This article was co-authored by Julian So from ONC Lawyers.

- Introduction – Defining Green Bonds

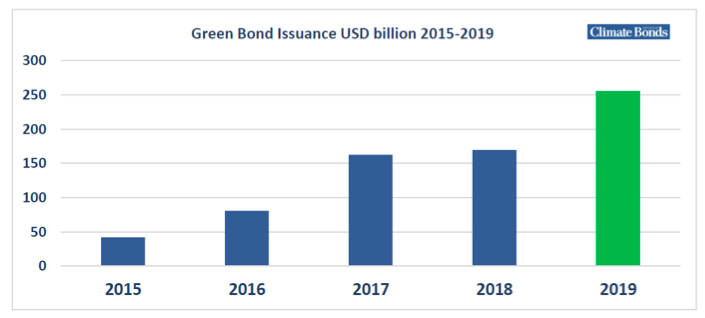

Green bonds, also known as climate bonds, are any type of bond instruments where proceeds are specifically earmarked for new and existing projects with environmental benefits and that can mitigate risks associated with climate change. The green bond market has undergone exponential growth in recent years, which can be seen in Figure 1 below showing the global issuance of green bonds from 2015 to 2019. With over 1,700 green bonds issued in 2019, valued at more than USD 257 billion, the green bond market is growing at a fast pace. It is estimated that by 2020, green bond issuance will surpass USD 350 billion

Figure 1: Global Annual Green Bond Issuance 2015 – 2019 (Source: Climate Bonds Initiative)

- Underlying Activities and Businesses of Green Bonds

The pivotal component of green bonds is an underlying environmentally beneficial activity, such as projects aimed at renewable energy, energy efficiency, pollution prevention and control, sustainable management of living natural resources, terrestrial and aquatic biodiversity conservation, clean transportation, sustainable water management, climate change adaptation, and eco-efficient products, production technologies and processes.

While broad categories of environmentally beneficial activities can be agreed at a high level in the market, criteria with respect to what activities qualify as environmentally beneficial is inevitably uncertain. This uncertainty prompts the question of who has the authority to decide what bonds can be labelled as green and this leads to two competing regimes: central regulation and market-driven regulation.

Some central regulators, such as China,[1] have regulations and rules to identify if an underlying activity or project qualifies as environmentally beneficial, which may not be aligned with the international green bond definitions. In most other jurisdictions, the sufficiency of environmental benefits is determined by the market, i.e. market-driven. That means, in market-driven regulated jurisdictions, the issuers are either able to label their bonds as green by voluntarily complying with universal guidelines, for example the Green Bond Principles published by International Capital Market Association, or by engaging an environmental consultant to issue an opinion for the benefit of investors in support of the green bonds.

- Real-World Examples of Green Bonds

Green bonds originated in 2008 when a group of Swedish pension funds wanted to invest in projects that help combat climate change and they turned to the World Bank for help. Thereafter the World Bank issued the first labeled green bond and started the trend of financing from investors for green projects. Since then, the World Bank has been at the forefront of expanding green bond product offerings with the view to financing a sustainable future. For example, in 2016 the World Bank issued a green bond to finance for air pollution control in China with a project life of 25 years and raised USD 523.6 million, of which the total financing is provided by World Bank loans. Another example is green bonds issued by the World Bank to finance a water resources and irrigation management program in Indonesia in 2011 with a project life of 25 years. The aggregate amount of these green bonds in Indonesia is USD 119.3 million, of which 74% is contributed by World Bank loans.

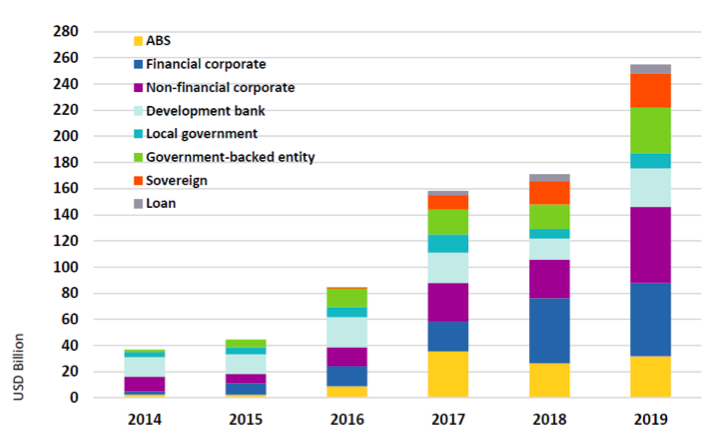

The green bond market had been dominated by issuers like the World Bank until 2013, when a growing number of green bond issuances were made by corporates, government-backed entities and governments, which is illustrated in Figure 2. In the meantime, it can also be seen in Figure 2 that a certain portion of green projects has been financed through the issuance of asset backed securities (“ABS”), which are backed by financial assets such as mortgages or lease receivables, i.e. securitisation.

Figure 2: Green Bond and Green Loan Issuance by Individual Sector 2014 – 2019 (Source: Climate Bonds Initiative)

One successful green ABS issue is a solar ABS issued by SolarCity (now known as Tesla Energy) in 2013. This ABS issue raised USD 54 million, backed by cash flows from power-purchase agreements for the electricity generated by a bundle of residential rooftop installations of around 5,000 customers.[1] Thereafter, Tesla Energy concluded 8 further solar ABS deals. Another successful real example of green ABS is related to a Dutch lender Obvion, which issued Europe’s first 100% green residential mortgage backed securities (meaning the bonds are backed by residential mortgages linked to energy efficient homes) in 2016 and raised USD 1.3 billion.

- Green Bond Investor Demand

Green bond issuance exploded in recent years as there is an increasing demand coming from a range of investors, which include the mainstream institutional investors such as Goldman Sachs, Amundi and AXA, corporate treasuries such as Barclays and Apple, specialist Environmental, Social, Governance (“ESG”) and responsible investors such as Natixis, sovereign and municipal governments such as California State Treasurer, and also retail investors who can invest through some mainstream investment banks or socially responsible funds.

Investing in green bonds can definitely bring quite a few benefits to investors in addition to the environmental benefits created for the whole society. For corporate investors, the most obvious benefit of investing in green bonds is to show that they are socially responsible. Accordingly, they can benefit from showing their efforts in integrating ESG factors into their investment processes so as to support initiatives their stakeholders or end asset owners care about. Besides, as the market is encouraging environmentally friendly projects, investing in green bonds also come with a monetary incentive from tax exemption and tax credits. Further, with the higher transparency of the use of proceeds, green bonds can be seen as less risky compared to conventional green bonds.

- Enhance Green Bonds through Securitisation and Derivatives

Even though the risk of green bonds might be lower than conventional bonds in the sense of more transparency, general green bonds still have the same credit risk as conventional bonds because their credit risk is based on the full balance sheet of the issuer. Therefore, as long as the green bonds are not independent from the original issuers, although the green project itself may have a low risk, the credit risk could still be high.

However, such issuer credit risk could be eliminated through green securitisation, which allows the issuance of bonds to be detached from the issuer’s balance sheet. This is because the underlying assets need to be assigned or transferred to an independent separate special purpose vehicle (“SPV”). In the green ABS issued by Tesla Energy mentioned above, the residential solar leases used to back the solar ABS had been transferred to a SPV for this purpose. Also, through multiple tranches of seniority, the more senior green ABS can potentially achieve a higher credit rating than the original asset owner and the less senior green ABS can deliver a higher return.

Furthermore, credit risks, currency exchange risks and other risks associated with receivables from “off-take” and purchase agreements can also be mitigated with derivatives. For example, the credit risk of the Indonesian government and the currency risk of the Indonesian Rupiah in a green project may be mitigated by entering into a credit default swap and a currency swap with one or more reputable banks providing such hedges.

Addressing climate change and environmental problems is a responsibility of the whole society. The increasing awareness of this responsibility can be reflected in the investors’ increasing interest in the social and environmental purposes of their investments. Green bonds’ popularity with both the issuers and investors definitely proves that this is the type of financial products that can satisfy both the issuers’ financing needs and investors’ investment needs and also the society’s overall need of combating climate change and environmental problems at the same time.