More and more work is being done under the form of a joint venture (“JV”), particularly on rail and infrastructure projects. JVs present opportunities for parties to spread financial risk (including costs and liabilities) whilst pooling their resources and expertise to provide a well-rounded and innovative offering to their clients. Such arrangements are particularly common at the pre-qualification and tender stages of a project.

Whilst there is no legal or fixed definition of a JV, a JV can essentially be defined as a commercial arrangement between two or more economically independent entities that collaborate to achieve a particular objective. It can take one of the following basic legal forms:

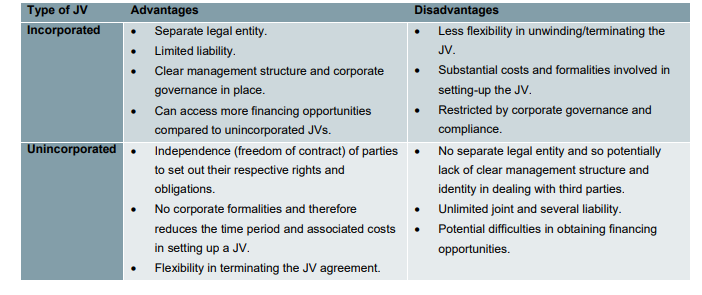

1. an incorporated JV e.g. a limited liability company or a limited liability partnership;

2. an unincorporated joint venture e.g. a contractual co-operation agreement / JV agreement; and

3. a partnership (or limited partnership).

The most common types of commercial JVs are incorporated and unincorporated.

Incorporated or unincorporated JV?

Considerations in forming a JV

Considerations in forming a JV

Prior to entering into a JV relationship, less and less consideration is given by parties to the associated risks. There is often the attitude among parties that the JV relationship will be fine. However, such an attitude could be detrimental in the event that the JV does not work out e.g. one of the partners becomes insolvent or there is a dispute between the parties. Such issues could have a detrimental impact on the partners’ reputations and also result in financial losses. Therefore, it is important that each partner considers, from the outset, the following key issues:

1. Culture/values – to avoid disputes between the JV partners, the partners should consider each other’s cultures, values and appetite for risk and whether or not they align.

2. Financial due diligence – in light of the current economic climate in addition to the recent insolvencies the construction industry has witnessed, it is important that the partners carry out financial due diligence on one another to satisfy themselves of each other’s solvency e.g. credit checks and Companies House searches.

3. Liability – in case one of the JV partners becomes insolvent, parent company guarantees should be obtained by each JV partner. If the JV is unincorporated, each partner should also seek cross-indemnities from the other.

4. Separate identity of the JV partners – collocation of the JV partners can often mean that it is difficult to distinguish between the different partners. Parties need to ensure that they maintain their own branding and that they retain ownership of their intellectual property rights as well as those which they develop on the project.

5. Split of the scope of work – in respect of unincorporated joint ventures, each partner will want to ensure that it is only liable for the work that it performs. Therefore, the scope of work should be clearly split and allocated to each JV partner accordingly, with each JV partner taking responsibility and providing resources for their own split of the work.

6. Insurance – it is important that there is insurance in place to cover both the JV entity and each JV partner. Partners should consider taking out project specific insurance, which can ensure the activities of the JV are insured, although this comes with an additional cost. Alternatively, each JV partner can rely on its existing insurance policies, however, this could cause issues in respect of differing levels of excess and indemnity and coverage issues. If JV parties choose to rely on their individual insurance policies they should consider how notification of potential claims are dealt with under their individual policies.

7. Disputes – consideration needs to be given as to how disputes with the client and sub-contractors are to be dealt with, in particular in respect of payment disputes. It is essential that the JV Partners agree from the beginning which partner will operate the contract on behalf of the JV and who will instruct lawyers (instead of ending up with three different sets of lawyers), who will incur the costs and who has the authority to settle a dispute on behalf of the JV. With respect to disputes within the JV arrangement, the JV parties should set out a mechanism for resolving disputes between the partners.

The form of JV agreement

Whilst FIDIC have published a standard form agreement for cross-border JVs, there is no standard form of agreement for domestic JVs. As JVs are on the rise, including multi-party JVs (we have recently seen a JV comprised of five partners), a standard form JV agreement would be very welcome. Such an agreement would mean a standard approach to JVs across the UK construction industry and would enable partners to more easily enter into JVs and adequately manage their liabilities and maximise the opportunities available.

International JVs – choice of law/court

Often one of the main issues in respect of cross-border JVs, is obtaining consensus from the partners on the choice of law and which court the JV agreement will be subject to. Whilst the laws and jurisdiction of the courts of England and Wales are internationally recognised and respected and preferable from a UK perspective, there may be resistance from foreign JV partners. When considering the choice of law and jurisdiction, the parties need to consider factors including amongst others, the location of the project and taxation implications.