In brief

On 12 September 2023, the EU Commission published a number of important transfer pricing initiatives both as part of the BEFIT Directive proposals and in the form of a standalone Transfer Pricing Directive.

These Directives, if adopted, should move the needle toward both the standardization of transfer pricing rules within EU member states, thereby reducing intra-EU transfer pricing disputes, and the simplification of compliance burdens. On the whole, these measures should be seen as a positive development for businesses.

It is clear that transfer pricing continues to be a key area of focus for many tax authorities. With proposed changes being consulted on in a number of jurisdictions (including the UK), alongside the ongoing work of the Organisation for Economic Co-operation and Development (OECD) in relation to Pillar 1 Amount B, there will be a significant amount of change in this area for in-house tax teams to consider.

Stakeholders have been asked to provide feedback on the new proposal by 15 November 2023

Background

On 12 September 2023, the EU Commission published a number of important transfer pricing initiatives with the goal of reducing tax compliance costs for cross-border businesses in the EU, increasing tax certainty, and mitigating the risk of tax disputes, double taxation or double non-taxation.

These initiatives form part of the package of proposals for the BEFIT Directive, a proposal that introduces a common set of rules for EU-based groups of companies to determine their taxable base, as well as instruments to facilitate transfer pricing compliance. BEFIT is the acronym for Business in Europe: Framework for Income Taxation, and you can find our alert on the BEFIT proposal here. The initiatives also form part of the proposed Transfer Pricing Directive, aimed at harmonizing transfer pricing rules within the EU and ensuring a common approach.

The EU Commission has opened the consultation process on the BEFIT Directive draft proposal and invited stakeholders to provide feedback by 15 November 2023. This is a great opportunity for multinational enterprises to provide input on the technical provisions of the proposal as well as on any administrative and compliance burdens.

The new transfer pricing initiatives come following the EU Commission's recognition of the high transfer pricing compliance costs borne by businesses, the increasing number of tax disputes and instances of double taxation, and the significant time and resources being deployed by member states to resolve cross-border issues.

While EU member states are part of the OECD and should follow OECD principles and recommendations, the role of the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations ("OECD Transfer Pricing Guidelines") differs between member states. Transfer pricing rules are currently not fully aligned in all member states, and each member state applies varying degrees of discretion in interpreting and applying the OECD Transfer Pricing Guidelines. These factors contribute to complexity for both multinational businesses in seeking to apply transfer pricing rules and guidelines consistently to their cross-border activities, and member state tax authorities in asserting taxing rights. This could create significant obstacles for the operation and competitiveness of the EU single market.

What is being proposed?

The BEFIT Directive and the Transfer Pricing Directive have different main focus areas and target different transfer pricing issues.

i. The BEFIT Directive's main focus is to establish a common set of rules for multinational groups headquartered in the EU or headquartered in third countries but with sufficient EU nexus to determine their common taxable base. The BEFIT Directive also proposes rules on simplifying transfer pricing compliance, in particular for low-risk activities (limited risk distributors and contract manufacturers). In this context, the BEFIT Directive seeks to achieve something similar to the approach offered by the OECD Pillar 1 Amount B proposal in terms of simplifying the application of the arm's length principle for certain activities.

ii. The Transfer Pricing Directive, in turn, focuses on harmonizing transfer pricing rules within the EU. The Transfer Pricing Directive is broad in scope, provides substantive transfer pricing rules and explicitly endorses the OECD Transfer Pricing Guidelines. This legislative initiative is new at an EU level, as transfer pricing rules are not harmonized at an EU level through legislative acts. In the past, the EU Commission dealt with transfer pricing issues through the long-standing work of the Joint Transfer Pricing Forum, an expert group set up by the EU Commission in 2002 and whose work was to propose to the EU Commission pragmatic, non-legislative solutions to practical problems posed by transfer pricing practices in the EU. What has been proposed under the Transfer Pricing Directive is consistent with the Joint Transfer Pricing Forum's past output.

The BEFIT Directive and transfer pricing

The BEFIT Directive offers two important simplifications for transfer pricing compliance and risk assessment in relation to certain types of transactions.

• For intra-BEFIT group transactions (for the purposes of calculating a BEFIT group member's baseline allocation)

• For low-risk activities between a BEFIT group member and an associated enterprise outside the BEFIT group

A "BEFIT group" is a group of EU-resident companies and permanent establishments that are owned at least 75% by a common parent entity.

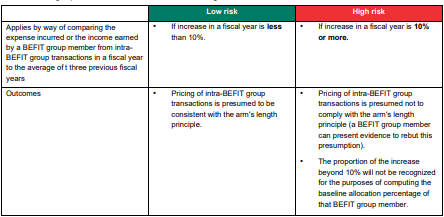

For intra-BEFIT group transactions, member states should categorize risk assessment into two "zones".

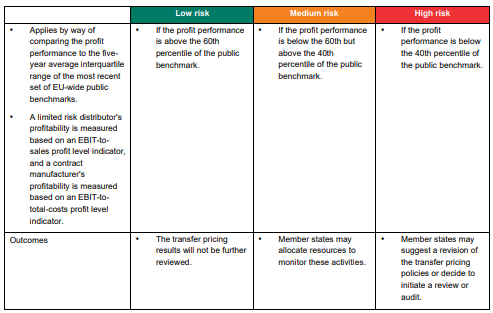

Another proposal of the BEFIT Directive is to introduce a simplified approach for transfer pricing compliance for low-risk activities between a BEFIT group member and an associated enterprise outside the BEFIT group. This will apply to low-risk distributors and low-risk contract manufacturers resident or situated in the form of a permanent establishment in a member state.

Under the proposal, member states shall structure their risk assessment in three transfer pricing risk zones, a so-called traffic light system. This approach is very similar to that taken by the Australian Taxation Office under its transfer pricing guidelines issued in 2019.

The EU Commission will be responsible for establishing the search criteria to identify comparables and establishing appropriate benchmarking analyses. Benchmarking analyses will be published on the EU Commission's website and updated every three years.

The Transfer Pricing Directive

The Transfer Pricing Directive generally sources many of its provisions from the OECD Transfer Pricing Guidelines, with some deviations and additions. Its main aim is to establish a more consistent application of transfer pricing rules across EU member states.

The Transfer Pricing Directive explicitly endorses the OECD Transfer Pricing Guidelines and therefore prescribes that member states must transpose the transfer pricing rules provided in the Directive in a manner that ensures that they are applied consistently with the OECD Transfer Pricing Guidelines.

The Council, based on a proposal of the EU Commission, may lay down further rules (consistent with the OECD Transfer Pricing Guidelines) on how the arm's length principle and the other provisions in the Transfer Pricing Directive should be applied to specific transactions between associated enterprises (e.g., the transfer of intangible assets or rights in intangible assets, the provision of services, cost contribution arrangements, transactions in the context of business restructurings, financial transactions) and dealings between a head office and its permanent establishments.

In a nutshell, the Transfer Pricing Directive sets out the following:

• A common definition of associated enterprises for EU member states, generally using a 25% threshold of voting rights and/or capital participation and/or profit entitlement as well as applying a "significant influence" test.

• More effective mechanisms for corresponding adjustments to be made outside a mutual agreement procedure, in particular the following:

(1) A "fast-track" procedure within 180 days at a taxpayer's request:

• Such a request is to be made by a taxpayer indicating all factual and legal circumstances necessary to evaluate the primary adjustment and providing a certificate or equivalent document attesting the definitive nature of the primary adjustment abroad. If this adjustment is not yet definite, a certificate is to be provided at a later stage before the corresponding adjustment is granted.

• Member states must declare the request admissible within 30 days if all the information has been provided or notify the taxpayer of the lack of necessary information and grant a cure period of at least 30 days.

• Member states must then ensure that, when the double taxation arises from a primary adjustment, the procedure is concluded within 180 days from the receipt of the taxpayer's request with a reasoned act of acceptance or rejection.

(2) Joint audits or other forms of international co-operation:

• Conditions for downward adjustments that could potentially be performed by member states.

• Conditions for recognizing compensating adjustments carried out by multinational groups.

• A requirement for the delineation of the actual transaction between the associated enterprises based on contractual relations between the parties and the parties' actual conduct.

• Transfer pricing methods in line with the OECD Transfer Pricing Guidelines and conditions when other valuation methods or techniques may be applied.

• Factors for comparability analyses in line with the OECD Transfer Pricing Guidelines.

• Rules for determining the arm's length range using the interquartile (the 25th to the 75th percentile) range of the results derived from a set of uncontrolled comparables and rules for adjustments to be made if the results are outside of the interquartile range. Notably, the proposal requires a mandatory adjustment to the median of all the results unless it is proven that any other point of the range determines an arm's length price. These proposed adjustment rules are generally stricter than those prescribed in the OECD Transfer Pricing Guidelines, which do the following:

(1) Provide recommendations on using interquartile results as one of the options for narrowing down the range and increasing comparability if the comparables have defects.

(2) State that where the range comprises results of relatively equal and high reliability, it could be argued that any point in the range satisfies the arm's length principle.

(3) Mention that it may be appropriate to use measures of central tendency (for instance, the median, the mean or weighted averages, etc., depending on the specific characteristics of the data set) where comparability defects remain.

The mandatory adjustment to the median also deviates from the current practice and legal framework in some member states.

An initiative to lay down common templates for transfer pricing documentation and define those that would have to abide by these templates.

Possible implications and next steps

Generally, the move toward standardization of transfer pricing rules within EU member states should be seen as a positive development toward simplification, reduction of intra-EU transfer pricing disputes and compliance burdens.

If the BEFIT Directive is adopted with the currently proposed transfer pricing initiatives, businesses and tax authorities may have a mutual understanding of the risk assessment protocols for at least some of the business activities. Businesses would be able to cross-check their results against the predetermined parameters or publicly available benchmarks to assess the level of the risks and proactively take steps to mitigate them. Tax authorities, in turn, would be able to dedicate their resources to checking transactions that show abnormal results or are nonroutine.

Adoption of the Transfer Pricing Directive, as the proposal currently stands, may lead to more standardization of transfer pricing rules across the EU member states.

Taking into account that the Transfer Pricing Directive leverages many of its provisions on the already widely applied OECD Transfer Pricing Guidelines, businesses would likely not face a significant number of changes. That being said, certain proposals require a closer look (e.g., rules on calculating benchmark ranges and the potential adoption of common templates for transfer pricing documentation). The rules for corresponding and compensating adjustments could be of particular assistance to businesses.

One noteworthy area of potential complexity is the interaction between the BEFIT approach to risk assessments for low-risk transactions, in particular baseline distribution activities, and the ongoing work of the OECD/Inclusive Framework in relation to Amount B. While the consultation in relation to Amount B is ongoing, it is anticipated that the Amount B guidance will be published in the OECD Transfer Pricing Guidelines in January 2024. The BEFIT approach may need to be revisited once the OECD guidance on Amount B has been finalized.

If adopted, the Directive has to be transposed into local law by 31 December 2025, and the provisions will apply as of 1 January 2026.