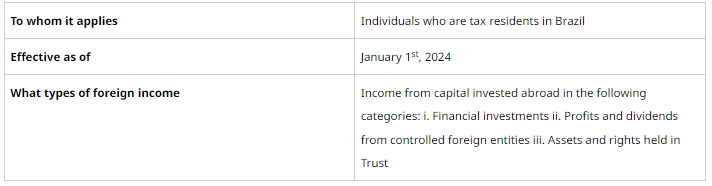

The Provisional Measure (MP) No. 1,171, published on April 30, 2023, brought new tax rules for individuals who are tax residents in Brazil earning foreign income, among other provisions.

General Rule

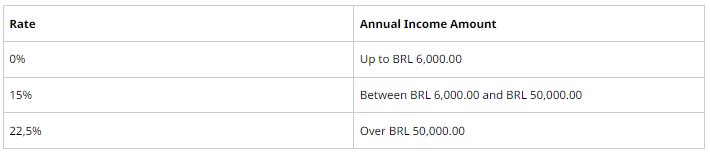

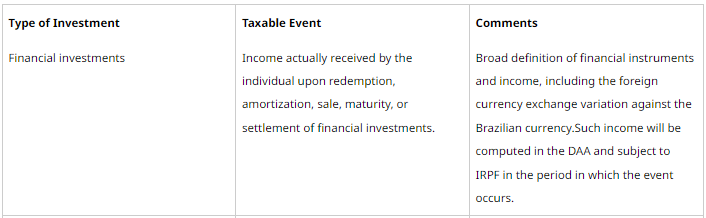

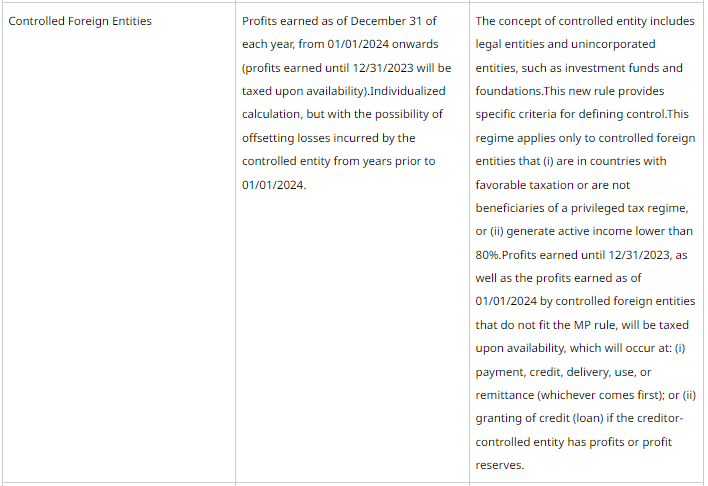

These foreign incomes will be subject to taxation under the Individual Income Tax (IRPF) and must be reported in the Annual Adjustment Return (DAA). Such incomes are subject to the progressive rates below, without any deductions:

Note: this form of taxation does not apply to operations subject to capital gain on the sale, discharge, or settlement of assets and rights located abroad that do not constitute financial investments under the MP.

Specific Rules:

Updating the Value of Assets and Rights Abroad

The Provisional Measure also allows individuals with assets and rights abroad to voluntarily update the value of their investments on 12/31/2022, with a more favorable taxation:

- Gain subject to a flat rate of 10%

- Tax must be paid by 11/30/2023

- The taxpayer may choose among the assets and rights that meet the requirements

- Gain will increase the acquisition cost, which may reduce future taxation when the asset or right is realized (as opposed to the progressive capital gain rates, ranging from 15% to 22.5%)

- It applies only to the following assets and rights, provided they are declared in the DAA for the 2022 fiscal year (filed by 05/31/2023):

- financial investments;

- real estate properties or assets that represent rights over real estate;

- vehicles, aircraft, vessels, and other movable assets subject to registration in general, even in fiduciary alienation, and

- stock participation in controlled entities.

- The following are excluded from the update: assets or rights that have not been declared in the DAA for the 2022 calendar year, filed by 05/31/2023; assets or rights that have been sold, discharged or liquidated prior to the option’s formalization date; jewelry, precious stones and metals, works of art, historical or archaeological antiquities, pets or sports animals, and animal reproduction genetic material, subject to registration in general, even in fiduciary alienation

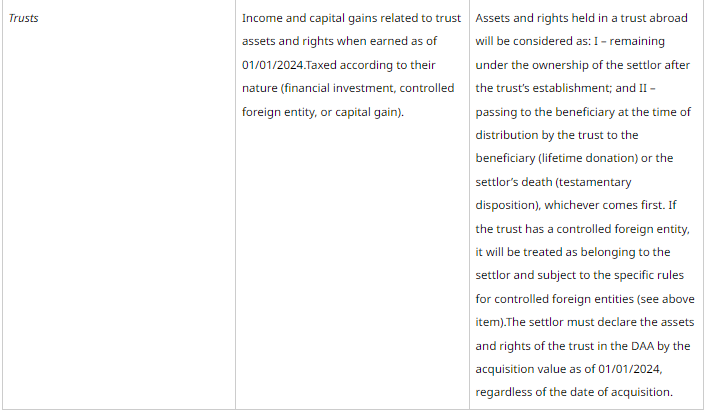

- Assets and rights subject to trusts also qualify.

- The individual who has opted for the reassessment of foreign controlled entities may carry out a new reassessment for the period up to 12/31/2023, with the gain also taxed at a rate of 10%, and the tax must be paid by 05/31/2024.

Conversion of Foreign Currency

The Provisional Measure determines that the exchange rate to be used to convert foreign currency values to Brazilian currency is the closing rate of the foreign currency disclosed for sale by the Central Bank of Brazil, for the occurrence date, thus allowing other currencies, besides the US Dollar (USD), to be used.

Repeals

The Provisional Measure repeals the following provisions of Section 24 of Provisional Measure No. 2,158-35/2001, which regulates the capital gain resulting from the sale of assets or rights and the liquidation or redemption of financial investments, owned by individuals, acquired in any currency other than the Brazilian Real:

- Paragraph 5 – which did not tax the capital gain resulting from the exchange rate variation due to the sale of assets or rights and the liquidation or redemption of financial investments made with income originally earned in foreign currency; and,

- Item I of paragraph 6 – which exempted from taxation of capital gain the disposition of assets abroad, including financial investments, when acquired as non-tax resident in Brazil

Key Take Aways

- Taxation of gains at 10% may be worthwhile, especially if the difference between the acquisition cost and the market value is significant and there is a possibility of realizing it in a short period of time.

- Holders of trusts without the purpose of estate succession (i.e., revocable trusts) should evaluate their usefulness in light of the new rules.

- The new rules make it difficult to defer taxation on foreign income, but it is worth considering certain types of financial investments abroad that can achieve this objective (deferral), since the legislation defines the moment of taxation as being the actual perception by the individual.

- Congress must convert the MP into law within the Constitutional deadline, and in this process, new changes may arise.