The amendments to the Indian Stamp Act 1899 (Act) have come into effect from 1 July 2020. These amendments were first proposed under the Finance Act of 2019 and the Indian Stamp (Collection of Stamp-Duty through Stock Exchanges, Clearing Corporations and Depositories) Rules, 2019 (Rules).

The amendments are intended to facilitate ease of doing business and bring in uniformity in stamp duty payments on issue and transfer of securities and have introduced substantial changes to the erstwhile stamp duty regime. The amendments relate not only to the rates of stamp duty but also to the process of levying and collecting stamp duty. The stamp duty regime has undergone a fundamental change since the taxable event has shifted from ‘execution of an instrument listed in the schedule’ to a ‘corporate action pertaining to a transaction’. This paradigm shift may be subjected to judicial scrutiny for examining its constitutional validity.

We have summarized below certain key aspects of these amendments and its impact on the Mergers & Acquisitions (M&As) in India – i.e. issuance by and transfer of securities of public and private companies.

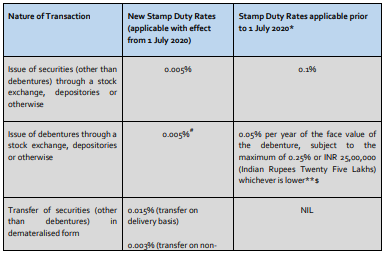

A. Revision in Stamp Duty Rates (Comparative Analysis)

*For comparison purposes, we have relied on the stamp duty rates under Maharashtra Stamp Act 1958.

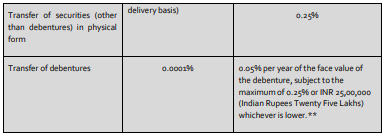

**payable on debentures being marketable securities

# Prior to the amendment to the Act, only debentures being ‘marketable securities’ were liable to be stamped under Article 27 of Schedule I to the Act which deals with stamp duty on Debentures. The amended Article 27 omits the words “being a marketable security”. The Act therefore now seeks to levy stamp duty on issue of all types of debentures – marketable or otherwise.

$ Further, the Amendment seeks to withdraw the exemption from payment of stamp duty on Debentures if the Debentures were issued in terms of a duly stamped registered mortgage deed or debenture trust deeds. The withdrawal of the exemption would lead to enhanced transaction costs for companies borrowing funds by means of issue of securities.

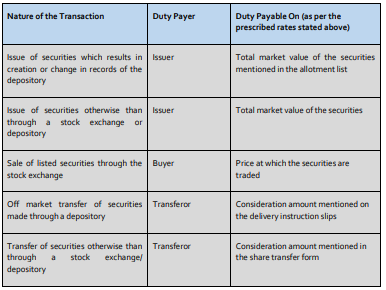

B. Onus of payment and amount on which stamp duty is calculated

C. Onus of payment and amount on which stamp duty is calculated

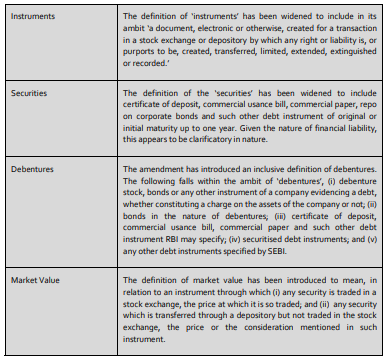

1. Changes to key definitions

2. No exemption for transfer of securities in dematerialized form

Prior to the amendment, by virtue of Section 8A of the Act, stamp duty was not payable on the transfer of shares in dematerialized form. This made transfer of shares in the dematerialized form an attractive proposition due to reduced costs. However, Section 8A of the Act has now been amended and stamp duty exemption available for transfer of shares in dematerialized form has been done away with.

3.Collection of Stamp Duty

The amendment has introduced several changes to the process of collection of stamp duty in case of issuance, transfer or sale of securities through stock exchange or depositories. In case of,

(i)sale or transfer of securities on the stock exchange, stamp duty shall be collected by the stock exchanges or clearing corporations; and

(ii)in case of off market transfer of shares through the depositories or issuance of securities which results in creation or changes in the records of the depository, stamp duty will be collected by the depository.

There have been no significant changes made to the manner in which stamp duty is levied and collected in case of issuance and transfer of securities in physical form.

Comments:

The amendments have introduced a uniform system for collection and payment of stamp duty on the issue and transfer of securities. These changes will certainly bring affordability in the stamp duty at least in some states and are likely to avoid practice of choosing states where the stamp duty rates are lower. This rationalized and harmonized system through centralized collection mechanism is expected to ensure minimization of cost of collection and enhanced revenue collection.