Irish investment fund products can be constituted in various legal forms. A range of factors can influence the choice of legal vehicle, including tax treatment, risk spreading requirements, local market requirements and market preferences.

The structuring options include a Unit Trust, an Irish Collective Asset-management Vehicle (ICAV), a Variable Capital Company (VCC), an Investment Limited Partnership (ILP) and a Common Contractual Fund (CCF). This series takes a look at each of these options.

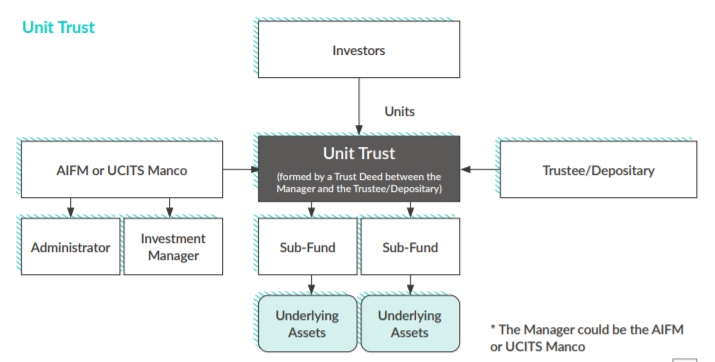

What is a unit trust?

A unit trust is defined by the Unit Trusts Act, 1990 (the principal legislation in relation to unit trusts in Ireland) as "any arrangement made for the purpose, or having the effect, of providing facilities for the participation by the public, as beneficiaries under a trust, in profits or income arising from the acquisition, holding, management or disposal of securities or any other property whatsoever".

How is a unit trust created?

A unit trust is created by a trust deed entered into between a trustee who is also the depositary

for UCITS/ AIFMD purposes (Depositary) and a management company.

How is a unit trust structured?

A unit trust is a contractual fund structure constituted by trust deed. A unit trust is not a separate legal entity and does not have legal personality. Because of this, a unit trust does not enter into contracts in its own name. The Depositary acts as legal owner of the unit trust's assets on behalf of the investors. Managerial responsibility rests with the board of directors of the management company. The management company enters into contracts with the administrator, investment manager and other service providers.

Regulatory regimes

A unit trust may be authorised as a UCITS (in which case they must be open-ended). UCITS are subject to the UCITS regime which includes the Central Bank of Ireland's UCITS Regulations.

A unit trust may be authorised as an Alternative Investment Fund (AIF) under the Unit Trusts Act 1990 in one of two categories:

- A Retail Investor AIF (RIAIF) which may be marketed to retail investors.

- A Qualifying Investor AIF (QIAIF) which may be marketed to Qualifying Investors.

Both RIAIFs and QIAIFs are subject to the AIFMD regime which includes the Central Bank of Ireland's AIF Rulebook.

Liquidity

Unit trusts may be open ended or, if authorised as RIAIFs or QIAIFs, may have limited liquidity or be closed-ended.

Umbrella/ Single fund/ Segregated Liability between sub-funds

Unit trusts may be single funds or umbrella funds. Umbrella unit trusts enjoy segregated liability between sub funds by operation of trust law and the trust deed.

What do investors hold?

Investors hold units which represent a beneficial interest in the assets of the unit trust.

Main advantages

- Routine changes can be made to the trust deed without having to obtain prior investor approval if both the management company and Depositary certify that such changes do not materially prejudice the interests of investors.

- Unit trusts are not required to hold annual investor meetings.

- In addition to the UCITS/ AIF regime, a unit trust is generally subject to Irish trust law.

- For RIAIFs and QIAIFs, a unit trust is not obliged to operate on the principle of risk spreading.

- Unit trusts are preferred in certain jurisdictions (such as Japan) where local regulators and investors are more familiar with a contractual investment structure.

Points to note

- Unit trusts must have a management company.

- Broadly, a regulated fund constituted as a unit trust is exempt from tax on its income and gains on underlying investments and instead operates an exit tax on certain chargeable events (e.g. distributions to, or disposals of units by, its non-exempt Irish resident investors). Non-Irish tax resident investors and Irish exempt resident investors are outside the scope of the exit tax regime. To the extent the unit trust, or a sub-fund of an umbrella unit trust, is invested 25% or more in Irish real estate, consideration needs to be given to the potential application of IREF withholding tax and exemptions therefrom.