The global aviation industry is witnessing a boost with total passenger traffic expected to reach approximately 9.5 billion in 2024, surpassing pre-pandemic levels and marking a 10% year-on-year growth from 2023.1 This global momentum is mirrored in India, where domestic passenger traffic has risen by 9.6% year-on-year, signaling a vibrant recovery and strong demand for air travel.2

As the global aviation landscape evolves, India’s aviation sector stands at a pivotal crossroads, rich with opportunities yet fraught with challenges. This article explores the significant changes, while also highlighting the broader opportunities that lie ahead for India’s aviation sector. As we delve into these opportunities, we will uncover how the current challenges, if tackled properly, could pave the way for a more robust and competitive aviation industry.

Recent key developments in Indian aviation sector

- Bhartiya Vayuyan Vidheyak Bill

The Ministry of Civil Aviation (“MoCA”) plays a crucial role in shaping the future of civil aviation in India, overseeing a vast array of regulatory frameworks and growth initiatives. The Ministry along with regulatory authorities such as Directorate General of Civil Aviation (“DGCA”), Aircraft Accidents Investigation Bureau (“AAIB”), Airports Authority of India (“AAI”), Airports Economic Regulatory Authority (“AERA”), and Bureau of Civil Aviation Security (“BCAS”) is tasked with not just enhancing air transport but also ensuring safety, efficiency, and sustainability. These authorities are governed by Aircraft Act, 1934.

The Aircraft Act, 1934 was enacted to regulate activities related to aircraft including their manufacturing, possession, use, operation, sale, import, and export. However, over the years, this Act has undergone numerous amendments leading to complexities and ambiguities. These changes often caused confusion and regulatory inconsistencies.

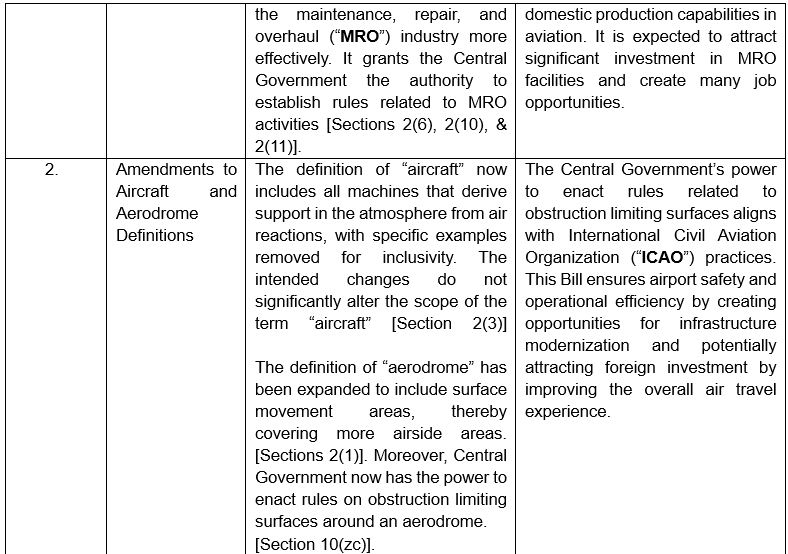

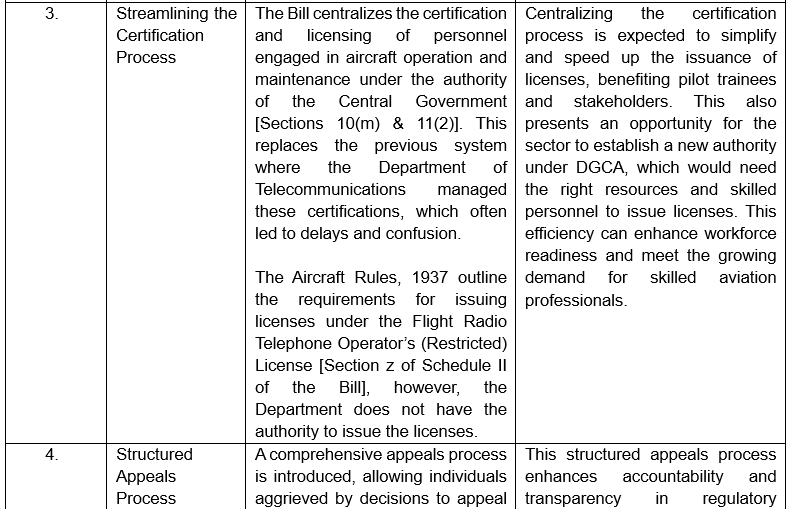

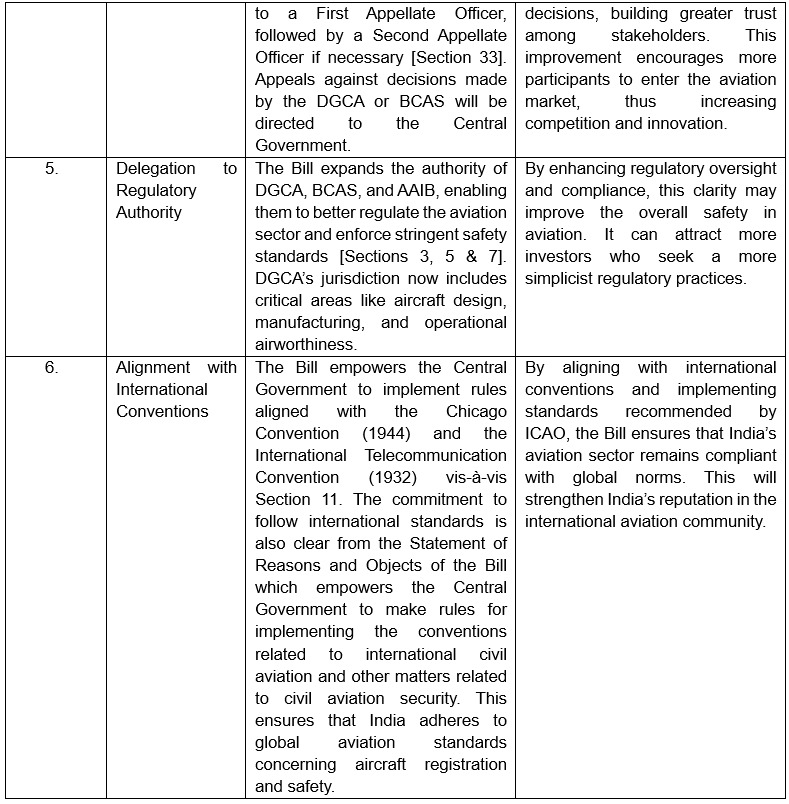

To address these challenges, the Bhartiya Vayuyan Vidheyak Bill 2024 has been introduced as a transformative measure. The Bill aims to streamline regulations and align them with international standards. By addressing redundancies and ambiguities, this Bill promises to create a more favorable environment for investment and growth. Important changes proposed in the Bhartiya Vayuyan Vidheyak Bill along with potential opportunities:

- Growth in flight training institute

To address the increasing demand for qualified professionals many leading aviation airlines are establishing their own training institutions. For example, Air India is investing INR 200 crore to set up South Asia’s largest flight training academy in Amravati, Maharashtra, aimed at training up to 800 pilots annually. With its massive order of 470 new Airbus and Boeing aircraft, the airline anticipates a growing need for skilled pilots.

Similarly, the GMR Group has launched the GMR School of Aviation by investing INR 50 crore to train aircraft engineers. As airlines like IndiGo, Air India, and Akasa Air place significant orders for new aircraft, these training initiatives are essential to ensure a steady flow of industry-ready talent, helping to address the shortage of skilled professionals in the sector.

- GIFT City as a key hub

Gujarat International Finance Tech-City (“GIFT City”) has rapidly emerged as a critical hub for aircraft leasing with approximately 26 leasing entities now registered at its International Financial Services Centre (“IFSC”)3 and more expected to follow. Since the Indian government’s push in 2019 to make India a global player in aviation leasing, GIFT IFSC has seen significant growth in leasing transactions. Over 150 aviation assets including aircraft, engines, and helicopters have already been leased through the center, demonstrating the growing demand for India-based leasing operations.

This shift represents a strategic move to reduce reliance on traditional leasing centers like Dublin and Singapore, positioning GIFT City as a competitive alternative. One of the most notable milestones in this development was Air India’s acquisition of an Airbus A350-900 through a finance lease transaction facilitated by Air India Fleet Services Limited which is a GIFT IFSC-registered entity. 4

GIFT IFSC with its favorable tax policies, regulatory framework, and infrastructure has attracted both domestic and international leasing companies. As more airlines expand their fleets and the demand for aircraft leasing increases GIFT City is poised to become a central player in the global aircraft leasing market.

Opportunities in India’s Aviation Sector

- Rising Air Travel Demand

The Indian aviation sector continues to show strong growth with domestic air passenger traffic for the month of October estimated at approximately 138.5 lakh. This represents a 6.3% increase from 130.3 lakh in September 2024 and a 9.6% year-on-year growth. Notably, passenger traffic in October 2024 was 12.8% higher than the pre-Covid levels of October 2019. For the first seven months of FY2025 (April-October 2024) domestic air passenger traffic reached 932 lakh, showing a year-on-year growth of 5.9% and a significant 12.6% higher than the pre-Covid level of 827.5 lakh in the same period of FY2020.5

In addition to strong domestic air traffic, international passenger traffic for Indian carriers also saw impressive growth. For the first half of FY2025, international passenger traffic stood at approximately 162.6 lakh, marking a year-on-year increase of 16.0% and a 46.5% rise compared to the pre-Covid levels of 111 lakh in the same period of FY2020, this will be strengthened by recent Bilateral Air Services Agreements with 116 countries which include key partners like Australia, the UK, and the UAE.6

- Opportunities for Carriers

India’s aviation sector is booming with rapid growth and heavy investments creating vast opportunities for carriers. This growth allows airlines to expand operations, add new routes, and invest in modern fuel-efficient aircraft. New airports, maintenance facilities, and the rise of Urban Air Mobility (“UAM”) in crowded cities are also driving innovation across the industry.

Foreign Direct Investment (“FDI”) is fueling further growth with partnerships like the Airbus-Tata collaboration and Air India’s restructuring under Tata Group opening up new avenues. As private investments continue to pour in there is also a growing demand for MRO services which will provide airlines with opportunities to upgrade fleets and boost efficiency.

This expansion is reflected in major fleet orders. Air India has placed an order for 85 Airbus planes while IndiGo is investing USD 5 billion in 30 A350-900s, bringing its total fleet order to over 1000 aircraft. SpiceJet has leased 10 new Boeing 737s after raising funds and together with Air India and IndiGo’s plans for 170 wide-body planes. India’s total aircraft order book has surpassed 1,200 planes in just 14 months (since February 2023). New entrants like Shankh Air, which recently received approval to operate, are further contributing to the sector’s dynamic growth.

- Opportunities in India’s MRO Sector

Currently, over 80% of India’s MRO needs are met by foreign sources. A Deloitte report titled “MRO to India: Poised to Take Off”7 indicates that developing a strong domestic MRO industry could save India at least USD 2 Billion and create nearly 90,000 jobs.

The country’s aviation sector is growing rapidly with a significant increase in passenger numbers and a substantial order book of around 1620 aircraft. According to CAPA India, this number could reach nearly 2000 aircraft by March 2025, showing strong confidence in the market’s future.

To help the MRO sector grow, the government has introduced several key measures, including allowing 100% foreign direct investment (“FDI”), reducing the Goods and Services Tax (“GST”) on MRO services from 18% to 5%, and streamlining customs processes. Updated MRO guidelines have removed royalties and clarified land allocation at airports.8

Recently, at the second Asia-Pacific Ministerial Conference on Civil Aviation, the Union Minister emphasized the need for a supportive business environment for aviation while focusing on MRO services and domestic manufacturing.

Challenges in India’s Aviation Sector

- Infrastructure Challenges

While the number of operational airports has increased from 74 in 2014 to 157 in 2024, overcrowding remains a significant issue. Many airports in India are operating beyond their designed capacities leading to congestion and delays. Despite this growth, there is a pressing need to develop additional airports that can accommodate larger passenger volumes.

Many Tier II and Tier III cities lack the necessary infrastructure, such as adequate roads and facilities, which hinders airport development in these regions. Government policies and programs are crucial in addressing this issue. For example, the UDAN (Ude Desh ka Aam Naagrik) scheme aims to enhance regional connectivity by making air travel more affordable, but its success depends on improving infrastructure in these cities.

- Operational Challenges

- Fuel Costs Strain Profitability

The Indian aviation industry recorded 6.3% growth in domestic passenger traffic for October 2024 but it faces profitability challenges due to high fuel costs and operational hurdles. The industry is expected to incur a net loss of INR 20 to INR 30 billion in FY2025 and FY2026.9 Elevated aviation turbine fuel (“ATF”) prices and ongoing supply chain issues such as engine failures and maintenance delays significantly impact airlines’ financial performance.

As of June 2024, about 15-17% of the total fleet remains grounded which limited airlines’ capacity to meet rising demand.10 Although ATF prices have stabilized in H1 FY2025, they remain 47% higher than pre-COVID levels. Moreover, the industry recorded a smaller loss of INR 10 billion in FY2024,11 but losses are anticipated to increase to INR 20-30 billion in the coming years due to high fuel prices and escalating operational costs.

- Pilot Shortage

India’s aviation sector is facing a critical pilot shortage with a deficit of about 12-15% of trained pilots. Despite having 4000-5000 newly licensed pilots unemployed, airlines prefer experienced candidates due to the high costs and lengthy training. The shortage is exacerbated by mass layoffs during the COVID-19 pandemic. There is a need for better workforce planning and government intervention to enhance pilot training programs as many airlines are expanding.

Operational challenges are evident from recent events such as Vistara canceling 10% of its flights due to pilot sick leave, Akasa Air facing disruptions from abrupt pilot resignations, and DGCA imposing fines on Air India for operating flights with non-qualified crew members.

- Impact of Airport Taxes & Charges on Air Travel

High airport taxes and charges pose significant obstacles to airport operations and increase the cost of air travel. The aviation market, being highly price-sensitive, struggles with rising costs as airlines pass these expenses onto passengers which potentially discouraging travel. This situation adversely affects demand and limits growth, particularly in regions where competitive pricing is essential.

- Financial Challenges

- Grounded Aircraft

Financial constraints have severely impacted airlines, particularly since the COVID-19 pandemic when the government ordered aircraft to be grounded. Despite some relaxations, airlines remained obligated to pay lessors which further strained their finances. Without government support, such as through the Emergency Credit Line Guarantee Scheme many airlines faced difficulties meeting financial commitments resulting in grounded aircraft. For instance, SpiceJet’s leased Boeing 737 Max planes were rendered mostly unusable due to government restrictions leading to financial default to lessors. Other affected airlines include Kingfisher Airlines, Go Airlines, and Jet Airways.

- Faulty Engines

The Indian aviation industry also faces critical supply chain challenges, particularly concerning Pratt and Whitney (“P&W”) engines. In FY2024, Go Airlines grounded half of its fleet due to faulty engines while IndiGo grounded over 70 aircraft due to similar issues. Approximately 160 aircraft are currently grounded across various Indian carriers, representing about 25% of the total fleet and significantly impacting industry capacity.

- Sustainable Aviation Fuel (“SAF”) in India

As the third-largest domestic aviation market, India confronts growing emissions, presenting both challenges and opportunities. The development and adoption of SAF could help achieve net-zero targets while stimulating economic growth. India has the potential to produce 8-10 million tonnes of SAF by 2040, exceeding the expected domestic demand of about 4.5 million tonnes.12 However, a lack of a clear regulatory roadmap complicates progress. Despite abundant feedstock availability, including agricultural waste and used cooking oil, coordinated efforts among the government, airlines, and producers are necessary to establish SAF production facilities and create a favorable investment climate. The recent inclusion of sustainable blended aviation fuel in the Union Budget 2024-25 is a positive step, but achieving carbon emission reduction targets will be challenging amidst rising air travel demand.

- Regulatory Challenges

- Drone Challenges Ahead

The rise of drones in India is spurred by technological advancements and a supportive regulatory framework. The drone market is projected to reach a valuation of INR 120- 150 billion by 2026.13 However, challenges persist, including privacy concerns due to unauthorized surveillance capabilities of drones, security risks associated with malicious uses, and the regulatory lag in keeping up with rapid technological advancements. Continuous updates to regulations by the DGCA are essential to address these challenges.

- Unified Authority for Indian Aviation Regulation

Currently, India’s aviation sector is regulated by multiple bodies including the DGCA and BCA leading to confusion and overlapping responsibilities. Establishing a single, unified authority to oversee all regulatory aspects could simplify oversight, improve efficiency, and ensure consistent enforcement of rules, enhancing accountability and streamlining operations in the industry.

Conclusion

In conclusion, while the Bhartiya Vayuyan Vidheyak Bill 2024 offers promising opportunities for India’s aviation sector challenges like infrastructure gaps, rising fuel costs, and pilot shortages must be addressed. For the Bill to be effective, it needs to create a supportive environment for sustainable growth. Additionally, it’s high time to establish aviation tribunals staffed with experts to handle industry-specific disputes efficiently. This would streamline decision-making and help resolve aviation matters more effectively. By tackling these issues, India can ensure its aviation sector thrives on the global stage.