Introduction

On 30 April 2019, the South African Revenue Service (“SARS”) published draft rules, schedules and forms for the implementation of the carbon tax and provided details on the envisaged carbon tax administration, including the registration of clients, licensing of emissions facilities, carbon tax environmental levy accounting and the application of allowances as rebates.

According to the explanatory memorandum that accompanied these rule amendments, the draft rules are proposed to come into effect on 5 June 2019.

Public comment period

The period within which the public may comment on these documents has been extended from the initial date of 20 May 2019 to 31 May 2019. Interested persons therefore have until 31 May 2019 to submit comments to: C&[email protected] or [email protected].

Preliminary comments and observations

Form DA 180, which will be the environmental levy return for carbon tax, will be added at a later stage. Carbon tax-liable entities will be expected to submit this form in July 2020 for the tax period ending 31 December 2019. The absence of this form is problematic. Historically, the collection and processing of carbon emissions data for most organisations has been the responsibility of an environmental officer and not directly within the CFO’s realm of responsibility. With a tax now imposed on carbon emissions, the CFO is expected to have a much greater involvement and, in some cases, responsibility for carbon emissions reporting.

A CFO would prefer starting from the position of checking what the DA 180 form requires and then working back from that end position to ensure that there is a framework in place to cover emissions data collection and processing to ensure accountability for these processes and reliability of information and to provide a defensible position to respond in the event of questioning from SARS. The absence of the form therefore complicates the process of establishing these internal controls. No indication has been given when this form will be published.

The implementation date for the carbon tax has been stipulated as 5 June 2019 even though the public comment period for the draft rules ends a few days earlier on 31 May 2019. Furthermore, two sets of regulations (the trade exposure regulations and the performance allowance regulations) have not yet been published for comment. The 2019 Budget Review stated that these documents would be published for public comment in February 2019 and March 2019 respectively. It would seem reasonable that given the delay in the publication of these documents that the implementation date for carbon tax should also have been pushed out in order to give taxpayers sufficient time to consider these regulations prior to the introduction of the carbon tax.

Overview of the draft rules

These draft rules apply to:

- the carbon dioxide (CO2) equivalent of greenhouse gas emissions generated in South Africa that is liable to environmental levy in terms of item 157.00 of section F of Part 3 of Schedule No. 1;

- the licensing of an emissions generation facility as a customs and excise manufacturing warehouse;

- the registration of a person who operates emissions generation facilities at a capacity prescribed in the rules;

- the calculation of the amount of environmental levy payable in respect of a licensed emissions generation facility for each tax period;

- the submission of account and payment of environmental levy in respect of emissions generated in a licensed emissions generation facility; and

- other matters relating to the administration of environmental levy for the purposes of Chapter VA.

Licensing and registration

Every person who operates emissions generation facilities at a combined capacity equal to or above the carbon tax threshold must license each emissions generation facility as a customs and excise manufacturing warehouse.

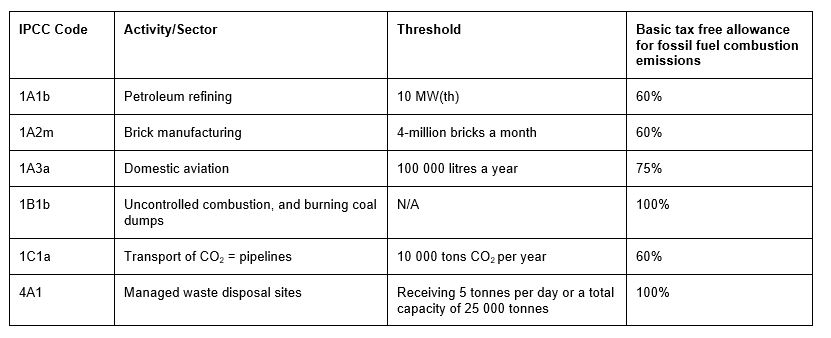

An emissions generation facility/ies is considered to be one or more emissions generation points where the source category activity of the same IPCC code occurs. An emissions generation point is the place where emissions liable to environmental levy are generated. The carbon tax threshold means the number determined by matching the activity listed in the column “Activity/Sector” with the value reflected in the corresponding line of the column “Threshold” in Schedule 2 of the Carbon Tax Act. Below is an extract from Schedule 2 from the Carbon Tax Bill.

Table: Extracts from Schedule 2 to the Carbon Tax Bill

Thus, a petroleum refiner that has three emissions generation facilities of 4MW each is obliged to license each emissions generation facility as a customs and excise manufacturing warehouse, as the combined capacity of the three emissions generation facilities exceeds 10MW. If the petroleum refiner has three emissions generations facilities of 3MW each, then the combined capacity will be below the applicable carbon tax threshold of 10MW. In such a case, the petroleum refiner must register in terms of section 59A of the Customs and Excise Act, 1964 and the its rules. It is apparent from the extracts from Schedule 2 that the threshold differs with the particular type of activity. Importantly, the obligation to register an emissions generation facility is placed upon the person who operates the emissions generation facility; not the person who owns the emissions generation facility. Also, the test is whether the combined capacity of the emissions generation facility is equal to or above the carbon tax threshold.

Certain types of persons are not required to license nor are they required to register their emissions generation facilities. These are persons who operate emissions generation facilities in respect of which the carbon tax threshold is not applicable or an allowance for fossil fuel combustion of 100% applies. Thus, taxpayers who operate emissions generation facilities where coal dumps are burned or managed waste disposal sites are not required to license or register their facilities, as no carbon tax threshold is applicable or a 100% allowance for fossil fuel combustion applies, or both.

The calculation of the amount of environmental levy payable

Every licensee must calculate the amount of environmental levy payable for each tax period in respect of each of its licensed emissions generation facility in the manner set out in the draft rules. A tax period in relation to a taxpayer is:

- from a date determined by the minister in the Government Gazette ending on 31 December of the year in which that date is determined. If the carbon tax is passed into law on 5 June 2019, then the first tax period will be 5 June to 31 December 2019; and

- subsequent to the period contemplated in paragraph 1, the period commencing on 1 January of each year and ending on 31 December of that year.

Submission of account and payment

Every licensee must submit, for each tax period, a separate annual account on form DA180 in respect of each licensed emissions generation facility of that licensee; pay the environmental levy as calculated on the said form DA180 and its annexures in accordance with rule 54FD.03 and submit any supporting documents the commissioner may require.

The licensee must submit the documents and payment in the month of July of the year following the tax period but not later than the penultimate working day of that month. Thus, if carbon tax is passed into law on 5 June 2019 then the first account must be submit in July 2020.