Long-awaited proposed regulations recently released by the Department of the Treasury (Treasury) and the Internal Revenue Service (IRS) address the classification of certain transactions involving digital content and the source of income from such transactions (the Proposed Digital Content Regulations) and move toward a comprehensive basis for classification of so-called “cloud transactions,” involving on-demand network access to computing resources (the Proposed Cloud Regulations, and together with the Proposed Digital Content Regulations, the Proposed Regulations). See REG-130700-14.

- Proposed Digital Content Regulations:

- Expand the scope of the existing 1998 regulations addressing software to include digital content such as audio books, music and movies, or any other content in digital format either currently protected by copyright law or formerly protected by copyright law solely due to the passage of time;

- Propose new rules for determining the source of a sale or transfer of certain types of digital content, generally by reference to the location of end-user download or installation.

The Proposed Regulations provide greater certainty for taxpayers with respect to the US federal tax treatment of increasingly common transactions, but also leave numerous significant points unaddressed, including particularly the rules for determining the source of income from cloud transactions. This question may well have broader implications as countries are debating proposals for the taxation of the digital economy.

Overview

The Proposed Regulations build upon the framework that was established in the software characterization regulations found in Treas. Reg. § 1.861-18, which were issued in 1998 (the 1998 Regulations).

The 1998 Regulations are limited in scope to the classification of transactions involving “computer programs,” which are generally defined as a set of instructions used by a computer to bring about a certain result. The Proposed Regulations would expand the scope of transactions covered by the 1998 Regulations in two ways:

- The Proposed Digital Content Regulations would broaden the scope to cover all digital content (i.e., digital content or any other content in digital format either currently protected by copyright law or formerly protected by copyright law solely due to the passage of time), not just computer software. Under this definition, the medium of transfer (e.g., transfer of digital content copied onto a physical disk versus download of digital content) is not relevant to characterization of a transaction, but as discussed below, may impact the source of a sale or transfer of certain types of digital content;

- The Proposed Cloud Regulations would cover cloud transactions (i.e., transactions involving on-demand network access to computing resources).

Proposed Digital Content Regulations

Copyright Right vs. Copyrighted Article. The Proposed Digital Content Regulations change the term “computer software” to “digital content,” thus maintaining the existing approach, which distinguishes between a transfer of a copyright right and the transfer of a copyrighted article. The distinction between a copyright right and a copyrighted article under the 1998 Regulations is based upon whether the transferee has the ability to make copies of the computer software, the right to prepare derivative computer software, the right to make a public performance, or the right to publicly display the computer software. If the transferee has any of these rights, it generally is considered to have acquired a copyright right.

The use of the term “digital content” rather than “computer software” under the Proposed Digital Content Regulations requires that these same standards be used for purposes of determining the character of income from transactions in electronic books, videos and music. A limited exception is provided in the Proposed Digital Content Regulations with respect to the transfer of a mere right to public performance or display of the digital content for advertising purposes. The Proposed Digital Content Regulations provide that such a transfer does not constitute a transfer of a copyright right.

Eversheds Sutherland Observation: The preamble to the Proposed Regulations indicates that the IRS and Treasury believe that the Proposed Regulations are consistent with the manner in which most taxpayers treat digital content transactions today. Thus, this is not expected to be a significant change, but will ensure consistency in treatment by taxpayers.

Character of Digital Content Transactions. Under the 1998 Regulations, the transfer of a copyright right is treated either as a sale or a license, and the transfer of a copyrighted article is treated as either a sale or a lease. The Proposed Regulations expand this character to all digital content.

The Proposed Digital Content Regulations maintain the 1998 Regulations’ methodology for distinguishing between sales and licenses of a copyright (based upon whether all substantial rights in the copyright have been transferred) and between sales and leases of copyrighted articles (based upon whether sufficient benefits and burdens of ownership have transferred).

To illustrate the expansion of the definition of “computer software” to include all “digital content,” the Proposed Digital Content Regulations add three new examples. Each of these examples describes scenarios from the current digital economy, including,

- The transfer of an electronic book, which is treated as a license of a copyright right to the seller of the electronic book, and a sale of copyrighted article in the case of the purchase by the consumer;

- A music subscription service that requires downloads of content but limits access to the subscription term, which is treated as a transfer of copyrighted articles for a limited term, and therefore a lease; and

- A digital television and movie service that allows multiple options for accessing content, including purchase, rental, and a “streaming” option where content can be accessed only online, which is treated as a sale in the case of a purchase, a lease in the case of a rental, and a “cloud transaction,” which is characterized under the Proposed Cloud Regulations, in the case of the streaming option.

The examples provide helpful guidance to determine whether a transfer is a sale, a license or a lease, as well as to distinguish between a transfer of a copyright right and the transfer of a copyrighted article in the case of digital content, including addressing the effect of limitations on the ability to duplicate or access content that is provided electronically.

Eversheds Sutherland Observation: The examples generally treat access to digital content in the same manner that rights with respect to a physical book, CD or DVD are treated. Thus, the purchase of an e-book or a movie is treated as the purchase of a copyrighted article, even though it can be viewed only on a specific device and the purchaser is limited in its right to duplicate the book. Similarly, a music or movie download that is available only for the term of the user’s subscription is treated as a lease. The fact that the user retains a copy is not significant because an electronic lock prevents access to the copy after the subscription ends.

The treatment of subscription models that allow for online access as well as downloads of content are not clearly addressed by the examples. Although Example 9 addresses the characterization of streaming subscription services, while Example 10 addresses the characterization of downloaded digital content as subject to § 1.861-18, no example addresses the streaming service that also permits limited downloads of digital content. Most services that provide streaming options today also allow for digital downloads for limited periods of time. The current regulations provide that any transaction consisting of more than one of the categories of transactions under the regulations is treated as separate transactions unless one of the transactions is “de minimis, taking into account the overall transaction and the surrounding facts and circumstances.” In the case of a streaming service, the right to download is arguably incidental to, and therefore, “de minimis.” But, clarification through additional examples in the final regulations would be welcomed.

It is also unclear under the Proposed Regulations how purchase price is to be allocated among items that are downloaded pursuant to a subscription service that requires users to download content. The examples indicate that each download is considered to be a lease, but no indication is made as to how to allocate the subscription fee to each leasing transaction. It is administratively difficult to allocate subscription price to individual downloads, and likely will result in inconsistent treatment of economically similar transactions. The treatment of all subscription services as “cloud transactions,” regardless of any right to download content, could ensure consistent treatment of economically similar transactions.

Special Source Rule for Electronic Transfers of Copyrighted Articles. The Proposed Regulations also deem the sale or lease of copyrighted articles to have occurred at the location of download or installation onto the end-user’s device used to access the digital content for purposes of the passage-of-title rule. The effect of this special rule is to source income from such transactions at the location of download or installation where the passage-of-title rule applies. Where information about the actual location of download or installation is absent, taxpayers may use recorded sales data for business or financial reporting purposes as a proxy.

Eversheds Sutherland Observation: It is unclear under what circumstances download location information will be considered “absent,” or how taxpayers may demonstrate the absence of such information. In this regard, the Proposed Regulations could be read to require sellers of digital content to build new systems that track the location of digital download.

Download location is also subject to manipulation, and may not accurately reflect the location where an electronic sale of a copyrighted article is commercially complete. The preamble to the Proposed Regulations specifically requests comments regarding the availability, reliability and cost of download location information. As an alternative, consideration may be given to using customer address or similar customer identification information.

The focus on download location also may have implications for the broader international tax discussion regarding taxation of the digital economy. Many digital tax proposals focus on the location of download to support digital taxation rights.

Proposed Cloud Regulations

Cloud Transactions. The examples in the Proposed Digital Content Regulations provide that access to an online streaming service is treated as a “cloud transaction,” which is subject to the new Proposed Cloud Regulations. The Proposed Cloud Regulations define a “cloud transaction” as a transaction through which a person obtains on-demand network access to computer hardware, digital content, or other similar resources. Under the Proposed Regulations, a cloud transaction is classified as either:

- A lease of computer hardware, digital content, or other similar resources; or

- The provision of services.

Character of Cloud Transactions. To determine whether a cloud transaction is classified as a lease or as the provision of services, the Proposed Cloud Regulations build on existing services versus lease factors found in § 7701(e) and in case law. The non-exhaustive list of factors in the Proposed Cloud Regulations generally includes whether the recipient has: physical possession of the property; control of the property; significant economic or possessory interest in the property; no risk of substantially diminished receipts or increased expenses from nonperformance under the contract; no concurrent use of the property; and whether the total contract price exceeds rental value of the property for the contract period.

The Proposed Cloud Regulations also provide 11 examples to illustrate the application of these factors across a variety of digital transactions, including access to data center servers, access to online software or software development platforms, access to online databases, streaming services, and data storage. Notably, in every case where the transaction is determined to be a cloud transaction, it is treated as a provision of services. In this regard, the preamble to the Proposed Cloud Regulations requests taxpayers to identify examples of cloud transactions that would be characterized as leases rather than as the provision of services.

The general rule under the Proposed Cloud Regulations is that a cloud transaction is classified as either a lease or a services transaction, and if an arrangement comprises multiple transactions, each is classified separately unless it is “de minimis,” taking into account the overall arrangements and facts and circumstances. This mirrors the rule for multiple transactions in the 1998 Regulations. An example in the Proposed Cloud Regulations illustrates the application of this rule where a customer enters into an agreement for access to offline software and data storage capacity. The access to offline software is treated as a digital content transaction, and the agreement for data storage is treated as a cloud transaction. In the example, there are separate agreements for the access to offline software and data storage, and each can be contracted for separately.

Eversheds Sutherland Observation: Understanding the parameters for determining when a single transaction may be bifurcated into components will be important in applying the Proposed Cloud Regulations. The examples address the easy case where each component transaction could be purchased separately. Offers or purchases of packaged transactions represent a more difficult case, and the Proposed Cloud Regulations may require separately allocating consideration to the various components in the package for purposes of determining the character of income and expense from such transactions.

Source of Cloud Transactions. The Proposed Cloud Regulations do not address the source of income from cloud transactions. Comments are requested regarding the proper rules for determining source of income from cloud transactions.

Eversheds Sutherland Observation: Income from services generally is sourced to the location in which the services are performed. While the Proposed Cloud Regulations do not change this result, they also do not provide additional guidance with respect to how this general rule applies to cloud transactions (i.e., where such services are performed). In theory, drawing on international proposals with respect to the digital economy, the location of services could be based upon where servers that provide on-demand network access are located, where such services are consumed, or some combination of factors. Any of these approaches would be a marked shift from current US rules. Whether any inference about the IRS and Treasury’s leanings on this question could be gleaned from the use of download location for sourcing sales of copyright articles in the Proposed Digital Content Regulations remains to be seen.

In this regard, the source of income from cloud transactions is closely tied to international discussions regarding the taxation of the digital economy. While services income traditionally has been sourced to the location in which income-producing activity occurs, proposals to tax digital services transactions increasingly emphasize the location of the user.

Application of the Proposed Regulations

The Proposed Regulations apply for purposes of all of the international tax provisions of the Internal Revenue Code, and for purposes of § 59A Base Erosion Anti-Abuse Tax and § 250 foreign-derived intangible income rules. The Proposed Regulations are proposed to be effective for contracts entered into after the date that the Proposed Regulations are published as final.

Eversheds Sutherland Observation: Characterization of a payment as a lease, rather than as a service, under the Proposed Cloud Regulations could have implications for whether such payment is treated as a “base erosion payment” under § 59A. Specifically, characterization may have implications for whether the “services cost method” exception is available, and whether the payment is properly attributable to the cost of goods sold.

Change in Method of Accounting

The Proposed Regulations note that the new rules when applicable may require certain taxpayers to change their methods of accounting for affected transactions. In this regard, the Proposed Regulations require that such changes in method of accounting must be implemented pursuant to applicable regulations and administrative procedures governing voluntary changes in method of accounting.

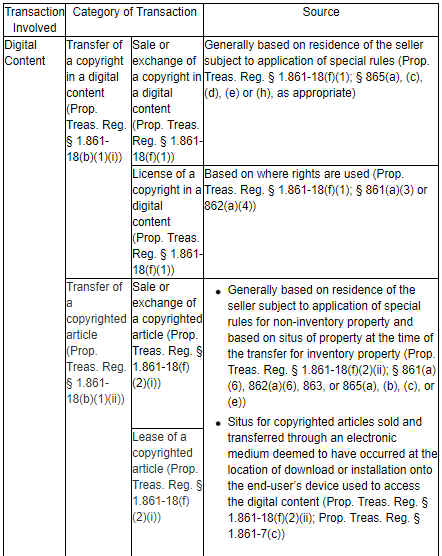

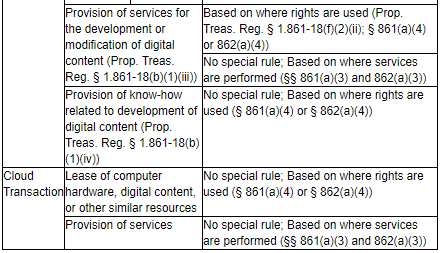

Summary Chart