A European legislative initiative aimed at requiring companies to undertake human rights and environmental due diligence is gradually but steadily making its way through the EU institutions.

Previously, on March 10, 2021, the European Parliament (the “Parliament”) adopted a resolution with “recommendations to the Commission on corporate due diligence and corporate accountability,” setting the stage for what would be a comprehensive, EU-wide due diligence mandate designed to foster responsible business conduct.

The Corporate Sustainability Due Diligence Directive (“CSDDD” or the “Directive”), which was then formally proposed by the European Commission (the “Commission”) on February 23, 2022, seeks to oblige companies based or operating in the EU to identify, assess, prevent, and mitigate adverse human rights and environmental impacts arising from their activities. Following the Commission’s proposal, the Council of the European Union (the “Council”) adopted its negotiating position on the CSDDD on December 1, 2022.

Most recently, on April 25, 2023, the Parliament’s Committee on Legal Affairs (“JURI Committee”) voted in favor of adopting a compromise text in response to the Commission’s proposed CSDDD, with amendments specifying details about the scope of companies and sectors to be covered under the legislation. The text approved by the JURI Committee—which has not been formally released—is now on its way to a full plenary vote at the Parliament in June 2023.

As evident from recent developments, the CSDDD is nearing the trilogue negotiations phase among the Commission, the Council, and the Parliament. The negotiations are expected to be vigorous, given the three EU institutions’ varying approaches to some of the key provisions of the CSDDD. These include:

- Employee and turnover thresholds for EU and non-EU companies to be covered under the Directive;

- Applicability of due diligence requirements to companies in the financial sector;

- Scope of operations to be covered by due diligence requirements, particularly with respect to companies’ upstream and downstream business relationships and activities;

- Scope of human rights and sustainability issues to be addressed through due diligence requirements;

- Corporate directors’ fiduciary duties and companies’ civil liability for damages caused by failure to comply with the Directive.

In this article, we discuss the respective proposals of the Council and the Parliament’s JURI Committee on the CSDDD and what companies can expect to see in the coming months.

Corporate Sustainability Due Diligence Requirements at the EU Level

As discussed in our previous client alert, the Commission’s proposed text of the CSDDD requires large companies based or operating in the EU to conduct human rights and environmental due diligence on their operations, as well as those of their subsidiaries and upstream and downstream value chains. In response, and in accordance with the EU legislative adoption process, the Council and the Parliament reviewed the Commission’s proposed text and subsequently developed their respective negotiating positions on the CSDDD.

- Council’s Negotiating Position

On December 1, 2022, the Council adopted its negotiating position on the CSDDD. While the Council’s position repeats many of the requirements of the Commission’s proposal, it contains a number of noteworthy amendments.

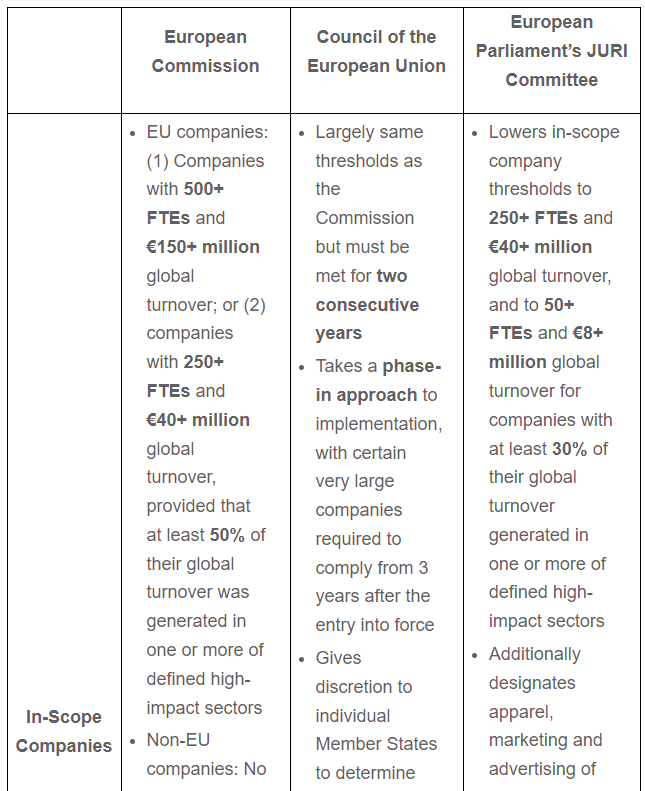

- Phased-In Approach: Although the Council retained the Commission’s proposed employee and revenue thresholds for determining in-scope companies, it introduced a phased-in period to allow certain companies additional time to comply with the CSDDD’s requirements. Under the Council’s approach, the CSDDD would first apply to “very large companies” with more than 1,000 employees and €300 million net worldwide turnover (for non-EU companies, €300 million turnover generated in the EU) beginning in three years from the Directive’s entry into force, before it is applied to other in-scope companies.

- Applicability to Financial Sector: Unlike the Commission’s proposal, the Council’s position seeks to make the applicability of the CSDDD to financial services companies optional for Member States. Thus, under the Council’s version of the Directive, Member States would be able to determine whether to include financial services companies within the scope of the CSDDD when implementing the Directive into national law.

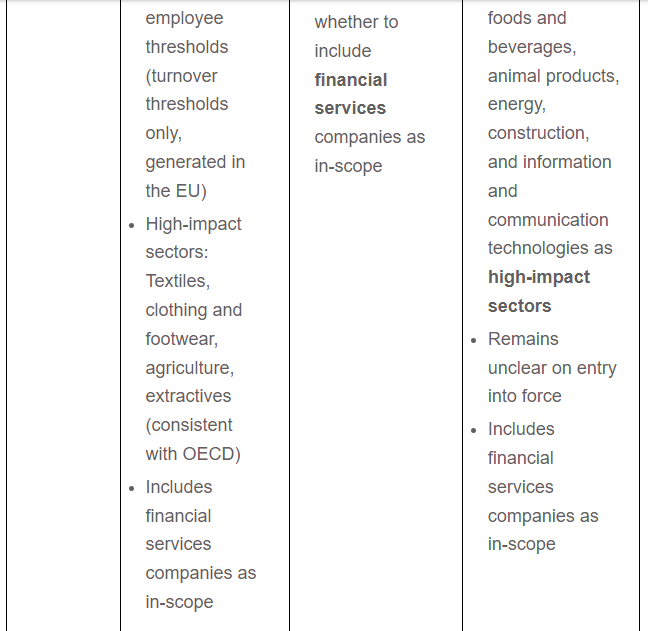

- Extent of Due Diligence Obligations: The term “value chain” within the Commission’s proposal has been replaced with the narrower concept of “chain of activities” that largely encompasses suppliers and excludes the downstream users of companies’ products or services. This amendment, if incorporated into the final text of the Directive, would significantly reduce diligence obligations that were originally envisioned by the Commission—to apply directly or indirectly to nearly every significant company in the world.

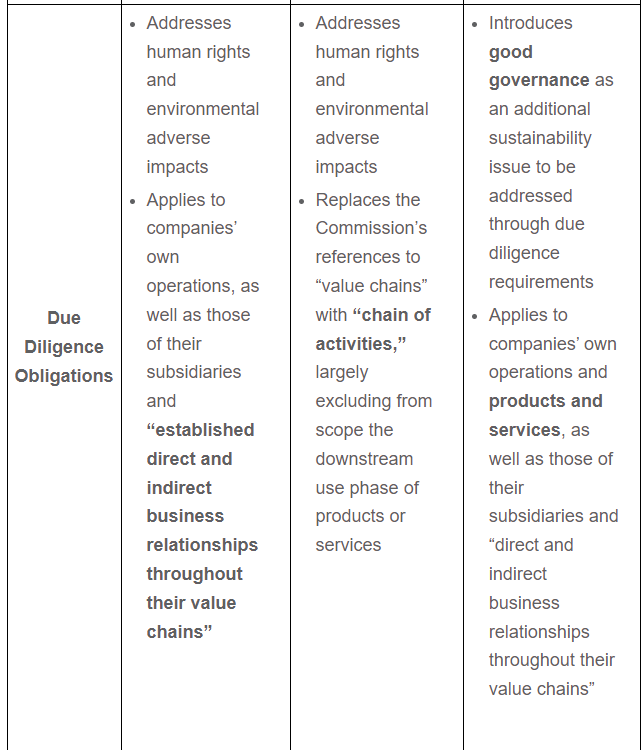

- Directors’ Duties: The Commission’s proposal linked directors’ remuneration to the company’s long-term value and sustainability. However, the Council deleted the relevant provisions in its position, mainly in response to concerns expressed by Member States regarding interference with national laws governing corporate directors’ duty of care.

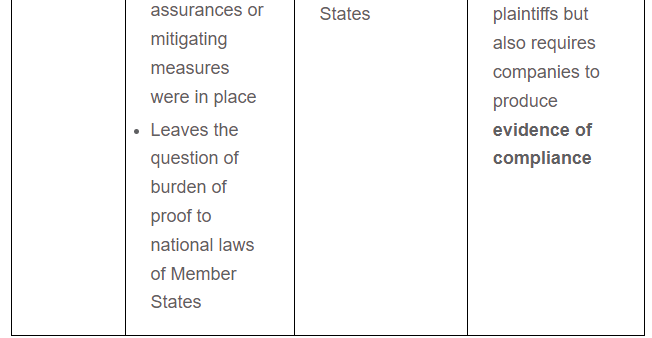

- Civil Liability: Under the Council’s approach, in-scope companies can be liable for damages caused by intentional or negligent failures to comply with the CSDDD’s requirements, but not when such damages are caused solely by their direct or indirect business partners. This deviates from the conditions of civil liability outlined in the Commission’s proposal, which excludes liability where the damage is caused only by companies’ indirect business partners.

- Amendments Proposed by the Parliament’s JURI Committee

On April 25, 2023, after a prolonged internal debate, the Parliament’s JURI Committee voted to approve a compromise text outlining its position on the CSDDD. While the final version of the compromise text has not yet been made public, on balance, the JURI Committee’s draft report takes multiple steps further on due diligence obligations than the Commission’s proposal or the Council’s position, signaling a bumpy road ahead to the trilogue.

- In-Scope Companies: The JURI Committee’s draft report significantly expanded the scope of companies to be covered under the CSDDD by lowering the relevant employee and turnover thresholds. Under the JURI Committee’s approach, EU companies with more than 250 full-time employees and a worldwide net turnover exceeding €40 million would be subject to the requirements of the CSDDD. For companies in designated high-impact sectors, the thresholds are further lowered to 50 full-time employees and a global turnover of €8 million. Non-EU companies would be subject to the same turnover thresholds (but not employee thresholds) generated in the EU.

- High-Impact Sectors: The JURI Committee also proposed a longer list of high-impact sectors to additionally include apparel, marketing and advertising of foods and beverages, animal products, energy, construction, and information and communication technologies, among others.

- Scope of Due Diligence Obligations: Largely consistent with the Commission’s proposal, the JURI Committee seeks to oblige companies to conduct due diligence on their own operations, as well as those of their subsidiaries and “direct and indirect relationships throughout their value chains.” In addition, the JURI Committee seeks to direct companies to perform diligence with respect to their products and services, adding emphasis on adverse human rights and environmental impacts that could arise from the use of companies’ products and services.

- Due Diligence Criteria: Notably, the JURI Committee seeks to introduce good governance—defined as “the proper functioning of public administration and services, the rule of law, democratic electoral systems, and freedom of expression”—as an additional sustainability issue to be addressed through the Directive’s due diligence requirements. According to the JURI Committee’s draft report, adverse good governance impact could result from bribery, corruption, blackmail, tax evasion and avoidance, and illegal political funding or exercise of influence.

- Climate Transition Plan: Whereas the Commission’s proposal and the Council’s position only require companies to adopt a climate transition plan in line with the Paris Agreement, the JURI Committee’s draft text explicitly requires that companies adopt and effectively implement such a plan.

- Civil Liability: The JURI Committee’s draft report omitted the Commission’s proposed safeguard to protect companies from civil liability where damages were caused solely by adverse impacts arising from activities of an indirect business partner, and where there were contractual assurances or mitigating measures in place.

- Key Anticipated Points of Discussion

The CSDDD will be subject to negotiations among the Commission, the Council, and the Parliament, with a great deal of formal and informal discussions expected to take place in the coming months. While we cannot exhaustively present all the differences between the various texts, and noting that the JURI Committee’s final compromise text has not been released, the following areas are anticipated to be the key points of debate and where future changes might occur:

What to Expect Next

Once the entirety of the Parliament has agreed on its official position on the CSDDD, the Parliament will enter into negotiations with the Commission and the Council. With key differences between the Commission, the Council, and the Parliament in their approaches to the CSDDD, companies can expect tense discussions and active stakeholder participation in the coming months. However, the political momentum to finalize the Directive is strong, and Spain—which will take the chair of the Council in the second semester of 2023—has already announced that it intends to make the CSDDD a high priority. Taken together, these latest developments in the EU signal that corporate human rights and environmental due diligence is here to stay as a business imperative.