The “Tax Cuts and Jobs Act” signed December 22, 2017 (the “Tax Act”) changes US tax considerations for cross-border services outsourcing and cloud agreements. Whether you are a customer or a provider of services, you should evaluate your existing and planned outsourcing and cloud services arrangements to determine whether you may take advantage of these changes. The effect of the Tax Act is complex and will vary from deal to deal and company to company, and you should consult with your tax specialists. This Legal Update provides a high-level summary of those changes that we believe will most directly impact the economics and the structure of the outsourcing and cloud services arrangements.

1. Deduction of Cost of Equipment and Software

The Tax Act permits a company to deduct in the year of purchase the cost of “qualified property” that is either new property placed in service or used property acquired from an unrelated person. Under prior law, the purchase-year depreciation percentage was scheduled to be 40% for property placed in service or acquired in 2018, 30% in 2019 and 0% after that. The new law increases the percentage to 100% for property placed in service or acquired before 2023 and then ratchets it down to 80% for 2023, 60% for 2024, 40% for 2025 and 20% for 2026. Qualified property includes tangible property (such as computer and networking equipment) with a recovery period of 20 years or less and computer software that is acquired outside of the acquisition of a trade or business. Deductible fees paid for licensed software are not affected.

This deduction could benefit US customers purchasing equipment or software from either the manufacturer or the service provider. It also could benefit service providers who acquire equipment and software for use in their business. As a result, it may drive changes in co-location deals, hosting deals, outsourced managed services deals and even cloud arrangements.

This deduction benefits the company that pays the invoice and places the equipment and software in service. If a US customer is using local-to-local contracts for its non-US affiliates, it would not be able to claim this deduction for equipment and software purchased directly by its non-US affiliates.

2. New Paradigm for Service Providers Comparing Costs of Operating in United States versus Operating Abroad

In addition to allowing companies to deduct the cost of certain equipment and software, the Tax Act reduces the cost of producing services in the United States by reducing the corporate tax rate from 35% to 21%. This reduced tax rate may spur US companies to repatriate outsourced services from non-US providers back to company locations within the United States or even spur non-US providers to increase their operations in the United States. It may also cause customers to purchase more services from US providers (presumably at lower cost due to tax savings for the US providers).

Tugging in the other direction is the Tax Act’s transition from a system of worldwide taxation to a “modified” territorial system for US corporations that generate foreign-source net income through non-US subsidiaries. Under the Tax Act, foreign-source net income generated through non-US subsidiaries is not taxed in the United States except to the extent such income is considered either “Subpart F” income or global intangible low-taxed income (“GILTI”).

For the US-parented provider deciding whether to increase its US operations relative to non-US operations, there are several other provisions that must be considered, including the deduction for foreign-derived intangible income (“FDII”), the tax on GILTI, and the base erosion and antiabuse tax (“BEAT”). A non-US-parented provider deciding whether to increase its operations in the US group relative to the non-US group must consider how the FDII deduction and the BEAT affect the costs of operating in the United States.

3. FDII versus GILTI

The FDII deduction and the GILTI tax are considered the “carrot and stick” approach for incentivizing US-based companies to increase their US operations relative to non-US operations. The FDII deduction rewards US corporations that export services or sales of property to non-US customers by providing, in lieu of the 21% corporate rate, an effective rate of 13.125% on the non-routine portion of income from such activities. The GILTI tax, on the other hand, penalizes US corporations that earn income from such activities through offshore subsidiaries and that otherwise avoid US tax. The GILTI tax does this by imposing a minimum US tax at an effective rate of 10.5% on the non-routine portion of such income and permitting a foreign tax credit for only 80% of the foreign taxes paid to the nonUS jurisdiction.

Both FDII and GILTI generally focus on the same type of income, that is, income from the performance of services or sales of property to non-US customers. While the term “FDII” implies that the favorable tax rate is available only to income earned from “intangibles,” the plain language of the statute suggests that the scope is quite broad and the new provision should apply to any type of services income or sales income without regard to how much income is actually generated by intangible property. Similarly, GILTI has “intangible low-tax income” in its name, but the minimum tax actually targets lowtax services or sales income regardless of how much is generated from intangible property.

There are several variables that affect the amount of tax, including the company’s aggregate tax basis in tangible, depreciable assets and tax rate in each jurisdiction. The following example illustrates the interaction between FDII and GILTI and how that interaction relates to the costs of operating onshore or offshore.

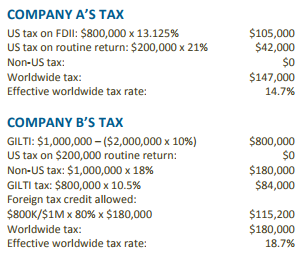

Assume there are two US-based service providers who perform services for a non-US customer. Company A performs the services from the United States, and Company B performs the services through its non-US subsidiary in Country X. Company A and Company B each earns $1 million of taxable income. Assume that Company B’s non-US subsidiary receives no intellectual property or services from its US corporate parent that would cause an income allocation to the parent under section 482 of the US Tax Code. Company A has $2 million of tax basis in tangible, depreciable assets in the United States, and Company B has $2 million of tax basis in tangible, depreciable assets in Country X. The tax rate in Country X is 18%.

The calculations below indicate that Company A will pay less tax than Company B:

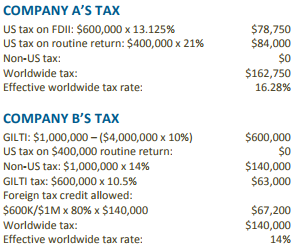

If, however, we change the two key variables, Company A pays more tax than Company B. For example, assume the same facts except that the tangible asset base is $4 million and the non-US tax rate is 14%. In that case, Company B would pay less worldwide tax than Company A.

One takeaway of the foregoing example is that the FDII deduction creates a disincentive to hold high-basis tangible assets in the United States. More high-basis tangible assets cause more of Company A’s income to be taxed at 21% rather than the more favorable rate for FDII. Note that purchased assets have a cost basis with straightline depreciation for FDII purposes even if they are currently expensed and have no tax basis for other purposes. Conversely, Company B has an incentive to build up its tangible asset base in the foreign jurisdiction. More high-basis tangible assets increase the amount of Company B’s routine return that is exempt from US tax and correspondingly reduce its GILTI tax. These drivers run counter to the incentive under the current expensing rule to invest in US tangible assets.

4. New Limits on Ability to Move Operations Offshore

The US-parented provider’s ability to shift income to the non-US subsidiary is still subject to the requirement in section 482 that the division of income between the US corporation and the non-US subsidiary be determined on an “arm’s length” basis. The Tax Act did not change those rules. Indeed, given that the income of a non-US subsidiary may not be taxed, the Internal Revenue Service (“IRS”) may enforce the section 482 principles with even more vigor than before.

The Tax Act made two changes that could make it substantially more costly for a US-parented provider to shift its intellectual property and contractual relationships with non-US customers to a non-US subsidiary. First, the Tax Act repealed the exception in section 367(a) that permitted US persons to make tax-free transfers of certain property to a non-US subsidiary for use in the active conduct of a trade or business. Second, the Tax Act defined “intangible asset” for purposes of both section 367(d) and section 482 to include goodwill, going concern value, workforce in place, or any other asset that is not attributable to tangible property or the services of any individual. Thus, if a US-parented provider permitted its non-US subsidiary to contract directly with a non-US customer that previously had contracted with the US-parented provider, the IRS may contend that the US-parented provider made a taxable outbound transfer of the value of the customer relationship.

5. Managing the BEAT

The BEAT affects US corporations with average annual gross receipts of at least $500 million for the last three years. The purpose of the BEAT is to protect the US tax base, particularly in light of the switch to the modified territorial system. The BEAT is a minimum tax (5% for a taxable year beginning in 2018, 10% for taxable years beginning after December 31, 2018 and before January 1, 2026, and 12.5% in a taxable year beginning after 2025) that effectively compares the corporation’s regular tax liability to the minimum tax on the corporation’s income calculated without taking deductible payments to non-US affiliates into account. If the minimum tax amount is larger, then the BEAT is owed in lieu of regular tax.

The BEAT becomes important in the outsourcing context where a US-based service provider makes a deductible payment to a non-US affiliate for services or property. For example, assume a US corporation contracts to provide outsourcing services to a non-US customer, and the corporation performs the services using personnel in India employed by a non-US subsidiary. Under section 482 principles, the US corporation would be required to make an arm’s length payment to the non-US subsidiary for the value of providing those services to the corporation’s customer. That payment would be added back to the corporation’s taxable income and trigger the BEAT unless it qualifies under an exception in the Tax Act for payments that are “arm’s length” as determined by using the section 482 services cost method (“SCM”).

The SCM permits intercompany charges at cost with no markup if they are specifically listed by the IRS (e.g., payroll, treasury activities, information and technology) or are otherwise low-margin services with an arm’s length charge of 7% or less. Use of the SCM, however, may not always be practical because foreign jurisdictions typically require a payment that includes a markup on cost. In India, for example, a markup on cost is predominantly applied.

It was recognized during the legislative process that the utility of the SCM exception would be limited unless a clarification was made. There is a Senate floor colloquy indicating that if taxpayers may set up two accounts, one for “services cost with no markup and another account for any additional amounts paid or accrued, . . . the first account would be subject to the exception under the bill.” It is not known whether Treasury will issue guidance that confirms the ability of US corporations to bifurcate their payments to nonUS affiliates in order to qualify for the SCM exception. A US corporation taking this position should add back only the markup component of the charge for BEAT purposes.

Another concern for a US-parented provider that operates through non-US subsidiaries is that payments made to a non-US subsidiary are likely Subpart F income unless the services are performed in the country in which the subsidiary is incorporated. For example, income earned by a UK subsidiary performing services through its employees in India would be Subpart F income because the subsidiary is performing services outside of its country of incorporation. In that case, the benefit that the US-parented provider derives from deducting a charge paid to the UK subsidiary would effectively be eliminated due to the inclusion of the UK subsidiary’s income in the US corporation’s income. The add-back of the deduction for BEAT purposes is required even if the payment is Subpart F income and the US corporation effectively does not enjoy a net deduction. Using the bifurcation approach discussed above to qualify for the SCM exception could mitigate that problem.

There are many other changes and considerations for US companies under the Tax Act. Whether considering a new outsourcing or cloud deal, or operating under previous arrangements, companies should re-evaluate the structure of these deals to capture valuable tax benefits and to avoid potential tax pitfalls.