staff.

-

A potential buyer should diligence financial arrangements with referral sources to ensure that payments have not been made in return for referrals or other business paid for by government payment programs. If such arrangements exist, it is important to understand whether the arrangements fit into an exception under the Stark law and/or a safe harbor under the Anti-Kickback Statute and comply with all other applicable federal and state fraud and abuse laws.

-

Behavioral health facilities are required to protect the health information of its residents. Providers are likely covered entities under The Health Insurance Portability and Accountability Act of 1996 (“HIPAA”). Substance abuse treatment providers may also be subject to the data privacy regulations of 42 CFR Part 2 (“Part 2”), which specifically protects the confidentiality of addiction treatment records. A potential buyer should review HIPAA and Part 2 privacy and security policies and business associate agreements as well as any prior breaches of protected health information for continuing liability and appropriate corrective action.

-

A potential buyer should perform due diligence of the behavioral health facility’s billing practices, including claims processes and procedures and billing and collections processes, particularly as it relates to government payment programs. The buyer may consider conducting a billing and coding audit as part of financial due diligence and should pay careful attention to any claims for prior overpayment.

Conducting legal due diligence on the target business provides the opportunity to better ascertain a fair purchase price of the behavioral health business and identify liabilities for which the buyer may be liable after consummation of the transaction. Legal due diligence with respect to health care issues can complement accounting or business diligence to contextualize financial liabilities particular to the health care sector such as payor overpayment liabilities, deferred revenues and reimbursement obligations. Such liabilities are important to identify because they may require adding additional closing conditions, or such liabilities may need to be addressed as adjustments to purchase price or through a net working capital adjustment.

Liability for non-compliance with regulatory requirements can range from financial penalties, which can be significant, to criminal liability under certain circumstances.

Additionally, representations and warranties insurance policies have become increasing available for targets operating in the health care sector, and the insurers are increasingly willing to cover items that were previously excluded from coverage to the extent the buyer can demonstrate its adequate performance of due diligence with respect to such items.

Structuring the Transaction

The parties should consider deal structure in light of the necessary regulatory approvals. Asset sales and joint ventures will almost always require full regulatory approval of the change of the ownership of the facility since the buyer or JV entity will become a new licensed operator of the behavioral health facility, and such transactions will constitute a “change of ownership” as defined by the state in which the facility is located. However, pursuant to stock sales or mergers, the shares, membership interests or partnership interests of the licensed operator will be purchased; therefore the licensed entity stays in place, which is often referred to as an “indirect change of ownership.” Regulatory approval may not be required in a stock sale, depending on how “change of ownership” is defined in the state. In most states, at a minimum, a notice to the regulator would be required where the licensed entity will remain but that entity’s ownership will change.

To the extent that the parties decide on a structure that will require regulatory approval, such approval could take anywhere from 30 days to two years. In certain states in which there is a lengthy regulatory approval process and it is permitted, the parties may consider a bridging structure, whereby the parties close the deal while the regulatory approvals are pending with the buyer entering into a management agreement with the current licensee. The terms of such a management agreement often provide that the buyer will receive the economic and operational equivalent of the transfer of the behavioral health assets.

Key Negotiating Points

The representations and warranties for the purchase agreement should be reviewed carefully to confirm they include certifications that the behavioral health facility:

-

Has operated the business in a compliant manner.

-

Possesses all necessary healthcare licenses and permits.

-

Is in compliance with state and local licensing laws.

-

Is in compliance with fraud and abuse laws, including anti-kickback statutes.

-

Is in compliance with HIPAA and Part 2 compliance, if applicable.

-

Has formal and informal arrangements at the facility, including relationships with payors, vendors and residents that comply with applicable laws.

A robust set of regulatory covenants may be necessary in deals that do not involve a simultaneous signing and closing. Such covenants should include requirements that the seller:

-

Continue to operate the facility and maintain all licenses in good standing.

-

Promptly provide copies of all written correspondence with regulatory authorities or payors.

-

Cooperate in obtaining buyer’s licenses and permits and any required regulatory approvals.

The parties should agree on who will retain or assume liabilities after closing. Generally, an asset sale that is structured appropriately will allow the buyer to avoid assuming some (but not all) regulatory liabilities. However, in most cases, all regulatory liabilities will be assumed in a stock sale. The indemnification provisions of the purchase agreement allow the parties to alter such arrangements by assigning the relevant liabilities to one party or the other. In a behavioral health transaction, subject to negotiated baskets and caps, the seller is typically responsible for liability for any occurrence prior to the closing, and the buyer is liable for post-closing liabilities. Furthermore, it is not uncommon for specifically identified regulatory indemnities to be subject to larger caps, baskets, or time limitations. If any governmental payor program agreements are to be assumed, a buyer should consider seeking indemnity for fraud and abuse law violations, as well as overpayments and underpayments, so that the buyer will not be responsible for obligations for activities that occurred before closing, but which were not discovered until after closing.

Closing conditions should be outlined in a manner that provide for flexibility in anticipation of regulatory issues that may arise. For example, in addition to a closing condition that simply requires that the parties obtain all required regulatory approvals, such a condition may also include a right to extend the closing date or change to a bridging structure if approvals are not provided when expected. Also, the buyer should consider seeking the ability to reserve the right not to close if there are material pending or threatened administrative, litigation or governmental proceedings, if any material licenses or permits are not in good standing, or if any required regulatory approvals are not obtained.