In This Edition

- Shareholder Proposals for 2026 Proxy Season: SEC Staff to Consider Only No-Action Requests Challenging Propriety of Proposals under State Law

- SEC Chair Atkins Solicits Comments to Reform Regulation S-K

- Directors and Officers of FPIs Required to Begin Publicly Reporting Equity Ownership, Awards, and Transactions on March 18, 2026

- SEC Staff Updates Guidance on Proxies, Integration of Offerings, Regulation D Offerings, and Exchange and Tender Offers

- In Executive Order, President Trump Issues Directives to the SEC Targeting DEI and ESG Policies of Proxy Advisors

- Nasdaq Gets Discretionary Authority to Deny Initial Listings Based on Manipulation Risk

- Nasdaq Imposes Higher Float Thresholds for New Listings under its Net Income Standard

- New Nasdaq Rules Align de SPAC Listings Involving OTC Trading SPACs with IPO Treatment

- SEC Approves Nasdaq Rule Mandating Accelerated Delisting and Trading Suspension for Persistently Low-Priced Securities

- Nasdaq Proposes New $5 Million “Market Value of Listed Securities” Continued Listing Standard

- Nasdaq Proposes 23-Hour Trading Day for Equity Securities and ETPs

- NYSE Proposes New Minimum Trading Price Standard for Listed Companies

- NYSE Follows Nasdaq’s Lead: Aligns de SPAC Listings Involving OTC Trading SPACs with IPO Treatment

- NYSE American Proposes Amendments to Initial Listing Standards

- ISS and Glass Lewis Issue Updated Proxy Voting Policies for the 2026 Proxy Season

- Court Approves Modifications to Ease Long-Standing Research Analyst Restrictions on Major Banks

SEC Developments

Shareholder Proposals for 2026 Proxy Season: SEC Staff to Consider Only No-Action Requests Challenging Propriety of Proposals under State Law

THE BOTTOM LINE

- For the 2026 proxy season, the Securities and Exchange Commission (the “SEC”) will not substantively review or respond to no-action requests by companies seeking to exclude shareholder proposals from their proxy materials other than requests on the basis that a shareholder proposal is not a proper subject for shareholder action under state corporate law.

- Companies intending to exclude shareholder proposals from their proxy materials must, however, still notify the SEC and proponents no later than 80 calendar days before filing a definitive proxy statement, as required by Rule 14a-8(j) under the Securities Exchange Act of 1934 (the “Exchange Act”).

- A company that desires a non-substantive “no objection” response from the SEC staff for the exclusion of a shareholder proposal on other bases must include a representation that it has a reasonable basis to exclude the proposal based on the provisions of Exchange Act Rule 14a-8, prior published guidance, and/or judicial decisions.

- In deciding whether to exclude a proposal on other bases, companies should seriously consider whether they have a reasonable basis to exclude the proposal bearing litigation risk in mind.

- ISS requires companies excluding proposals on ordinary business, substantial implementation, or conflicts-with-company proposal grounds to clearly explain their reasons for exclusion, and, in rare cases, a company’s failure to provide a clear and compelling argument for exclusion of a proposal may result in ISS recommending a vote against one or more agenda items, including a recommendation against appropriate directors.

THE DETAILS

On November 17, 2025, the SEC Division of Corporation Finance (the “Division”) released a statement indicating that it will not respond to no-action requests by companies seeking to exclude shareholder proposals from their proxy materials during the current proxy season (October 1, 2025 - September 30, 2026) other than requests under Rule 14a-8(i)(1) under the Exchange Act (i.e., requests intending to exclude a shareholder proposal on the basis that it is not a proper subject for shareholder action under state corporate law). According to the statement, the Division is taking this action to enable it to focus on clearing the large backlog of pending registration statements and other filings resulting from the October-November 2025 government shutdown and on the basis of the Division’s view that, other than with respect to no-action requests under Rule 14a-8(i)(1), there is a sufficient body of applicable guidance for companies and proponents to rely on.

The exception for no-action requests based on Rule 14a-8(i)(1) appears intended to encourage companies that may want to challenge precatory proposals (i.e., nonbinding proposals) on the ground that they are improper under state corporate law. Referring in a footnote to a speech by SEC Chair Atkins in October, which we discussed here, questioning the propriety of precatory proposals under state corporate law, the statement notes that “regarding the application of state law and Rule 14a-8(i)(1) to precatory proposals, the Division has determined that there is not a sufficient body of applicable guidance for companies and proponents to rely on . . . the Division will continue to express its views . . . until such time as it determines there is sufficient guidance.”

While the Division will not respond substantively to any company submissions for excluding shareholder proposals other than those on the basis of Exchange Act Rule 14a-8(i)(1), the statement notes that if a company includes with its Exchange Act Rule 14a-8(j) notification a representation that it has a reasonable basis to exclude a proposal based on the provisions of Exchange Act Rule 14a-8, prior published guidance, and/or judicial decisions, the Division will respond with a letter indicating that, based solely on the company’s or counsel’s representation, the Division will not object if the company omits the proposal from its proxy materials. According to the Division’s statement, the absence of prior staff response agreeing that there was some basis to exclude a particular type of proposal does not mean a reasonable basis cannot exist, and the existence of prior staff response disagreeing with a company’s view that a proposal may be excluded does not mean a reasonable basis cannot exist to exclude the same or a similar proposal. In deciding whether to exclude a proposal, companies should seriously consider whether they have a reasonable basis to exclude a proposal bearing litigation risk in mind. In addition, given ISS’s reaction to the change (discussed below), companies that choose to exclude a proposal should clearly explain their reasons for doing so.

Notwithstanding the change in the Division’s no-action process, companies intending to exclude shareholder proposals from their proxy materials must notify the SEC and proponents no later than 80 calendar days before filing a definitive proxy statement, as required by Exchange Act Rule 14a-8(j).

Reactions from ISS and Glass Lewis

In response to the Division’s new process, ISS updated its FAQs on Non-Compensation Procedures & Policies noting its expectations and possible actions when companies seek to exclude shareholder proposals based on three commonly used exclusionary bases: the ordinary business exclusion, the substantial implementation exclusion, and the conflicts-with-company proposal exclusion. In all these cases, ISS expects companies to clearly explain their reasons for excluding a proposal. Specifically, for the ordinary business exclusion, companies must also explain why they believe any relevant precedent (SEC or court) does or does not apply; for the substantial implementation exclusion, they must explain their reasons for any significant deviations of their relevant implemented practice from that proposed in the shareholder proposal; and, for the conflicts-with-company proposal exclusion, they must explain how the proposal conflicts with their own proposal. ISS further notes that, in certain cases, failure to present a clear and compelling argument for the exclusion of a proposal may be viewed as a governance failure, leading to ISS highlighting the exclusion for its client’s information through direct reference in its report, contentious flag at the proposal level, or, in rare cases, a recommendation to vote against one or more agenda items for the stockholder meeting (which may be individual directors, certain committee members or the entire board).

In its case, Glass Lewis noted in its 2026 Benchmark Policy Guidelines that its basic premise is that shareholders should be afforded the opportunity to vote on matters of material importance, stating that “the basic right of shareholders to file proposals is critical to the proper functioning of our system of corporate governance and in the best economic interest of all shareholders.” Its benchmark policy guidelines further notes that the SEC’s ongoing changes and their ramifications will be closely monitored and that updates may be made to the benchmark policy guidelines before or during the 2026 proxy season should regulatory developments warrant or its approach changes.

SEC Chair Atkins Solicits Comments to Reform Regulation S-K

In January 2026, SEC Chair Atkins issued a statement inviting the public to provide comments on “how the [SEC] can amend Regulation S-K, with the goal of revising the requirements to focus on eliciting disclosure of material information and avoid compelling the disclosure of immaterial information,” noting that he has instructed the SEC Division of Corporation Finance to engage in a comprehensive review of the regulation.

His request for comments is focused on requirements of Regulation S-K other than the executive compensation disclosure requirements in Item 402 of Regulation S-K, which were the focus of an SEC roundtable in June 2025. According to the statement, the SEC received over 70 unique comment letters on Item 402, and the SEC staff is currently evaluating those letters and preparing recommendations for revisions to Item 402.

In his statement, SEC Chair Atkins expressed his view that Regulation S-K has become unwieldy, stressing that the regulation does not always reflect information important to a reasonable investor as “[it] currently elicits both material and a plethora of indisputably immaterial information.”

Directors and Officers of FPIs Required to Begin Publicly Reporting Equity Ownership, Awards, and Transactions on March 18, 2026

THE BOTTOM LINE

- Beginning on March 18, 2026, directors and officers of foreign private issuers (“FPIs”) with equity securities registered under the Exchange Act will be required to publicly file reports under Section 16(a) of the Exchange Act relating to holdings of, and transactions in those securities—the same reports (Forms 3, 4 and 5) long required for officers and directors of domestic issuers.

- Directors and officers of FPIs will, however, not be subject to the risk of short-swing profit disgorgement under Section 16(b) of the Exchange Act or restrictions on short sales under Section 16(c).

- Unlike the rules for domestic issuers, securityholders that beneficially own more than 10% of a registered class of equity of an FPI will not be subject to reporting obligations.

THE DETAILS

Beginning on March 18, 2026, directors and officers of FPIs with equity securities registered under the Exchange Act will be required to publicly file reports under Section 16(a) of the Exchange Act. These reports are the same as those long required for officers and directors of domestic issuers. This new requirement is mandated by the “Holding Foreign Insiders Accountable Act” (the “HFIAA”), a small section of the much larger and wide-ranging National Defense Authorization Act for Fiscal Year 2026.

The HFIAA grants the SEC the authority to grant individual or class-based exemptions from its requirements if the SEC determines that the laws of a foreign jurisdiction apply substantially similar requirements. Until and unless the SEC exercises that exemption authority, the new reporting requirements will apply to directors and officers of all FPIs, including Canadian companies reporting under the Multijurisdictional Disclosure System.

The Reporting Obligations

The HIFAA’s reporting obligations include:

- Reports due on March 18, 2026, for incumbent directors and officers of FPIs. For persons that are directors or officers of FPIs on March 18, 2026, a Form 3 will be due on that date. Form 3s disclose a person’s holdings of equity securities and derivatives of equity securities of the issuer, such as stock options, and include holdings of both American Depositary Receipts and underlying equity securities.

Holdings through trusts, by certain immediate family members and through personal investment vehicles will also often need to be disclosed.

- Reports for new directors, officers, or newly registered FPIs. Beginning on March 18, 2026, a Form 3 will be due 10 calendar days after a person becomes a director or officer. If an FPI registers its equity securities after March 18, 2026, its existing directors and officers must file a Form 3 on the date of registration.

- Reporting of transactions. Beginning on March 18, 2026, a Form 4 will be required within two business days of any transaction by the director or officer in the FPI’s equity securities or derivatives thereof. This includes open-market transactions, grants of equity compensation, option exercises, and gifts. Transactions are reportable even if effected under a 10b5-1 plan, an effective registration statement, or offshore.

Transactions through trusts, by certain immediate family members and through personal investment vehicles will also often need to be disclosed.

- Deferred transaction reporting. In very limited circumstances, directors and officers of FPIs may be eligible to report specific transactions on a Form 5, which is due 45 days after the company’s fiscal year-end, instead of on a Form 4.

Differences from Section 16 Regime for Domestic Issuers

While the HFIAA imposes meaningful new reporting obligations on directors and officers of FPIs, it does not subject FPIs to the entirety of the Section 16 regime. Importantly:

- The HFIAA does not directly impose trading restrictions on directors and officers of FPIs. Critically, the HFIAA does not subject directors and officers of FPIs to the risk of short-swing profit disgorgement under Section 16(b) of the Exchange Act or restrictions on short sales under Section 16(c). This is a significant difference from the long-standing Section 16 regime applicable to directors, officers, and certain significant shareholders of domestic issuers. In other words, while it imposes important new public reporting obligations, the HFIAA does not directly create new restrictions on trading by directors and officers of FPIs.

- The HFIAA does not apply to 10% securityholders. Unlike the rules for domestic issuers, where securityholders that beneficially own more than 10% of a registered class of equity are subject to Section 16, the HFIAA’s reporting obligations apply only to directors and officers of FPIs.

However, a subset of investors may still be captured by the HFIAA. An investor can be treated as a director and become subject to Section 16 if that investor has “deputized” another person to serve on a company’s board of directors. Whether an investor has become a “director by deputization” is a facts-and-circumstances inquiry. While not express in the text of the HFIAA, the caselaw and guidance around “director by deputization” may apply equally in this context, resulting in such investors having reporting obligations under the HFIAA.

Practical Steps for FPIs

There are a few key steps FPIs should take to prepare for these new reporting obligations:

- Educate directors and officers about the new public disclosure requirements. For many directors and officers of FPIs, the need to publicly disclose personal holdings and transactions will be new and potentially sensitive. Individuals may need time to prepare for these disclosures, which could influence the timing of their transactions.

- Make sure the list of officers is current. The definition of “officer” is in part a functional definition, rather than one that just relies on titles or corporate formalities and can require some judgment to ensure the right list of persons is included. That said, the definition is substantially very similar to the definition of “executive officer” used in the compensation clawback rule (Exchange Act Rule 10D-1) recently adopted by the SEC. As such, many FPIs already have experience applying that definition.

- Obtain EDGAR codes for officers and directors. Directors and officers will need their own SEC filing codes to make the filings required by the HFIAA. Obtaining these codes can often take several days or longer. If directors and officers do not currently have filing codes, FPIs should plan to obtain them well in advance of March 18, 2026.

- Establish a filing process. Directors and officers typically grant a power of attorney to internal counsel to execute Section 16 reports on their behalf. The filings are then prepared by internal counsel (or, in some cases, by external counsel, especially for initial or complex filings). FPIs should determine who will be granted the power of attorney and whether filings will be drafted by internal or external counsel. If internal counsel will draft filings, FPIs should ensure their teams have received appropriate training and have access to the necessary systems or service providers to submit filings to the SEC.

- Prepare initial Form 3s. Gather all relevant information for Form 3s of incumbent directors and officers and prepare the Form 3s in readiness for filing on March 18, 2026.

SEC Staff Updates Guidance on Proxies, Integration of Offerings, Regulation D Offerings, and Exchange and Tender Offers

On January 23, 2026, the staff of the SEC Division of Corporation Finance issued a series of interpretive guidance in the form of Compliance & Disclosure Interpretations (“C&DIs”) covering rules under the Securities Act of 1933 (the “Securities Act”) and the Exchange Act, as applicable, relating to (i) proxies, proxy materials, and information statements, (ii) the integration of securities offerings, (iii) private placements under Regulation D, (iv) historical compensation information for a spun-off company, (v) registered exchange offers, and (vi) tender offers.

We summarize the main points from the staff’s guidance below.

PROXY RULES

Revised Questions 126.06 & 126.07 (Proxy Rules C&DIs)

- The revised guidance reverses the staff’s position on the voluntary submission of Notices of Exempt Solicitation under Exchange Act Rule 14a-6(g). Exchange Act Rule 14a-6(g) requires any person who engages in an exempt solicitation in respect of any security and beneficially owns more than $5 million of the security to file a notice with the SEC attaching all written soliciting materials. Previously, the staff did not object to the voluntary submission of such notices by persons who did not satisfy the beneficial ownership threshold. The revised guidance now states, however, that the staff will object to a voluntary submission of such notice. According to the guidance, the staff is reversing its position because the vast majority of such notices have been voluntary submissions made primarily to generate publicity.

New Question 133.02 (Proxy Rules C&DIs)

- The staff will not object if a registrant conducts its “broker search” less than 20 business days before the record date of the applicable meeting of stockholders, provided that the registrant reasonably believes that its proxy materials will be timely disseminated to beneficial owners and otherwise complies with Exchange Act Rule 14a-13. The staff noted that, because of technological advancements, the “broker search” process can often be completed in less than 20 business days before the record date.

New Question 182.01 (Proxy Rules C&DIs)

- A registrant’s failure to comply with Exchange Act Rule 14c-2’s requirement to distribute an information statement to its stockholders at least 20 calendar days before any corporate action that is approved by its stockholders by written consent or authorization without its solicitation may be taken does not invalidate the corporate action.

- Where the written consents were solicited by a dissident stockholder without the registrant’s knowledge, the staff will not object to the registrant’s failure to comply with the 20-calendar-day requirement as long as the registrant distributes the information statement as soon as practicable after it becomes aware of the written consents.

INTEGRATION OF SECURITIES OFFERINGS

Withdrawn Guidance

The staff withdrew 10 of its prior guidance relating to the integration of securities offerings because they have been superseded by the extensive amendments to Securities Act Rule 152 (governing integration), which became effective in March 2021. The withdrawn guidance were issued at various times before 2021—in 2008, 2009, 2016 and 2017.

New Question 148.01 (Securities Act Rules C&DIs)

- An issuer that solicited various individuals through general solicitations in an offering under Rule 506(c) of Regulation D under the Securities Act, may subsequently sell to those individuals through an offering under Rule 506(b) of Regulation D, which does not permit general solicitations, if the issuer established a substantive relationship with those individuals prior to the commencement of the Rule 506(c) offering.

- In analyzing whether a substantive relationship exists, the quality of the relationship between an issuer (or its agent) and a prospective investor is the most important factor.

- In establishing a substantive relationship with a prospective investor, the issuer (or its agent) must have sufficient information to evaluate and must, in fact, evaluate the investor’s sophistication, financial circumstances, and ability to understand the nature and risks of the securities to be offered.

- Such relationship cannot be established solely by passage of a specific time or a particular short form accreditation questionnaire.

- In the absence of a prior business relationship or a recognized legal duty to offerees, it is likely more difficult for an issuer to establish a pre-existing, substantive relationship, especially when contemplating or engaged in an offering over the internet.

New Question 148.02 (Securities Act Rules C&DIs)

- The effectiveness of a registration statement, in and of itself, does not raise integration concerns under Rule 152.

New Question 148.03 (Securities Act Rules C&DIs)

- An issuer that is unsuccessful in completing a shelf takedown may complete the offering privately under Securities Act Section 4(a)(2) or Rule 506(b) so long as the issuer complies with the general integration principle in Rule 152(a)(1) (i.e., the issuer reasonably believes that it either did not solicit any purchaser in the private offering through general solicitation or established a substantive relationship with the purchaser prior to the commencement of the private offering).

REGULATION D

New Question 260.39 (Securities Act Rules C&DIs)

- An issuer may use different verification methods in the same Rule 506(c) offering (including the methods specified in Rule 506(c)(2)(ii) or principles-based methods of verification) to verify the accredited investor status of different investors.

HISTORICAL ITEM 402(A) EXECUTIVE COMPENSATION DISCLOSURE - SPUN-OFF COMPANIES

Revised 217.01 (Regulation S-K C&DIs)

- The staff made a slight clarification on the analysis required in the context of a spin-off in determining whether historical compensation information under item 402 of Regulation S-K is required for a spun-off registrant. The C&DI states that the analysis must focus on whether, before the spin-off, the spun-off registrant operated as a separate division or standalone business (prior guidance had referred to “separate division” or “reporting company”) and, if so, whether there was continuity of management.

- The revised guidance also clarifies that when historical compensation disclosure is not required, only the compensation awarded to, earned by, or paid to the spun-off registrant’s named executive officers in connection with and following the spin-off needs to be disclosed.

EXCHANGE OFFERS

Revised Questions 139.29 and 139.30 (Securities Act Sections C&DIs)

- To align with its approach in the context of offers and sale of securities in acquisitions, the revised guidance expands the circumstances under which the staff will not object to registered exchange offers that are preceded by lock-up agreements (or agreements to tender) executed by some of the holders of the securities subject to the exchange offer.

- In general, the revised guidance, which was previously limited to registered debt exchange offers, now extends to all registered exchange offers on Form S-4 (or Form F-4).

- The prior guidance provided for certain conditions (the “default conditions”) under which the staff will not object, including that the agreements are executed only by accredited investors, the exchange offer is made to all holders of the relevant securities, and all security holders eligible to participate in the exchange offer are offered the same amount and form of consideration.

- The revised guidance states that the agreements may be executed by accredited investor or qualified institutional investors.

- More importantly, beyond permitting such exchange offers when the default conditions are satisfied, the staff will also not object to such exchange offers if:

- the accredited investors or qualified investors who executed the agreements will be offered and sold securities only in a Securities Act exempt offering; and

- the registered securities will be offered and sold only to the security holders who did not execute the agreements.

TENDER OFFERS

New Question 166.02 (Tender Offer Rules C&DIs)

- The staff clarified that Exchange Act Rule 14e-5(b)(10)—which allows purchases or arrangements to purchase the relevant securities to be made outside of a Tier 1 cross-border tender offer provided, among other conditions, the U.S. offering document prominently discloses the possibility of, or the intent to make, such purchases or arrangements—is available for such purchases or arrangements to purchase outside a Tier 1 tender offer that are made after the announcement of the tender offer but before offering documents are disseminated.

- The offering documents, when disseminated, should disclose that purchases outside the Tier 1 offer have already occurred and, if true, may continue during the tender offer.

New Question 166.03 {Tender Offer Rules C&DIs)

- The condition that purchases of the relevant securities by the affiliate of the offeror’s financial advisor outside a tender offer may not be made to facilitate the tender offer only applies to purchases made by the affiliate when the affiliate is not acting as a purchase agent of the offeror.

In Executive Order, President Trump Issues Directives to the SEC Targeting DEI and ESG Policies of Proxy Advisors

THE BOTTOM LINE

Among other directives, President Trump has directed the SEC to (i) review and consider revising or rescinding all SEC rules and guidance relating to proxy advisors (including Exchange Act Rule 14a‑8, the SEC’s shareholder proposal rule), especially where they implicate ESG or DEI, and (ii) examine whether investment advisers’ engagement of proxy advisors to advise on non‑pecuniary factors in investing (including ESG/DEI) is inconsistent with their fiduciary duties.

THE DETAILS

On December 11, 2025, President Donald Trump issued an Executive Order mandating a number of regulatory actions aimed at curtailing the influence of proxy advisors over U.S. public companies, particularly their influence over diversity, equity, and inclusion (“DEI”), and environmental, social, and governance (“ESG”) matters, which the Order refers to as “radical politically-motivated agendas” advanced and prioritized by proxy advisors over investor returns. The Order appears targeted at two prominent proxy advisors, Institutional Shareholder Services, and Glass Lewis, who are the only proxy advisors specifically referred to in the Order. The Order asserts that both firms “play a significant role in shaping the policies and priorities of America’s largest companies through the shareholder voting process” and “control more than 90 percent of the proxy advisor market” and states that the United States must “increase oversight of and take action to restore public confidence in the proxy advisory industry.” While the Order also includes directives for the Federal Trade Commission (“FTC”) and the Department of Labor, its most immediate market implications stem from directives to the SEC.

We summarize the Order’s directives below.

Directives to the SEC

The Order directs the SEC Chair to:

- Review and consider revising or rescinding all SEC “rules, regulations, guidance, bulletins, and memoranda relating to proxy advisors,” especially where they implicate ESG or DEI;

- Consider revising or rescinding rules and guidance on shareholder proposals, specifically including Exchange Act Rule 14a‑8, the SEC’s shareholder proposal rule, where inconsistent with the Order’s purpose;

- This directive aligns with the SEC Chair’s Spring 2025 rulemaking agenda, which envisages modernization of the shareholder proposal regime, as well as the SEC Chair’s recent speeches.

- Enforce the federal securities laws’ anti‑fraud provisions with respect to material misstatements or omissions in proxy advisors’ recommendations;

- Assess whether proxy advisors should be required to register as investment advisers;

- Consider requiring increased transparency from proxy advisors regarding their recommendations, methodologies, and conflicts of interest, with specific focus on ESG/DEI factors;

- Analyze whether proxy advisors facilitate coordination of voting decisions among investment advisers sufficient to form a “group” for purposes of beneficial share ownership reporting requirements under Sections 13(d)(3) and 13(g)(3) of the Exchange Act; and

- Direct SEC staff to examine whether investment advisers’ engagement of proxy advisors to advise on non‑pecuniary factors in investing (including ESG/DEI) is inconsistent with their fiduciary duties.

Other Directives

As regards the FTC, the Order directs the FTC Chair, in consultation with the Attorney General, to investigate whether any federal liability arises from conduct underlying certain state antitrust investigations into proxy advisors, and whether proxy advisors engage in unfair methods of competition or unfair or deceptive acts or practices that harm consumers, including by failing to adequately disclose conflicts of interest and undermining consumers’ ability to make informed choices.

The Order also tasks the Secretary of Labor with revising all regulations and guidance regarding the fiduciary status of proxy advisors in relation to proxy voting and other rights of shares of plans covered by the Employee Retirement Income Security Act of 1974 (“ERISA plans”), specifically whether a proxy advisor is an investment advice fiduciary under ERISA. The Secretary of Labor has also been directed to assess whether proxy advisors act solely in the financial interests of ERISA plans.

Nasdaq Gets Discretionary Authority to Deny Initial Listings Based on Manipulation Risk

THE BOTTOM LINE

- Nasdaq may now block initial listings of securities for qualitative reasons unrelated to misconduct by the issuer or regulatory misconduct by related individuals—even where an issuer meets all quantitative and qualitative listing standards—if qualitative indicators suggest that the security could be particularly susceptible to manipulative or unusual trading.

- In exercising this new discretion, Nasdaq may consider various factors, including considerations relating to the issuer’s advisors, issues identified with previously listed, similarly situated issuers, regulatory and other issues related to the issuer’s jurisdiction of location, liquidity and security concentration concerns, and going concern issues.

THE DETAILS

In December 2025, the SEC approved a Nasdaq rule proposal that gives the exchange limited discretion to deny initial listings—even where an applicant meets all quantitative and qualitative standards—if qualitative indicators suggest that the security could be particularly susceptible to manipulative or unusual trading. The proposal was driven by Nasdaq’s observation of problematic or unusual trading in certain recently listed companies and by a series of SEC trading suspensions that were based on concerns that unknown persons were using social media to recommend securities in an effort to artificially inflate their price and volume. In most cases, the securities subject to the suspension orders had been listed for less than one year, and there were no specific allegations that the companies themselves were involved in the manipulative activity. Because Nasdaq’s rules did not give Nasdaq discretion to deny listings based on potential misconduct by unaffiliated third parties or based on trading patterns observed in similarly situated companies—they only gave Nasdaq the discretion to deny listings in certain circumstances involving issuer misconduct or associations with individuals who have a history of regulatory misconduct—the rule was proposed to address this gap.

In exercising its discretion under the new rule, IM‑5101‑3, Nasdaq may take into account considerations relating to the company’s advisors (e.g., auditors, underwriters, law firms, brokers, clearing firms, and other professional service providers) or concerns Nasdaq has identified with previously listed, similarly situated companies. The rule also authorizes Nasdaq to deny initial listings based on a non-exclusive set of factors designed to identify securities that may be susceptible to manipulation. These factors include: where the company or persons exercising substantial influence over it are located, including the availability of legal remedies to U.S. shareholders in that jurisdiction, potential enforcement challenges facing regulators in that jurisdiction (including due to laws such as blocking statutes and data privacy laws), the ability to conduct comprehensive due diligence in that jurisdiction, and the transparency of regulators in that jurisdiction; whether the expected public float and share distribution raise concerns about liquidity or concentration; whether the company’s advisors have regulatory histories or were involved in prior transactions that became subject to concerning or volatile trading; whether the company’s management and board have experience with U.S. public company requirements; whether there are FINRA, SEC or other regulatory referrals related to the company or its advisors; whether the company has, or has recently had, a going concern audit opinion (and, if so, the company’s plan to continue as a going concern), and whether there are other factors that raise concerns about the integrity of the company’s leadership, significant shareholders or advisors.

If Nasdaq staff denies a listing application under this discretionary authority, they will issue a written determination explaining the basis for the decision. The company must then publicly announce its receipt of the determination and the specific concerns identified by Nasdaq within four business days and may seek review by a Nasdaq hearings panel within seven calendar days of the denial.

In light of the new rule, which became effective on December 12, 2025, issuers should proactively review their advisor selection and histories, float construction and distribution mechanics, governance readiness, and jurisdictional transparency, among other matters that may pose a problem under the rule.

Nasdaq Imposes Higher Float Thresholds for New Listings under its Net Income Standard

On December 18, 2025, the SEC approved a Nasdaq rule change that increases the minimum market value of unrestricted publicly held shares for companies seeking to list based on net income to $15 million across both the Nasdaq Global and Nasdaq Capital Markets. The previous threshold was $8 million and $5 million, respectively, for the Nasdaq Global and Nasdaq Capital Markets. This change would align the float requirement for the net income pathway with the thresholds already applicable to other initial listing standards, addressing Nasdaq’s observation that lower public floats have contributed to thin trading and impaired price discovery.

New Nasdaq Rules Align de‑SPAC Listings Involving OTC‑Trading SPACs with IPO Treatment

The SEC has approved amendments to Nasdaq’s initial listing standards for special purpose acquisition companies (“SPACs”) completing business combinations (“de‑SPAC transactions”). The rule amendments are aimed at harmonizing the treatment of SPACs that trade over‑the‑counter (“OTC”) with those already listed on a national securities exchange. Under the new rules, an OTC-traded SPAC that was previously listed on a national securities exchange and is listing in connection with a de‑SPAC transaction in connection with an effective Securities Act registration statement would be evaluated as the functional equivalent of an IPO so long as the SPAC, as is typical, provides its public shareholders redemption rights in connection with the de-SPAC transaction in exchange for a pro rata share of the IPO proceeds and concurrent sale by the SPAC of equity securities. To achieve this, the new rules exclude such listings from legacy “reverse merger” seasoning concepts that were designed to address back‑door registrations, recognizing that de‑SPACs with an effective registration statement entail Securities Act disclosure, SEC staff review, and underwriter involvement and diligence akin to a traditional IPO. Nasdaq rules already exclude de-SPACs by listed SPACs from those “reverse merger” seasoning concepts.

The new rules also make inapplicable to such listings the pre‑listing average daily trading volume thresholds that otherwise apply to issuers uplisting from the OTC market. According to Nasdaq, that liquidity requirement is a poor proxy in this context since pre‑combination trading in a SPAC is generally linked to the SPAC’s trust value and redemption features and therefore is not indicative of post‑combination trading dynamics in the operating company.

Importantly, the post‑combination company would still be required to satisfy all other initial listing standards, including quantitative criteria related to public float, investor distribution, and price. The new rules create a more predictable path to exchange listing at the time of a de‑SPAC for OTC‑traded SPACs that were previously listed on a national securities exchange, aligning Nasdaq’s standards with the SEC’s view of de‑SPACs as IPO‑equivalents from an investor‑protection and disclosure standpoint.

The new rules became effective upon approval by the SEC on December 8, 2025.

SEC Approves Nasdaq Rule Mandating Accelerated Delisting and Trading Suspension for Persistently Low-Priced Securities

On December 5, 2025, the SEC approved Nasdaq rule amendments that would significantly tighten the application of its minimum bid price framework for severely distressed securities. Under the rule, if a listed security closes at $0.10 or less for 10 consecutive business days, Nasdaq will promptly issue a staff delisting determination without affording the compliance periods otherwise available for bid-price deficiencies. Unlike under the prior rules, this would apply even if the company has not had a closing bid price below $1.00 for 30 consecutive days. The change is intended to address rapid price deterioration that Nasdaq views as indicative of substantial financial or operational distress and to move more quickly to remove such securities from the exchange in the interest of investor protection and market integrity.

The proposal would also alter the procedural posture during appeals. A company that receives a delisting determination for falling below the $0.10 threshold would see its securities suspended from trading on Nasdaq during the pendency of any appeal to a hearings panel, rather than benefiting from an automatic stay; during suspension, the securities would trade in the over-the-counter market. A hearings panel would retain discretion to grant a limited exception period and could reinstate trading if it determines that the issuer meets applicable standards, which may be demonstrated by sustaining the requisite bid price for at least 10 consecutive business days, subject to staff’s discretion to extend that period.

The rule took effect on January 19, 2026, 45 days after Commission approval. The new framework would apply prospectively to companies that have not already received a delisting determination for a bid-price deficiency and have appeared before a hearings panel by January 19, 2026, preserving the status quo for those already within the panel’s jurisdiction.

Nasdaq Proposes New $5 Million “Market Value of Listed Securities” Continued Listing Standard

On January 13, 2026, Nasdaq filed a proposed rule change with the SEC to adopt a new continued listing standard that would require companies listed on the Nasdaq Global Market (and the Global Select Market) and Nasdaq Capital Market to maintain a minimum “market value of listed securities” of at least $5 million. Under the proposal, a company that fails to meet this threshold for a period of 30 consecutive business days would be subject to immediate suspension and delisting; that is, that company will not be afforded the customary cure or compliance periods typically provided under Nasdaq’s rules. According to Nasdaq, the proposal is intended to enhance investor protections by removing from Nasdaq companies that the market has identified as facing severe and likely insurmountable challenges, as evidenced by their sustained low market valuations. Furthermore, Nasdaq observed in its proposal that such companies are generally unable to regain and sustain compliance with listing requirements and that their continued trading on the exchange poses difficulties for market makers seeking to maintain fair and orderly markets.

Nasdaq also proposes to modify its hearings and appeals regime so that a timely hearing request would not stay the trading suspension for these cases, meaning the security would generally trade over-the-counter while the appeal is pending. In addition, the proposal would limit the hearings panel’s discretion in these matters to effectively a factual-error review—permitting the panel to reverse a delisting decision only upon a finding that the staff delisting determination was issued in error in that the company never actually failed to meet the requirement—while prohibiting the panel from considering regained compliance or granting an exception period to cure. The SEC is expected to act on the proposal by March 15, 2026.

Nasdaq Proposes 23-Hour Trading Day for Equity Securities and ETPs

On December 29, 2025, Nasdaq filed a proposed rule change with the SEC to permit trading of equity securities and exchange-traded products on the exchange on a near-continuous basis: 23 hours per day, five days per week. The proposal is designed to accommodate rising investor demand for overnight trading—particularly among international investors located in jurisdictions (such as Asia) whose business hours do not align with traditional U.S. market hours—and to better position Nasdaq to compete with certain alternative trading systems already offering overnight trading. Under the proposal, Nasdaq would create a new “Night Session” (9:00 p.m. to 4:00 a.m. ET) that would operate alongside a consolidated “Day Session” (4:00 a.m. to 8:00 p.m. ET) (comprising the existing Pre-Market, Regular Market, and Post-Market trading periods). The exchange would pause trading for one hour each weekday between 8:00 p.m. and 9:00 p.m. ET to conduct maintenance, process corporate actions, and allow market participants to clear trades. The SEC approved similar proposals for extended trading by 24X and NYSE Arca in November 2024 and February 2025, respectively.

Nasdaq’s proposal establishes a framework for the night session that mirrors the limited functionality offered during existing extended-hours trading, including a reduced selection of order types and attributes. Under the proposal, Nasdaq member firms will be required to provide customers with enhanced risk disclosures addressing six additional potential risks associated with night session trading, including risks related to limited regulatory protections, limited trading alternatives, continuous trading, and the potential closure of financial market infrastructure companies during overnight hours. According to Nasdaq, certain issues—such as the full approach to trading halts for some corporate actions and the choice of volatility moderation mechanisms during the night session—would be addressed in an amendment to its filing or in a separate filing before the night session launch.

The SEC is expected to act on the proposal by February 27, 2026.

NYSE Developments

NYSE Proposes New Minimum Trading Price Standard for Listed Companies

The New York Stock Exchange (“NYSE”) has proposed an amendment to its rules that would establish a minimum trading price of $0.25 per share for listed securities. Under the proposed rule, if a security's closing price falls below $0.25 per share (the “minimum trading price”) on any trading day, the exchange would immediately suspend trading in the security and commence delisting proceedings. Unlike the exchange’s existing price criteria framework—which requires listed companies to maintain an average closing price of at least $1.00 over every consecutive 30-trading day period and permits a six-month cure period for securities that fall below that $1.00 threshold (but no right to submit a compliance plan)—securities that close below the minimum trading price would not be entitled to a cure period (and, similar to price criteria defaults, to submit a compliance plan), although issuers would retain the right to appeal a delisting decision. Although not codified in its rules, the exchange’s current practice is to immediately initiate suspension and delisting procedures when a stock trades below $0.10 per share. The proposal also clarifies that the NYSE retains its authority to suspend trading in or delist a security that has experienced a precipitous decline and is at an abnormally low level from which it is unlikely to recover, even if that security has not fallen below the minimum trading price.

According to the NYSE, the proposal responds to an increasing industry-wide trend of low-priced stocks trading on national securities exchanges, and the NYSE believes that such stocks have a greater potential of being manipulated or experiencing trading volatility because less capital is required to undertake manipulative trading activity. The NYSE further noted in its proposal that, in its experience, securities trading at abnormally low prices are typically unable to recover to any meaningful degree.

The NYSE has proposed an effective date of October 1, 2026 for the proposed standard to provide a transition period for impacted issuers to implement reverse stock splits or other measures to increase their share prices before the new standard takes effect. The SEC is expected to act on the proposal by March 17, 2026.

NYSE Follows Nasdaq’s Lead: Aligns de‑SPAC Listings Involving OTC‑Trading SPACs with IPO Treatment

Effective February 9, 2026, the SEC approved amendments to NYSE rules that harmonize the treatment of SPACs that trade over‑the‑counter (“OTC”) with those already listed on a national securities exchange by allowing OTC-traded SPACs that were previously listed on a national securities exchange and are listing in connection with a de‑SPAC transaction with an effective Securities Act registration statement to be evaluated as the functional equivalent of an IPO so long as they, as is typical for SPACs, provide their public shareholders redemption rights in connection with their de-SPAC transactions in exchange for a pro rata share of proceeds from their IPO and concurrent sale of their equity securities. The amendments are similar to those the SEC recently approved for Nasdaq, which we discuss above under “Nasdaq Developments— New Nasdaq Rules Align de‑SPAC Listings Involving OTC‑Trading SPACs with IPO Treatment.”

NYSE American Proposes Amendments to Initial Listing Standards

In January 2026, NYSE American proposed a rule change to amend its initial listing standards. Under the proposed rule, which is designed to ensure adequate liquidity for listed securities, all market value of publicly held shares requirements for initial listing would be recalculated on the basis of unrestricted publicly held shares only, meaning that securities subject to resale restrictions would no longer be counted toward a company’s liquidity calculations. Relatedly, the exchange is also proposing that companies listing in connection with an initial public offering or other underwritten public offering must have a market value of unrestricted publicly held shares of at least $15 million, satisfied solely from offering proceeds.

The proposed amendments, which are similar to Nasdaq’s rules, are intended to address concerns that securities with a substantial number of restricted shares may satisfy the exchange’s current initial listing liquidity requirements while having relatively few freely tradable shares, resulting in illiquid listings. In addition, the proposal would increase the minimum stock price required for initial listing from $2 or $3 per share (depending on the listing standard) to a uniform $4 per share, consistent with the initial listing requirements of the NYSE and Nasdaq Capital Market. For companies that are already publicly traded on the over-the-counter market or are transferring from another national securities exchange and seeking to list under the exchange’s Initial Listing Standards 3 or 4, the proposal would require that applicants meet the applicable total market capitalization and $4 minimum stock price requirements for 90 consecutive trading days prior to applying for listing.

The SEC is expected to act on the proposal by March 21, 2026.

Other Developments

ISS and Glass Lewis Issue Updated Proxy Voting Policies for the 2026 Proxy Season

ISS and Glass Lewis have issued their updated U.S. proxy voting policies for the 2026 proxy season. While ISS’s policies are effective for shareholder meetings held on or after February 1, 2026, Glass Lewis’s policies apply to shareholder meetings held after January 1, 2026. We summarize their key policy updates below.

ISS Key Policy Updates

Director Elections - Diversity Considerations Suspended. Until further notice, ISS will no longer consider gender and racial and/or ethnic diversity in its vote recommendations for director elections.

Problematic Capital Structure - Unequal Voting Rights. ISS’s policy has been updated to eliminate inconsistencies in the treatment of capital structures with unequal voting rights by considering them problematic regardless of whether superior voting shares are classified as “common” or “preferred.” The policy, however, includes new exceptions for:

- Convertible preferred shares that vote on an “as-converted” basis; and

- Enhanced voting rights with limited duration and applicability (e.g., where intended to overcome low voting turnout and ensure approval of a specific non-controversial agenda item and “mirrored voting” applies)

E&S-related Shareholder Proposals. ISS will now adopt a case-by-case approach for proposals on diversity, political contributions, human rights, and climate change. For diversity proposals, the change applies to proposals for disclosure of diversity policies/initiatives or workforce diversity data. ISS already applies a case-by-case approach to proposals for gender or race/ethnicity pay gap, and racial equity and/or civil right audits.

Long-Term Alignment in Pay-for-Performance Evaluation. The policy updates U.S. pay-for-performance quantitative screens to assess pay-for-performance alignment over a longer-term horizon, considering a five-year period instead of three years, while also maintaining an assessment of pay quantum over the short term.

Time-Based Equity Awards with Long-Term Time Horizon. The policy update reflects the importance of longer-term time horizons for time-based equity awards and provides for a more flexible approach in evaluating the equity pay mix in pay-for-performance qualitative reviews. ISS will no longer view a predominantly, or even entirely, time-based equity mix as inherently problematic if awards carry a sufficiently long-term horizon through extended vesting or post-vesting holding requirements.

Compensation Committee Responsiveness. The policy streamlines the language on this by removing duplicative factors for evaluating responsiveness to shareholder input on executive pay.

Company Responsiveness. The policy expands flexibility for companies to demonstrate responsiveness to low say-on-pay support, in light of recent SEC guidance on 13G vs. 13D filing status that may limit shareholder engagement. Where prior say-on-pay support fell below 70%, ISS will consider a company’s meaningful outreach efforts and the concrete pay program changes it adopted even if investors did not provide specific feedback.

High Non-Employee Director Pay. ISS’s policy on high non-employee director pay practices has been expanded to allow for adverse recommendations in the first year of occurrence if considered highly problematic, or when a pattern emerges across non-consecutive years. Problematic features include outsized director pay relative to peers or to executives, use of performance-based awards, retirement benefits, and excessive perquisites, especially without compelling rationale.

Enhancements to Equity Plan Scorecard. The policy adds a new scoring factor under the Plan Features pillar to assess whether plans that include non-employee directors disclose cash-denominated award limits and introduces a new negative overriding factor for equity plans found to be lacking sufficient positive features under the Plan Features pillar despite an overall passing score.

Glass Lewis Key Policy Updates

Mandatory Arbitration Provisions. The benchmark policy addresses provisions in governing documents requiring arbitration of investor claims arising under the federal securities laws (“mandatory arbitration provisions”).

- Like its policy on exclusive forum provisions, Glass Lewis will generally recommend a vote against a mandatory arbitration provision unless the company:

- provides compelling argument that it directly benefits shareholders;

- provides evidence of abuse of legal processes;

- narrowly tailors it to the risks involved; and

- maintains a strong record of good corporate governance practices.

- Glass Lewis may recommend a vote against governance committee members following the IPO (including direct listings) or spin-off of companies with highly restrictive governing documents that include a mandatory arbitration provision.

- Glass Lewis will consider the presence of a mandatory arbitration provision when evaluating whether a newly public company’s governing documents severely restrict shareholder rights indefinitely.

Shareholder Rights. A board’s adoption of the following may now result in a voting recommendation against the governance committee chair or the entire committee:

- Provisions limiting the submission of shareholder proposals;

- Provisions limiting the filing of derivative lawsuits; and

- Plurality voting standard for the election of directors instead of a majority voting standard.

Amendments to the Charter and/or Bylaws.

- The benchmark policy has been updated to note that proposed amendments to a company’s charter or bylaws will be evaluated on a case-by-case basis, with voting for amendments that are unlikely to have a material negative impact on shareholders’ interests generally recommended.

- Where several amendments are bundled under a single proposal, each proposed change will be analyzed individually, and the benchmark policy will recommend voting for the proposal only when, on balance, the amendments are in the best interests of shareholders.

- In such cases, material concerns with a single proposed amendment may lead to a recommendation against the proposed amendments.

Proposals to Eliminate Supermajority Voting. Company proposals seeking to eliminate supermajority voting requirements will be evaluated on a case-by-case basis, considering shareholder structure, quorum requirements, impending transactions—involving the company or a major shareholder—and any company internal conflicts, among other factors.

General Approach to Shareholder Proposals. Given ongoing changes and the prospects of additional changes to the shareholder proposal process, Glass Lewis notes that its benchmark policy may be updated prior to or during the 2026 proxy season should its approach to shareholder proposals change or regulatory developments warrant such an update. The policy, however, restates Glass Lewis’s basic premise that shareholders should be allowed to vote on matters of material importance.

Pay-for-Performance Methodology.

- Glass Lewis’s proprietary pay-for-performance model has been updated. Rather than a single letter grade of “A” through “F,” the model will use a scorecard-based approach, consisting of up to six tests. Each test will receive a rating, which will be aggregated on a weighted basis to determine an overall score ranging from 0 to 100.

- The six tests are: (i) Granted CEO Pay vs. TSR; (ii) Granted CEO Pay vs. Financial Performance, (iii) CEO STI Payouts vs. TSR; (iv) Total Granted NEO Pay vs. Financial Performance; (v) CEO Compensation-Actually-Paid vs. TSR; and (vi) Qualitative Factors (Downward Modifiers).

- Changes that materially reduce or eliminate performance vesting will be assessed case-by-case and could be viewed negatively if not paired with meaningful improvements elsewhere in the long-term incentive design.

Court Approves Modifications to Ease Long-Standing Research Analyst Restrictions on Major Banks

On December 16, 2025, the United States District Court for the Southern District of New York approved modifications to certain long-standing restrictions placed on major investment banks in the early 2000s as part of a court settlement (commonly referred to as the “global research settlement”) with the SEC. The restrictions, which were designed to address alleged conflicts of interest between the firms’ equity research and investment banking arms, included a communications firewall between the two arms.

The court’s approval was in response to motions filed by several of the major banks party to the global research settlement—and unopposed by the SEC—requesting that they be released from certain of the restrictions under the global research settlement. In their motions, the banks argued that those restrictions were no longer necessary because comprehensive, industry-wide regulation—principally Rule 2241 of the rules of the Financial Industry Regulatory Authority, which was adopted in 2015—now addresses the very conflicts of interest those restrictions were designed to manage, noting that the global research settlement itself anticipated this outcome by presuming modification once such rules were adopted. The banks further argued that, after a decade of effective enforcement of FINRA Rule 2241, maintaining a parallel, settlement-specific regime for only the banks party to the global research settlement creates a fractured framework that imposes unnecessary burdens and costs without corresponding investor protection benefits.

The global research settlement imposes several prescriptive restrictions that FINRA Rule 2241 does not, most notably a blanket ban on direct communications between investment bankers and research analysts except for narrowly enumerated exceptions. For example, the banks noted that the following actions, which would not pose any relevant conflict of interest under FINRA Rule 2241, are barred under the global research settlement: (1) bankers asking analysts for purely ministerial information (such as dial-in details for a public research call); (2) bankers passively (i.e., in “listen only” mode) attending a research analyst call with company management; and (3) bankers facilitating or even alerting an analyst to an investor’s or corporate client’s request for an introduction or discussion. The banks further noted that while the global research settlement mandates communication rules that often require legal/compliance chaperoning, FINRA Rule 2241 uses a principles-based “information barriers and policies/procedures” approach that allows benign interactions so long as conflicts are effectively managed.

In a December 5, 2025 statement hailing the SEC’s consent to the modification, SEC Commissioner Mark Uyeda noted that “the [SEC] took an important step toward eliminating outdated and costly requirements on firms and improving the availability of equity research in our markets by agreement to amend the [global research settlement].”

U.S. Equity & Debt Markets Activity - 2025

(data sourced from Dealogic)

Traditional IPOs

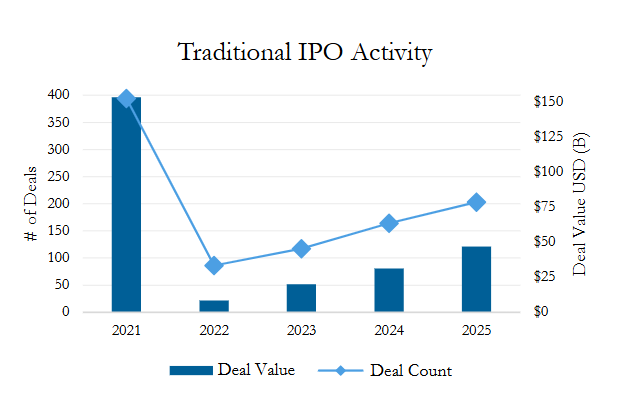

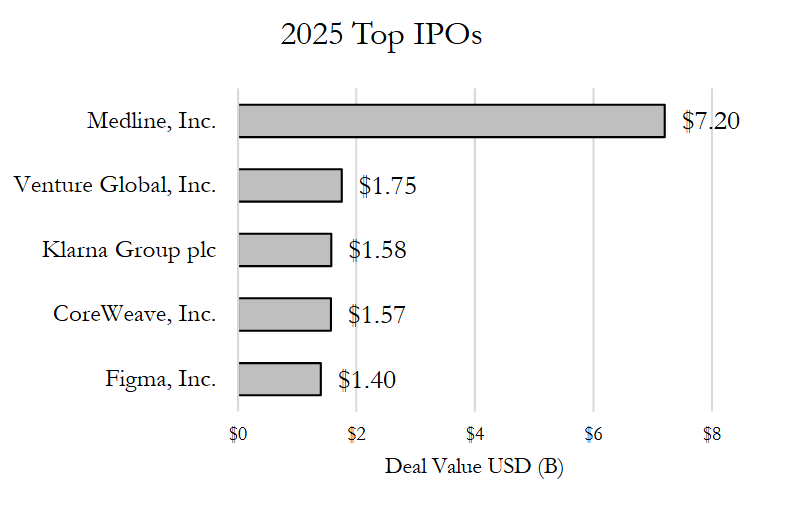

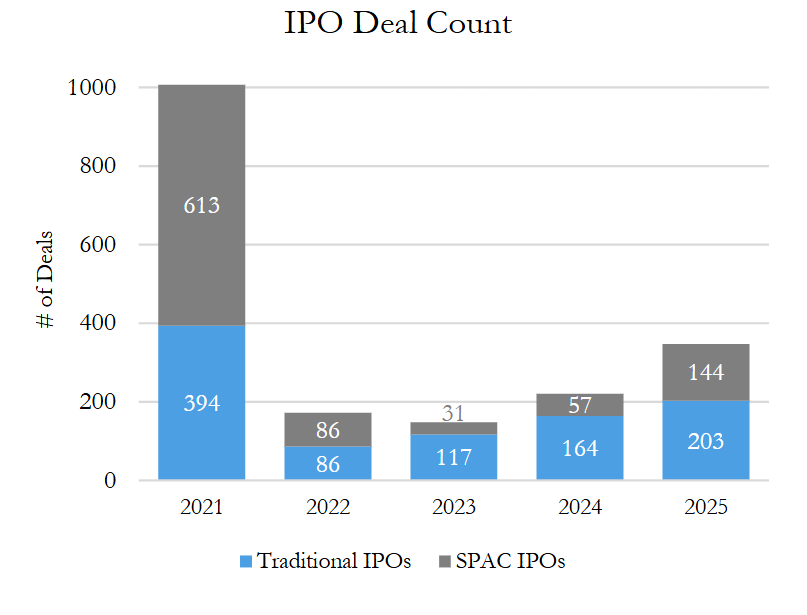

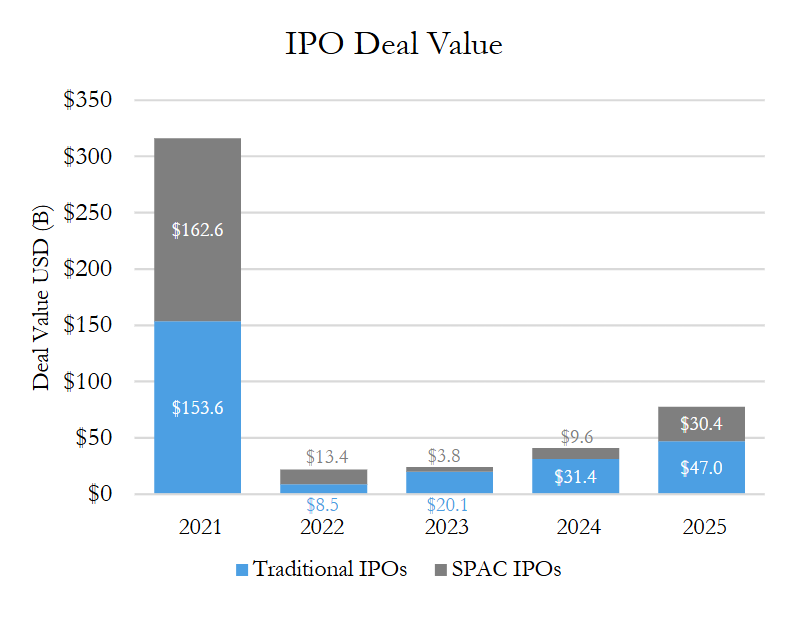

Traditional initial public offering (“IPO”) activity accelerated further in 2025, rising 50% by deal value and 24% by deal count from 2024 and continuing the streak of steadily increasing activity since 2022’s low. Just over 200 IPOs (about half of 2021’s record deal count) with nearly $50 billion in aggregate value priced in 2025, whereas 2024 saw 164 IPOs with $31.4 billion in deal value price. Overall, 2025 proved to be the strongest year since 2021, signaling a resurgence in new issues.

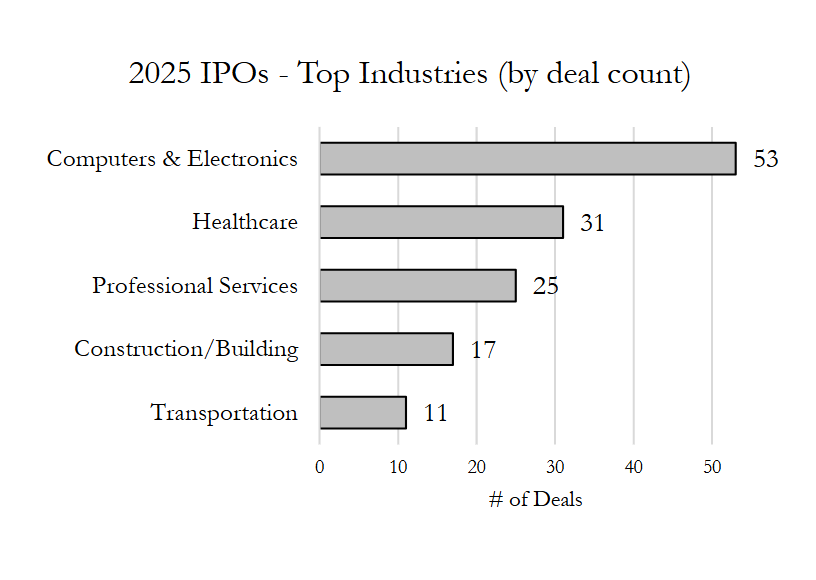

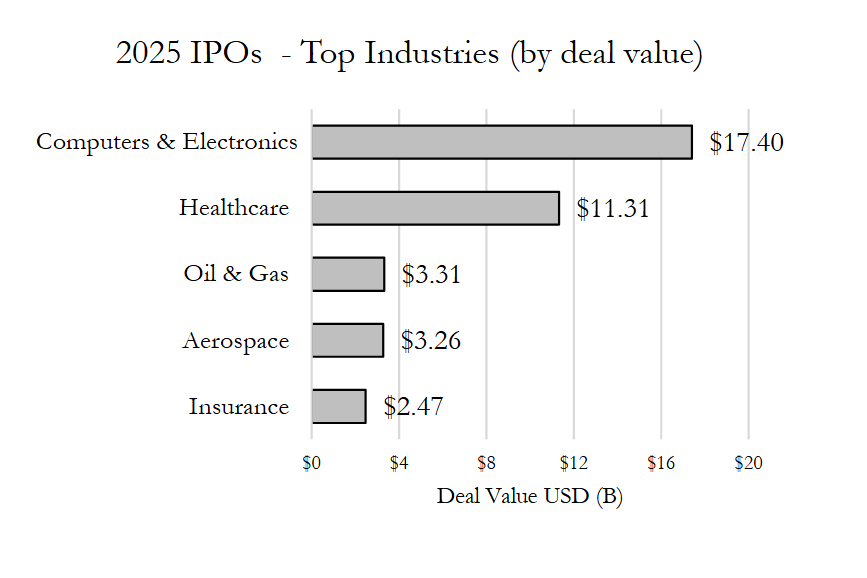

As with 2023 and 2024, technology and healthcare IPOs topped the charts in 2025, with technology leading with 53 IPOs raising a total of $17.4 billion followed by healthcare’s 31 IPOs totaling $11.3 billion proceeds. The largest IPO of the year—Medline’s $7.2 billion offering in December — accounted for 64% of the aggregate deal value for healthcare IPOs, while Klarna, CoreWeave and Figma (the third, fourth and fifth largest IPOs, respectively) collectively accounted for about a quarter of the aggregate deal value for technology IPOs. The professional services, construction and transportation industries also made a strong showing by volume, each with IPO counts in the double digits. The oil and gas, aerospace and insurance industries each priced several billion in IPO deal value, with Venture Global’s $1.75 billion IPO—2025’s second-largest IPO—placing the oil and gas industry in third place by deal value.

SPAC IPOs

IPOs by special purpose acquisition companies (“SPACs”) continued to surge in 2025, with deal value more than tripling (+215%) and deal count more than doubling (+153%) 2024’s numbers with 144 IPOs raising $30 billion in 2025. While still modest relative to traditional IPOs, 2025’s largest SPAC IPO—Drugs Made In America Acquisition II raising $500 million—was one of the largest since early 2022. Although activity remained only about one-fifth of 2021’s record count and value, overall, the continued strength in SPAC IPOs signals renewed investor interest and momentum after several quieter years, indicating the once popular mechanism is making a comeback.

Follow-Ons

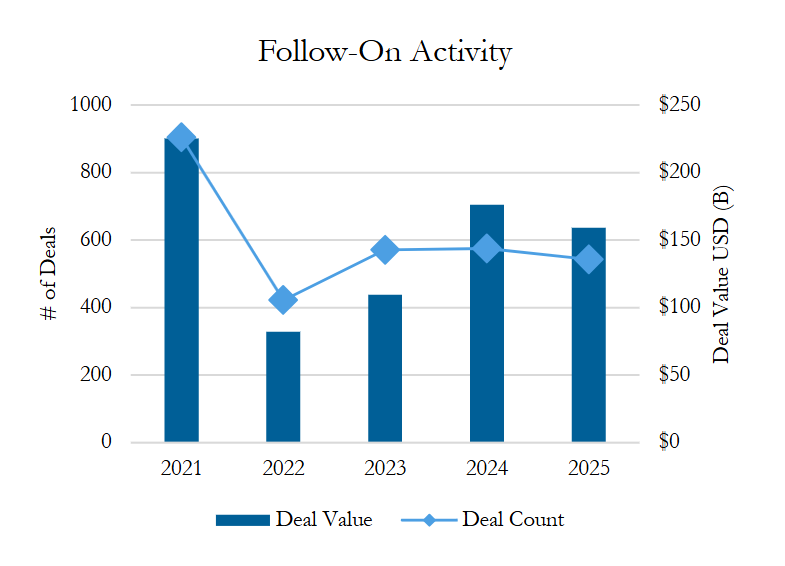

Follow-on activity dipped slightly in 2025, halting the upward trend since 2022. Compared to 2024, deal value was down 10% ($159 billion vs. $176 billion in 2024), while deal count was down 6% (543 vs. 575 offerings in 2024). Q1 2025 was especially low, with just over 100 offerings. Despite the decrease, follow-ons remained historically strong, up 94% by value and 29% by count from 2022’s record low.

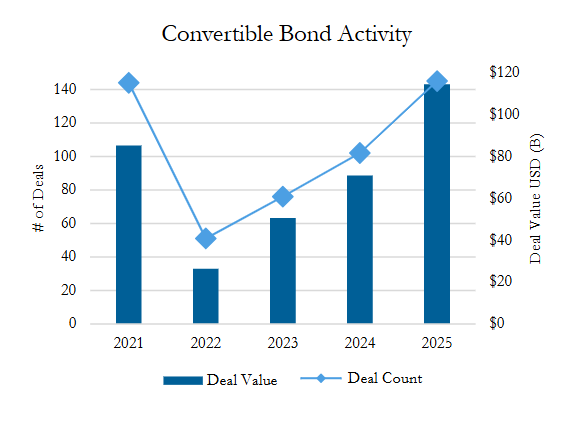

Convertible Bonds

In 2025, the convertible bond market recorded its most impressive year yet by deal value with $114 billion priced, surpassing 2020’s previous record. From deal counts in the last decade, the 145 convertible bond offerings in 2025 were second only to 2020’s record 170 deals and surpassed 2021 by one deal. Up 61% by deal value and 42% by deal count from 2024, 2025 continued the momentum since 2022’s low. Notably, issuance skewed to the second half of the year, with 90 offerings in the second half of 2025 compared to 55 in the first half, a reversal of the usual seasonal pattern observed in prior years.

Investment-Grade Debt

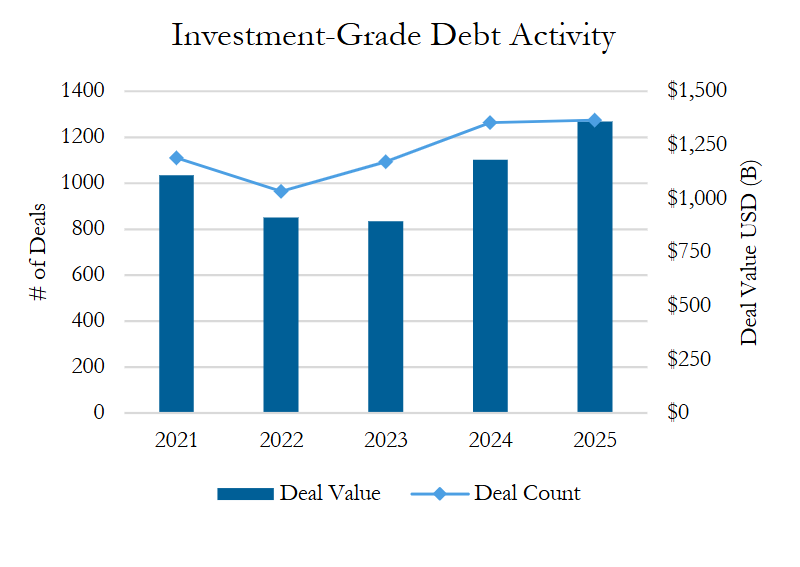

Investment-grade corporate bond activity1 continued to grow in 2025 with $1.36 trillion across 1,275 deals, largely surpassing the strong surge seen in 2024 from a deal value perspective (but only minimally in deal count). Deal value was up 15%, with deal count only up slightly (1%) from 2024. The continued growth in investment-grade corporate bond issuance indicates continued strong demand for high-quality debt.

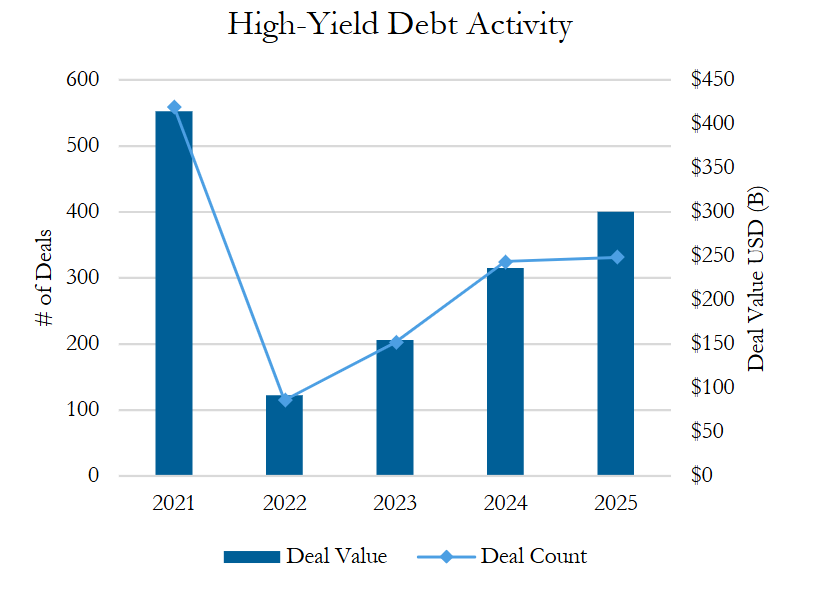

High-Yield Debt

Like with other debt and equity markets, 2025 continued the growing momentum of high-yield debt offerings since 2022, albeit at a more measured pace than prior years, with just over $300 billion priced across 331 offerings. Up 27% by deal value from 2024, 2025’s growth decelerated from the 50% increase from 2023 to 2024 and even more from the 70% jump of 2022 to 2023. With only six more deals (+2%) than in 2024, deal count growth was also minimal in 2025. Despite the progress, high-yield debt in 2025 remained below 2021’s record high by 28% by value and 41% by count, though still ranking third by deal value in the last decade.