As the world races to address the twin epidemics of obesity and type 2 diabetes, GLP-1 receptor agonists have emerged as the most transformative drug class of the decade. Semaglutide and tirzepatide now generate billions in annual revenue, reshaping pharma valuations and health system budgets alike. The CDC’s National Health and Nutrition Examination Survey data shows 40.3% adult obesity prevalence in the US, anchoring the scale of the public health burden being referenced. But beneath the commercial success, a different kind of race is unfolding one that is being fought in patent offices and courtrooms across the globe. The question is when and by whom the generic alternatives will arrive.

To understand this transition, it is essential to look at the IP architecture behind GLP-1 drugs. Just like many other drugs, GLP-1 drugs also carry layered protection such as compound patents, formulation patents, delivery device patents, and method-of-use claims, each expiring independently and on different timelines across jurisdictions.

Using PatSeer’s patent search software, we conducted a thorough patent search across GLP-1 patent families, queried across GLP-1 receptor agonist synonyms. The results of this patent analysis show a multi-layered IP strategy designed to sustain exclusivity well beyond the dates most commentators cite.

Key Insights from the GLP-1 Patent Landscape

GLP-1 patent filings surged 62% between 2019 and 2022

- The United States dominates priority filings with 760 families

- Obesity-related GLP-1 patents are newer and extend exclusivity

- Multiple overlapping patents create a dense patent thicket

- Generic entry will likely occur in markets by 2026

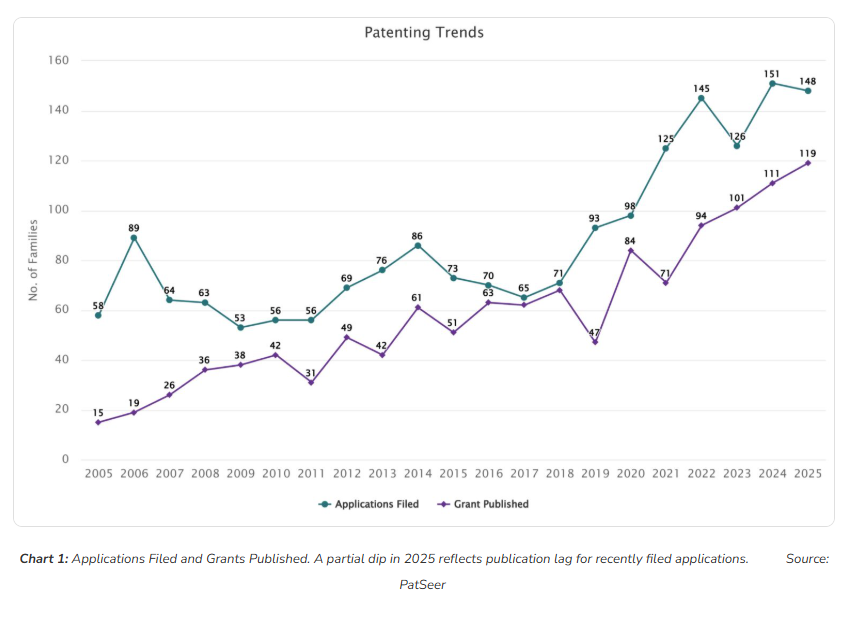

What Do GLP-1 Patent Filing Trends Reveal?

Chart 1 shows a clear and sustained acceleration in GLP-1 patent activity over two decades. From 2005 to 2018, filing volumes were relatively stable, ranging between 58 and 89 application families annually. This period reflects foundational research around peptide chemistry and initial formulation work.

The real turning point arrives between 2019 and 2022. Applications climbed from 93 families in 2019 to a peak of 145 in 2022, a 62% surge that tracks directly with the commercial success of semaglutide and the subsequent obesity indication expansion. Grant publications followed the same trajectory, reaching 119 the highest recorded level in 2025.

This convergence of high filing volumes and rising grant rates carries an important signal for market observers. The GLP-1 patent thicket is being actively reinforced, with a substantial volume of recently filed applications still maturing through examinations representing tomorrow’s exclusivity barriers.

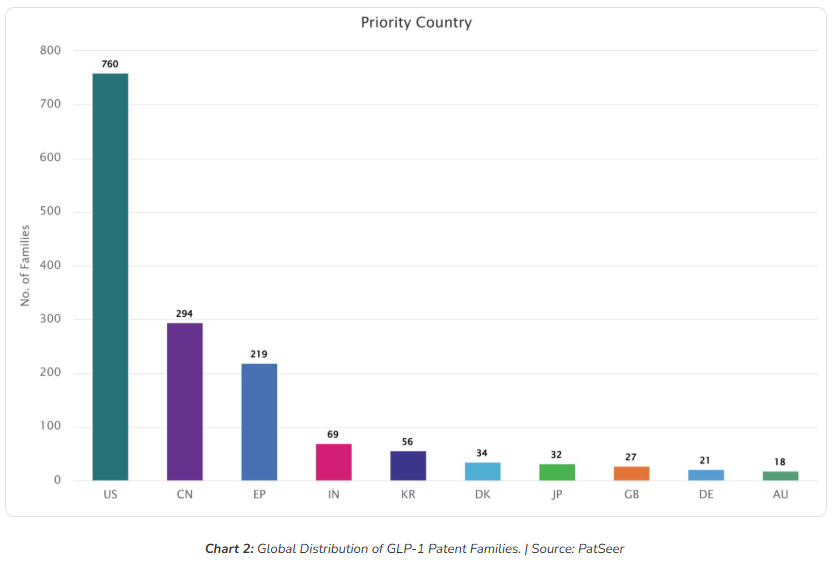

Which Countries Lead GLP-1 Patent Filings?

Chart 2 shows that the United States leads with 760 priority filings confirming its position as the primary arena for GLP-1 IP competition. This concentration reflects both the size of the American pharmaceutical market and the strategic importance of USPTO examination quality for downstream litigation.

China follows with 294 families, a figure that demands serious attention. Chinese assignees are not simply licensing from Western innovators they are positioning for both domestic market protection and potential global generic or biosimilar plays. India’s 69 families, while smaller in absolute terms, carry disproportionate strategic weight given the country’s Section 3(d) patent standards and its role as the world’s largest manufacturer of generic pharmaceuticals.

European Patent Office filings stand at 219 families, with South Korea (56), Denmark (34), Japan (32), and the United Kingdom (27) completing a truly global footprint. The geographic spread also reveals meaningful white space: jurisdictions with thin branded-player coverage, but strong generic manufacturing capacity represents the earliest corridors for generic market entry.

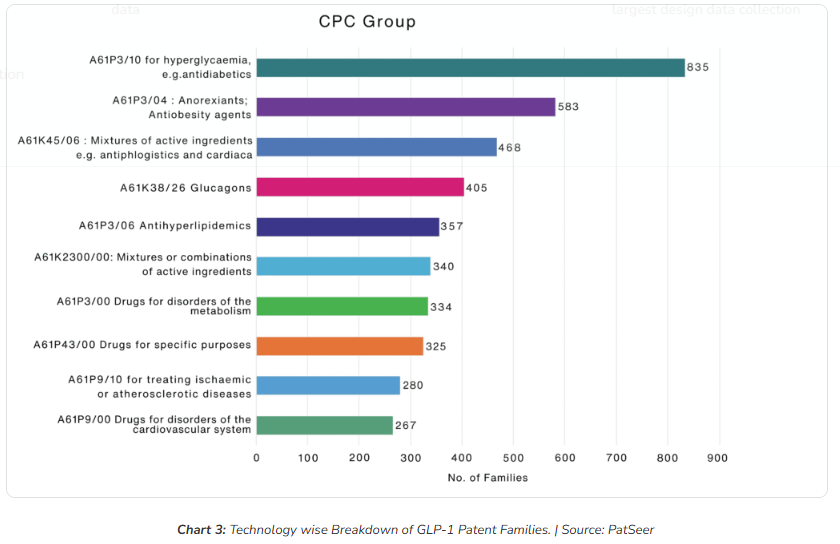

What are the Key Technology Areas in GLP-1 Patents?

Early GLP-1 patent activity was almost entirely concentrated in antidiabetic applications. Chart 3 shows that A61P3/10 (hyperglycaemia / antidiabetics) remains the dominant classification by a wide margin. This is the foundational layer of GLP-1 protection that most expiry discussions reference.

Early GLP-1 patent activity was almost entirely concentrated in antidiabetic applications. Chart 3 shows that A61P3/10 (hyperglycaemia / antidiabetics) remains the dominant classification by a wide margin. This is the foundational layer of GLP-1 protection that most expiry discussions reference.

But the second-largest cluster tells a more forward-looking story. A61P3/04 (antiobesity / anorexiant agents) has accumulated 584 patent families. These are, on average, newer filings than the diabetes corpus, meaning their protection timelines extend further into the future. A generic manufacturer who successfully clears the diabetes IP may face an entirely separate and more recent thicket when seeking the obesity indication.

The data also highlights significant IP density in combination therapy (A61K45/06, 468 families), glucagon-related innovations (A61K38/26, 405 families), and antihyperlipidemic applications (A61P3/06, 357 families). The cardiovascular clusters A61P9/10 (280 families) and A61P9/00 (267 families) are particularly notable: these represent the newest and fastest-growing areas of GLP-1 IP, where both Novo Nordisk and Eli Lilly are actively building post-cliff moats around recently approved cardiovascular indications.

The overall picture is a technology landscape that has expanded well beyond its diabetic origins. Each new indication represents a new market with an independent exclusivity layer with its own filing dates and expiry timeline.

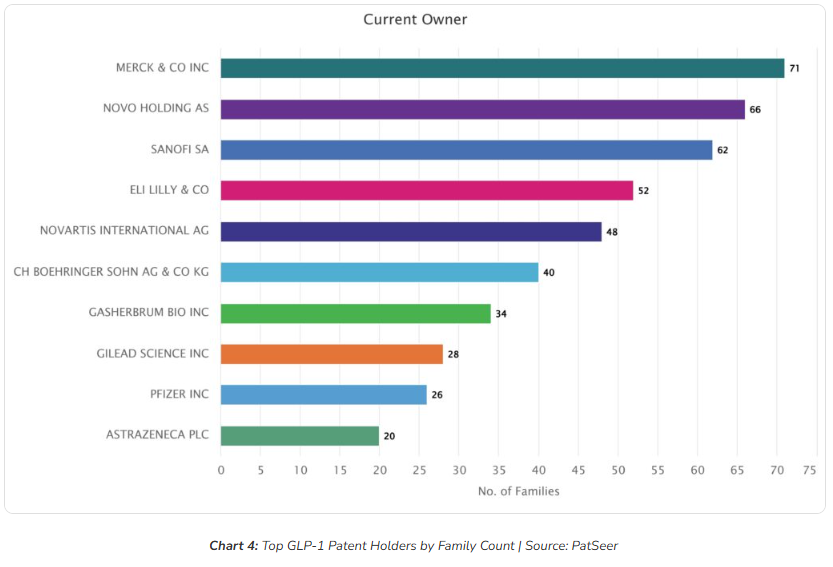

Who are the Key Players in the GLP-1 Patent Landscape?

The GLP-1 patent landscape is far more competitive and distributed than the commonly assumed Novo Nordisk versus Eli Lilly narrative.

While Novo Nordisk and Eli Lilly remain central from a commercial standpoint, the IP landscape shows a broader set of influential players. Merck & Co. emerges as a leading portfolio holder, highlighting how patent strength and market visibility do not always align.

Other major pharmaceutical companies, including Sanofi and Novartis, have established significant positions, reinforcing the depth of competition across the space. Boehringer Ingelheim also maintains a strong presence, contributing to the expanding IP footprint around GLP-1 therapies.

Beyond the large pharma players, emerging and specialized biotech firms such as Gasherbrum Bio add another layer of competitive complexity. At the same time, companies like Gilead Sciences, Pfizer, and AstraZeneca indicate continued strategic interest from across the broader pharmaceutical ecosystem.

The broader takeaway is that GLP-1 represents a crowded and multi-stakeholder IP landscape, where innovation and opportunity are distributed across a wide range of organizations. For companies evaluating licensing or partnership strategies, this diversity significantly increases both freedom-to-operate complexity and the potential for strategic collaboration or acquisition.

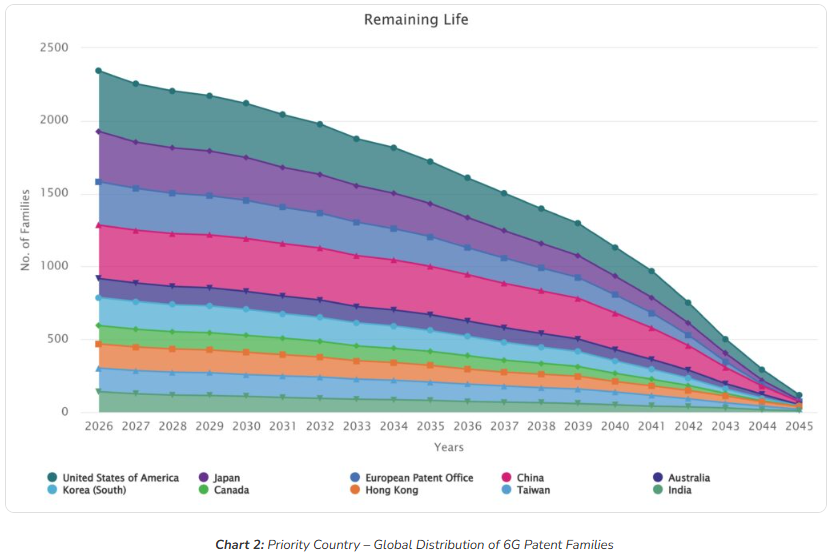

When Will GLP-1 Patents Expire?

The GLP-1 patent wall does not come down at once. Protection erodes gradually, jurisdiction by jurisdiction, across a window stretching from today through the mid-2040s.

The GLP-1 patent wall does not come down at once. Protection erodes gradually, jurisdiction by jurisdiction, across a window stretching from today through the mid-2040s.

The United States carries the highest volume of active families at any point through 2045, confirming it as the last major market where branded protection will hold. The European Patent Office and Japan follow a similar long-tail trajectory. China and Korea show steeper early declines, consistent with their higher concentration of older filings and the generic manufacturer positioning already visible in the priority country data.

India’s trajectory is particularly worth watching. The country’s well-established framework for challenging pharmaceutical patents under Section 3(d), combined with a growing domestic generics industry, positions it as one of the earliest major markets where generic GLP-1 entry becomes viable.

For companies assessing market entry timing, this chart is the most actionable signal in the dataset. The question is which jurisdiction opens first, and whether manufacturing and regulatory readiness can match that window.

What the GLP-1 Patent Landscape Signal?

The GLP-1 patent landscape highlights several strategic realities for pharmaceutical companies and generic manufacturers. GLP-1 patent activity continues to accelerate, reflecting sustained investment as the market expands beyond diabetes into obesity and cardiovascular therapies. The competitive field is broader than often assumed. While Novo Nordisk and Eli Lilly remain central players, several pharmaceutical and biotech companies hold meaningful GLP-1 portfolios.

Patent protection will also erode gradually rather than through a single patent cliff. Tracking this erosion across jurisdictions requires more than manual monitoring making AI patent search capabilities a critical tool for generic manufacturers and innovators alike. Generic entry is likely to occur in stages across jurisdictions, with emerging markets potentially opening earlier than the United States and Europe. For companies planning market entry, licensing strategies, or biosimilar development, understanding this layered patent landscape will be critical and leveraging purpose-built patent analysis software is increasingly essential to navigating it effectively.