On 17 December 2025, the European Commission (“Commission”) proposed a new regulation to amend the existing Carbon Border Adjustment Mechanism (“CBAM”). This proposal (“extension proposal”) for amending Regulation (EU) 2023/956 intends to extend CBAM’s scope to downstream goods of iron, steel, and aluminium and strengthen anti-circumvention provisions. This proposal would increase compliance and cost pressure on Indian industries that use iron, steel, and aluminium, as the expanded scope will impact USD 1.1 billion worth of additional Indian exports to the European Union (“EU”).

I. Let’s recap. What is CBAM?

The EU wants to become the world’s first climate-neutral continent by 2050. To meet this goal, the EU has established a binding intermediate target to reduce net greenhouse gas emissions by 90% by 2040.

An important part of this strategy is the EU Emissions Trading System (“EU ETS”), launched in 2005. Operating on a "cap-and-trade" principle, it requires domestic industries in carbon-intensive sectors to pay for every tonne of carbon they emit.

However, the EU ETS has created a dual challenge for the EU industry. While it has helped cut emissions within the EU, it has also made production of these goods within the EU more expensive. Increased carbon prices at home have incentivised businesses to relocate production to jurisdictions with less stringent environmental rules and encouraged downstream industries to import cheaper, carbon-intensive goods. This phenomenon, known as carbon leakage, has undermined the effectiveness of the EU ETS. Instead of reducing global emissions, the EU lost industrial jobs and economic growth without achieving a net climate gain. A recent communication from the European Commission highlights the severity of the situation, noting that EU producers can currently meet only 90% of domestic steel demand and 46% of aluminium demand.

To address carbon leakage, the EU introduced CBAM in May 2023. CBAM imposes a carbon price on imports of six carbon-intensive sectors, namely cement, aluminium, iron and steel, hydrogen, electricity, and fertilisers (“CBAM goods”). Under CBAM, the foreign producers must calculate and report their emissions for CBAM goods to EU importers. The EU importers would then, based on these emissions, pay a carbon price based on the underlying emissions of their imports. This mechanism creates reporting and compliance obligations on foreign producers and forces them to be more carbon efficient, as there is a price attached to their emissions. For example, producing one tonne of pig iron or crude steel in India using coal-based blast furnaces results in direct emissions of approximately 2.18 MT of CO₂. After accounting for free allocation adjustments, the CBAM cost would be about €90 per tonne based on actual emissions, rising to €140 per tonne if default values apply. Downstream products would incur even higher costs. EU importers are unlikely to absorb this entire cost, meaning a significant portion will be passed on to Indian exporters, thus impacting profitability, resulting in market loss to other competitors who would be efficient in managing emission technologies and methodologies.

II. What is CBAM Downstream Extension & Anti‑Circumvention Proposal?

The CBAM extension proposal seems to primarily target two objectives –

- Expand CBAM’s scope to include downstream goods of aluminium, iron and steel.

- Prevent circumvention by introducing safeguards against practices that could undermine CBAM compliance.

III. Why expand CBAM scope?

Currently, CBAM applies to basic goods such as iron and steel sheets, pipes, and aluminium ingots, which are intermediates for downstream products. The EU Commission estimates that downstream producers face a dual cost push:

- The phase out of free allowances under the EU ETS is expected to increase the cost of domestically procured CBAM goods.

- Implementation of CBAM will increase the import cost of CBAM goods.

This combination incentivises relocation and carbon leakage, since an EU producer could relocate to a non-EU location, import CBAM goods into that jurisdiction, manufacture downstream goods and export them to the EU without any carbon tax. The extension seems to be intended to prevent this kind of circumvention.

IV. How is the Indian downstream industry affected?

Which sectors are targeted: The extension proposal targets downstream products of iron and steel, and aluminium. It proposes to cover articles of iron & steel, articles of base metals, mechanical and electrical machinery and equipment. It would cover products like grills, netting and fencing, nails, furniture fittings, automobile parts (like engines, gearboxes, pumps), cooling towers, washing machines, AC/DC motors, and wires. These categories include Indian exports worth at least USD 1.1 billion to the EU.

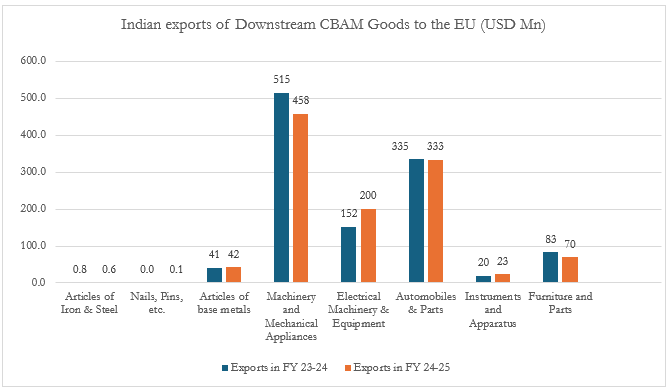

Current export exposure: The following graph depicts the export value of Indian downstream goods to the EU–

The data indicates that the extension proposal would primarily affect industries like automotive components, mechanical and electrical machinery, and furniture fittings. Among these, the automotive components industry stands out as the most vulnerable, given its heavy reliance on the European market, which accounts for approximately 27% of its total exports. The industry has set an ambitious target to triple its overall exports from USD 20 billion to USD 60 billion by 2030. However, achieving this goal will require navigating the compliance challenges of CBAM, which are likely to become one of the most critical hurdles for maintaining competitiveness and market access.

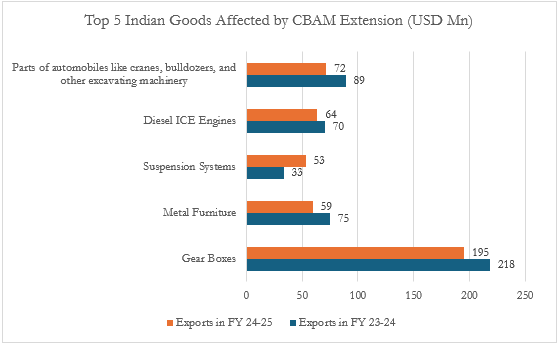

Within the sector, the top 5 Indian goods likely to be affected are as follows:

V. How are embedded emissions in downstream products calculated?

Embedded emissions for downstream products would be a sum of the following:

- Emissions attributed to production of the final good in the installation (direct + indirect), within ETS‑type system boundaries.

- Direct emissions: Emissions from production processes such as combustion, fuel consumption, etc.

- Indirect emissions: Emissions from electricity consumed in the production process.

- Embedded emissions in input materials or precursors. These include both direct and indirect emissions emitted during the production of precursors or input materials and thereafter, consumed in the production of final goods. Crucially, only precursors listed in Annexe I and Annexe VIII of the regulation (i.e., other CBAM goods) need to be counted. In practice, this implies accounting for emissions embedded in materials like steel, aluminium, and their pre-consumer scrap while producing items such as gearboxes, motors, or pumps.

VI. What’s Next? What should Indian producers do?

As CBAM is being proposed to be extended, Indian producers must take the following measures:

- Monitor, Report, and Verify: Indian producers must first identify whether their products are covered under CBAM. In case they are covered, Indian producers must establish robust installation-level emissions monitoring systems. Downstream industries should use 2026-2027 to adapt to CBAM and prepare themselves to be verified through CBAM-accredited verifiers.

- Map your supply chain and monitor suppliers' carbon emissions: Conduct detailed supply chain mapping to identify CBAM goods within your supply chain. Businesses must engage with their suppliers to ensure they receive the ‘actual’ emissions data, which would in turn help them comply with CBAM and lower their carbon footprint.

- Develop a CBAM compliance program: Start by mapping your product portfolio (using CN codes) against the downstream extension proposal. Next, design a comprehensive CBAM Compliance Program that clearly defines the roles and responsibilities of all stakeholders, covering legal, ESG, plant operations, and export teams. It should outline data flow processes, set robust document retention protocols, and ensure smooth coordination across departments.

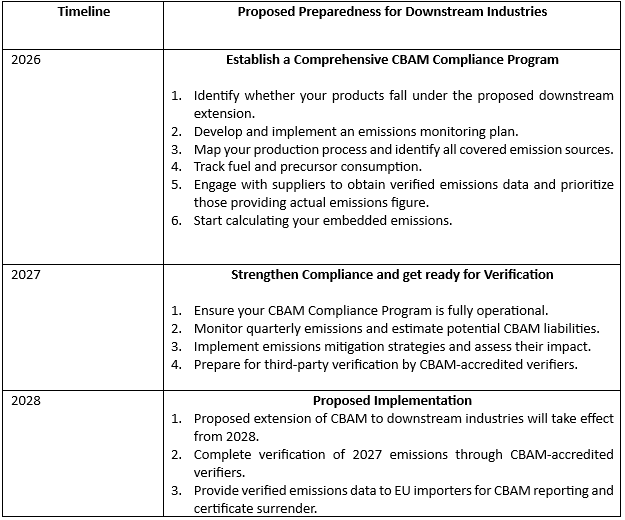

VII. Understanding CBAM Timelines for Existing Industries and Proposed for Downstream Industries:

The downstream extension of CBAM Goods is currently scheduled to take effect from 1 January 2028, making 2026–2027 critical years for exporters looking to safeguard their interests in the EU market. Businesses would be well advised to use this period strategically to establish robust monitoring, reporting, and verification (MRV) systems.

VIII. Conclusion

As indicated above, unlike the original CBAM goods and sectors connected thereto, there is no transition period for downstream products. Once the extension comes into effect, i.e., 1 January 2028, EU importers will face immediate financial obligations, including the purchase and surrender of CBAM certificates. Businesses that fail to implement effective MRV mechanisms risk severe consequences, i.e., loss of access to the EU market.

CBAM’s downstream expansion presents both a strategic opportunity and a compliance risk. Businesses that move early – by mapping covered products and inputs, strengthening emissions-data systems, and aligning contracts and supply chains – can protect and potentially expand EU market access while staying ahead of domestic and global competitors. Conversely, businesses that defer preparedness may find that commercial competitiveness alone is not enough: gaps in data, documentation, and governance can translate into delays, higher costs, or loss of EU market access. With the compliance burden set to intensify in the coming years, early adoption of CBAM readiness measures is increasingly becoming a baseline requirement for continuing to operate competitively in the EU.