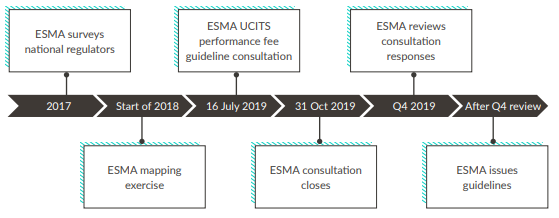

ESMA issued a consultation on guidelines for performance fees in UCITS on 16 July 2019. The date for responses to the consultation is 31 October 2019.

ESMA's analysis in 2018 of the national supervisory practices by national regulators of key aspects of UCITS' performance fees revealed a lack of consistency.

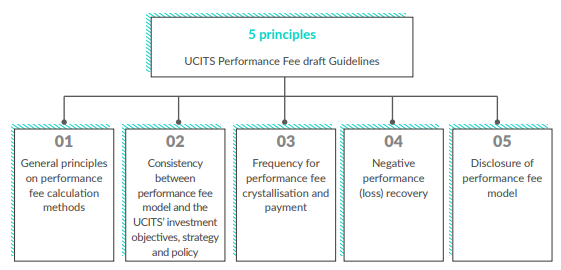

The proposed guidelines are broken down into 5 areas:

- general principles on performance fee calculation models

- alignment of performance fee model and the UCITS investment objectives, strategy and policy

- frequency of performance fee crystallisation and payment

- circumstances where a performance fee is payable

- disclosure

There is a transitional provision provided for existing UCITS operating performance fees of 12 months from the publication date of the guidelines. The publication date is likely to be after Q4 2019. UCITS with performance fees established after the publication of the guidelines will have to comply immediately.

ESMA asks whether the guidelines should also be applied to AIFs marketed to retail investors

The Central Bank of Ireland (CBI) issued a letter to industry on 4 September 2018 following its thematic review of the payment of performance fees by Irish UCITS. The CBI's guidance on UCITS performance fees was codified in the 2019 Central Bank UCITS Regulations

Background

ESMA's mapping exercise on UCITS performance fees during 2018 concluded that there was a lack of harmonization between national regulators in EU jurisdictions in their respective supervision of UCITS performance fees. The consultation on draft guidelines for performance fees has issued following this conclusion. ESMA considered the IOSCO Good Practice for Fees and Expenses of Collective Investment Schemes in defining the 5 principles set out in the draft guidelines.

Principle 1

The performance fee calculation method should include, at least, the following elements:

- Reference indicator

- Crystallization period and crystallization date

- Performance reference period

- Performance fee rate

- Performance fee methodology

- Computation frequency, which should be aligned with NAV calculation frequency

Compared to the current Irish requirements, there should be nothing controversial in these proposals. The gap analysis for Irish UCITS should be straightforward.

Principle 2

The UCITS or its management company should ensure that the performance fee model is consistent with the UCITS’ investment objectives, strategy and policy. For example, a high water mark or hurdle is likely to be more appropriate for absolute return funds than reference to an index. A UCITS with a long equity-focused strategy should consider it inappropriate to calculate its performance fee by reference, for example, to a money market index. If performance fees are payable on the basis of out-performance of a benchmark “X” then calculating performance fees based on “X-1%” would not be appropriate.

This seems reasonable and the gap analysis for Irish UCITS should be straightforward.

Principle 3

The crystallization period should not be shorter than 1 year so as to align interests between the portfolio manager and shareholders and promote fair treatment of investors. It should end on 31 December or at the UCITS’ financial year end. The portfolio manager’s performance should be assessed on a time horizon that is, as far as possible, consistent with the investors’ holding period.

A 1 year period aligns with current CBI guidance. The 1 year period is reasonable but it is debatable whether all UCITS performance fees should crystallise on 31 December or whether they should crystallise on the UCITS’ financial year end. The proposal to align investors’ holding period with the performance reference period should be carefully considered. Performance reference periods of greater than 1 year are likely as a result, more likely to be 3 years, which may to be problematic for managers who rely on annual payments.

Principle 4

A performance fee should only be payable in circumstances where positive performance has been accrued during the performance reference period. Underperformance or loss should be recovered before a performance fee becomes payable.

This is reasonable and the gap analysis for Irish UCITS should be straightforward.

Principle 5

There should be clear and adequate disclosure in the UCITS' prospectus, marketing material, KIID and financial statements. The prospectus should contain concrete examples of how the performance fee will be calculated. The annual and half-yearly reports should display clearly for each relevant share class (a) the actual amount of performance fees charged and (b) the percentage of fees based on the share class NAV.

For Irish UCITS, these requirements should not prove troublesome and the gap analysis should be straightforward. Some prospectuses may need to be updated to provide for a concrete example.

The minimum crystallization period and performance reference period should not apply to the fulcrum performance fee model.

Effective date and transitional provisions

A UCITS with a performance fee established after the date of application of the guidelines will have to comply immediately. It would be worth clarifying if this includes new UCITS sub-funds of existing UCITS umbrella vehicles. Based on ESMA's current projected next steps, this may be from Q1 2020. Existing UCITS with performance fees will have 12 months from the date of the Guidelines to align their procedures. By the same projection, this would be by Q1 2021. This would align with the CBI's transitional provisions in the 2019 Central Bank UCITS Regulations.

ESMA's proposed transition period should be considered by stakeholders from an operational perspective. Depending on the effective date of the ESMA guidelines, if the 12 month transition would cause UCITS to comply with new rules mid-performance reference period and would give rise to issues adverse to investors, these concerns should be fed back to ESMA through the consultation process.

Other ESMA consultation content

Feedback and supporting documentation

The consultation paper contains a discussion of the above 5 principles. There are 12 specific questions about these 5 principles and in total seeks responses to 19 questions. The consultation document contains extracts of the relevant provisions of the UCITS legislative framework and contains the IOSCO Good Practice for Fees and Expenses of Collective Investment Schemes.

ESMA survey of national regulators

There is a summary of the results of the 2017 ESMA survey of national competent authorities on performance fees which makes for interesting reading about the discrepancies between regulators in their supervision of performance fees. For example, two jurisdictions require presentation of performance fees in a table in the prospectus next to the other fees charged. While 20% is the average level of performance fees in the majority of jurisdictions, like Ireland, in two jurisdictions performance fees peaking at 30% were observed. As regards frequency of calculation and payment, most jurisdictions calculate performance fees on a daily basis and charge them on an annual basis.

Some responses indicated calculation on a monthly basis and payment on a quarterly basis. The Irish response in 2017 was that the CBI was to consult on a proposal for accruals and payments to be not less than one year, which we have seen borne out in the updated and consolidated 2019 Central Bank UCITS Regulations.

What about AIFs?

ESMA asks stakeholders to comment on whether the principles set out in the draft guidelines should be applied to AIFs marketed to retail investors. The aim would be to ensure equivalent standards in retail investor protection.

Central Bank of Ireland's current position on UCITS' performance fees

The CBI has recently codified its guidance on UCITS performance fees in the updated and consolidated Central Bank UCITS Regulations which issued 27 May 2019. You can read the ALG publication about the 2019 Central Bank UCITS Regulations here. One of the updated performance fee requirements is that the calculation of a performance fee does not crystallise more than once per year and that the performance fee is not paid more than once per year. There is a transitional provision for existing Irish UCITS to comply with these requirements by 27 November 2020 or such later date as the CBI may specify.

The CBI issued a letter on 4 September 2018 after a thematic review of Irish UCITS's performance fees. The letter highlighted supervisory issues identified from the review. It proposed actions to be taken to mitigate those issues. It also required boards of fund management companies to carry out a review of their existing performance fee methodologies. Specific review guidelines were set out and the CBI commented it will use the industry letter as a reference in any supervisory engagement carried out on UCITS performance fees.

An analysis will need to be done to see if the CBI's current position on UCITS performance fees is aligned with the draft ESMA Guidelines. It would be possible to give feedback to ESMA during the consultation period if any challenging discrepancies are detected. ESMA may accept the proposal. Otherwise any differences between the performance fee requirements in the 2019 Central Bank UCITS Regulations and the final ESMA Guidelines may require an update to the Irish legislation to reconcile.

Conclusion

Irish UCITS with performance fees or those seeking to set up new Irish UCITS funds, and potentially new sub-funds, with performance fees should take account of ESMA's proposed new guidelines.