Are you an Australian entity receiving payments from the United States (US)? If yes, you may be asked by the payer to submit a W-8BEN-E form to assist with reducing or eliminating US withholding taxes. This page will discuss:

- what the W-8BEN-E form is;

- who needs to complete it;

- how to complete it.

What is the W-8BEN-E form?

The W-8BEN-E form (Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)) is used to inform the Internal Revenue Service (IRS) about the details of non-US entities receiving payments from United States sources.

Where can I access it?

The current version of the W-8BEN-E form can be accessed on the IRS website. Instructions to complete the form are also available as a PDF.

Who must complete it?

The form must be completed by non-US entities receiving payments from US sources. Entities include corporations and trusts, but not individuals. Non-US individuals should instead use form W-8BEN.

More details about the entities who should complete the W-8BEN-E form are found under the heading on the front page of the form.

Who is it sent to?

The W-8BEN-E form should be sent to the United States withholding agent or payer, not the IRS. For example, the W-8BEN-E form should be sent to a United States lender making interest payments to an Australian entity, rather than to the IRS itself.

Completing it

There are generally four to five sections of the W-8BEN-E form to complete.

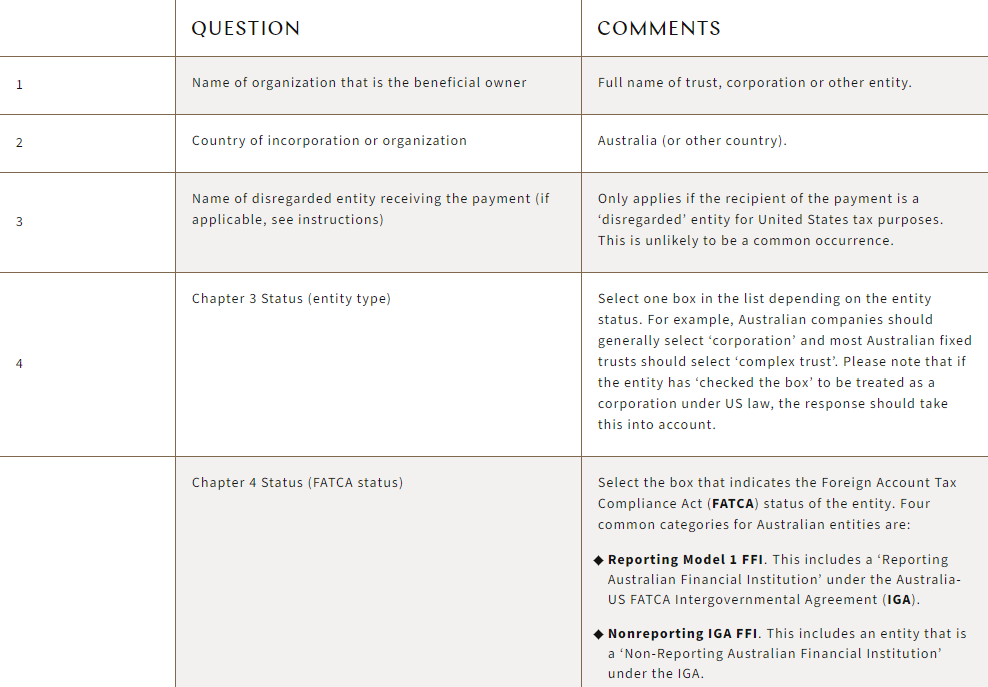

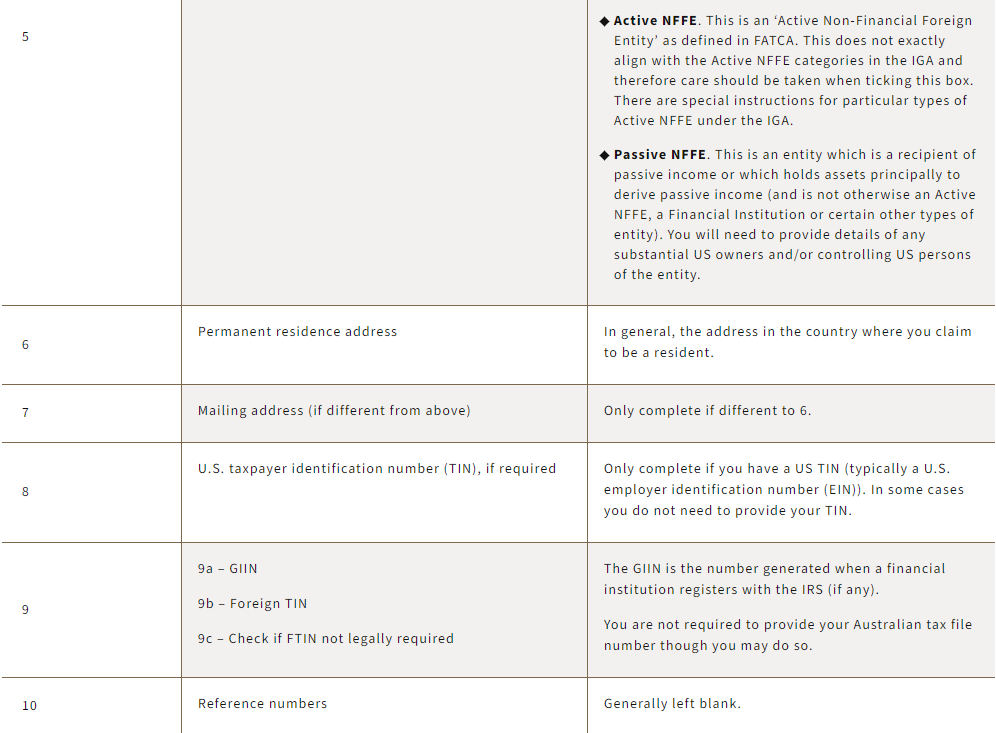

Completing Part I (Identification)

Part I contains 10 questions requesting general information about the entity. Questions 4 and 5 are the most important questions that will impact how the rest of the form is filled out.

Completing Parts II and III (Treaty benefits and disregarded entities / branches)

You should only complete Part II if a disregarded entity with a GIIN or a branch of an FFI in a country other than the FFI’s country of residence is involved. If so, you will need to fill in the FATCA status, address and GIIN (if any) of the disregarded entity in questions 11-13.

You can choose to complete Part III if you wish to claim tax treaty benefits in relation to certain payments. It is important to note that the Australia-US Double Tax Convention contains narrow and complicated limitation on benefits provisions. The eligibility for treaty relief should be carefully considered in the particular circumstances of each entity.

A flow-through trust is often treated as a ‘reverse hybrid’ and would not typically claim treaty benefits for the trust itself. The trust (being an intermediary) may complete Form W-8IMY and may be able to claim benefits on behalf of its members in Forms W-8BEN or W-8BEN-E. Different or additional documentation may also be required.

Completing Parts IV – XXIX (Based on the FATCA responses above)

You may be required to provide further information in relation to your FATCA status response in question 5. For example, if you selected “Nonreporting IGA FFI. Complete Part XII”, you will need to complete Part XII.

These additional FATCA sections are based heavily on US concepts, and less so from the IGA.

Completing Part XXX (Certification)

The appropriate signatory for the entity needs to declare that he/she has examined the information on this form and to the best of his/her knowledge and belief it is true, correct, and complete. Certain certifications are then made. The declarations and certifications are made under penalties of perjury.

There is also a promise to provide a new form within 30 days if any certification becomes incorrect (eg there is a change in the FATCA status or treaty eligibility).