I. Introduction

Revenue is a key component of all businesses, including franchisors, and it is important that counsel to franchisors have an understanding of the potential effects that accounting changes relating to revenue recognition can have on a franchisor. An important change in the rules related to revenue recognition became effective in 2019 and 2020 due to the adoption of Accounting Standards Codification, “Revenue from Contracts with Customers” (Topic 606)[1] (ASC 606) by the Financial Accounting Standards Board[2] (the FASB) on May 28, 2014.[3]

For many businesses, the impact of ASC 606 has been minimal, however, for the franchising industry, the impact of the new rules are sweeping. Before ASC 606, franchisors were generally allowed to recognize initial franchise fees as revenue when a franchise opened for business under ASC 952-605.[4] In contrast, ASC 606 results in the allocation of the initial franchise fee on a straight-line basis over the term of the franchise agreement unless the franchisor demonstrates that certain pre-opening services comprise a “distinct” deliverable.[5] For most franchisors, the new standard causes some portion of the initial franchise fee to appear as a contract liability (deferred revenue) on the balance sheet, as opposed to revenue on the income statement.

ASC 606 has largely been met with confusion and concern by the franchise industry. In particular, the franchise industry has raised concerns about the varying interpretations of timing of revenue recognition under ASC 606 for initial franchise fees, and the costs of implementing ASC 606.[6] In addition, although the underlying cash flows and operations of a business are unchanged, ASC 606 could negatively impact financials and may have a considerable effect on key valuation inputs, such as EBITDA. The deferred recognition of initial franchise fee revenue could ultimately hinder growth in the franchise segment and potentially result in business closures and job losses.[7]

On April 8, 2020, in response to these concerns and citing the coronavirus pandemic, the FASB announced the delayed implementation of ASC 606 for franchisors that are not public entities.[8] On July 22, 2020, the FASB stated that it intends to add a project to its technical agenda to provide franchisors with a practical expedient for the recognition of initial franchise fees that is designed to reduce the implementation costs related to applying ASC 606 to initial franchise fees, and will accept public comment on an alternative standard for private sector franchisors.[9]

Part II of this article provides a detailed explanation of revenue recognition rules for three major types of revenue streams for franchisors, including initial franchise fees, royalties and advertising fund contributions, both before and after the implementation of ASC 606. Specific examples illustrating the impact of ASC 606 on a franchisor’s balance sheet, income statement and cash flows statement and common valuations are provided in Part III. In addition, Part IV provides an overview of the impact of ASC 606 on the franchising industry, including a discussion of the benefits and disadvantages associated with ASC 606 according to CPAs, CFOs and other franchisor executives. Finally, Part V discusses additional changes to the revenue guidance for franchisors that are likely on the horizon.

II. REVENUE RECOGNITION RULES FOR FRANCHISORS BEFORE AND AFTER THE ADOPTION OF ASC 606

A. Before ASC 606

1. General Revenue Recognition Rules Under ASC 605

The FASB’s former rules associated with revenue recognition are included within Revenue Recognition (Topic 605) (ASC 605).[10] ASC 605 provided that to recognize revenue, revenue must be both “realized” (or “realizable”) and “earned”.

(a) Realized/Realizable Revenue. Revenue is “realized” when products (goods or services), merchandise, or other assets are exchanged for cash (or a claim to cash). Revenue is “realizable” when related assets received or held are readily convertible to known amounts of cash (or a claim to cash).[11]

(b) Earned Revenue. Revenue is “earned” when the entity has substantially accomplished what it must do (i.e., the entity’s “revenue-generating activities”) to be entitled to the benefits represented by the revenues. An entity’s “revenue-earning activities” include delivering or producing goods, rendering services, or other activities that constitute its ongoing major or central operations.[12]

2. Franchisor-Specific Guidance Under ASC 952-605

In addition to ASC 605, the FASB provided industry-specific guidance for certain types of franchisor-specific revenue under ASC 952-605. Among other areas, ASC 952-605 specifically addressed revenue recognition associated with initial franchise fees, royalties, and advertising fees.[13]

(a) Initial Franchise Fees. ASC 952-605-25 permitted the recognition of initial franchise fees when all material services or conditions relating to the sale were “substantially performed.”[14] Substantial performance by a franchisor was deemed to have occurred when the franchisor had no remaining obligation or intent—by agreement, trade practice, or law—to refund any cash received or forgive any unpaid notes or receivables, and substantially all of the initial services of the franchisor required by the franchise agreement had been performed. ASC 952-605-25-2 added that the commencement of operations by the franchisee was presumed to be the earliest point at which substantial performance has occurred, unless it was demonstrated that substantial performance of all obligations, including services rendered voluntarily, had occurred before that time.[15]

In short, once a franchisee “opened its doors” or otherwise began operations, the franchisor had met substantial performance requirements and could, therefore, recognize initial franchise fees as revenue.[16] The guidance under 952-605 provided a simple and clear method to determine revenue recognition related to initial franchise fees.

(b) Continuing Franchise Fees. The Accounting Standards Codification defines “continuing franchise fees” as “[c]onsideration for the continuing rights granted by the franchise agreement and for general or specific services during its life.”[17] The FASB provided that continuing franchise fees must be reported as revenue as the fees were earned and became receivable from the franchisee under ASC 952-605-25-12.[18] It is generally accepted that royalties and advertising fees meet the definition of “continuing franchise fees.”

Under this guidance, some franchisors recognized these royalties on a “lag basis.” This means they recognized royalties as revenue in the period subsequent to when the sales occur at the franchisee level. The reason for this is due to the lack of available information at the end of the reporting period. Other franchisors recognize the revenue associated with the royalties in the month in which the sales occur at the franchisee level.

ASC 952-605-25-13 provided an important caveat for fees required to be segregated and used for a specified purpose that often applied to determine revenue recognition for advertising fund contributions. The recognition of advertising fund contributions largely turned on whether the franchisor was merely arranging the activities to occur (i.e., the franchisor was acting as an “agent” with respect to the fund), or was itself conducting the activities (i.e., the franchisor was acting as a “principal” with respect to the fund). Under this guidance, if the franchisor was acting as an agent, advertising fund contributions were recorded as a liability against which the specified costs were charged. If there was a surplus of fees collected for purposes of an advertising fund, then the franchisor was required to carry that surplus as a liability on its balance sheet. In addition, if expenditures from the fund were in excess of advertising fund contributions collected, this was reflected as advertising expense in the income statement of the franchisor. If, however, the franchisor was acting as a principal and itself conducting the advertising activities, revenues were recognized once the funds were earned and receivable, similar to royalties.[19]

B. Revenue Recognition After ASC 606

1. General

ASC 606 broadly impacts all businesses that enter into contracts with customers to transfer goods or services and replaces hundreds of industry-specific revenue recognition rules with single comprehensive “principle-based” framework.[20] ASC 606 was the result of a joint project of the FASB and the International Accounting Standards Board to clarify principles of revenue recognition and develop a common revenue standard, and arose from a concern that the industry-specific U.S. rules resulted in varying recognition for economically similar transactions making comparisons across industries (and internationally) difficult.[21] The goal in developing new revenue recognition rules was to establish a principle-based revenue recognition model that would apply across different industries that would improve consistency in financial reporting.[22]

The FASB stated that the new guidance:

- Removes inconsistencies and weaknesses in existing revenue requirements.

- Provides a more robust framework for addressing revenue issues.

- Improves comparability of revenue recognition practices across entities, industries, jurisdictions, and capital markets.

- Provides more useful information to users of financial statements through improved disclosure requirements.

- Simplifies the preparation of financial statements by reducing the number of requirements to which an organization must refer. [23]

ASC 606-10-65-1d provides transition requirements that allow either full retrospective application of all periods presented in the financial statements or a modified retrospective application where on the date of implementation, there is a cumulative effect of implementation reflected in the financial statements.[24]

The underlying premise of ASC 606 is to “recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.”[25] ASC 606-10-05-4 provides a five-step process for applying this principle to revenue received under customer contracts:

Step 1: Identify the contract(s) with a customer

A contract is an agreement between two or more parties that creates enforceable rights and obligations. The guidance in [ASC 606] applies to each contract that has been agreed upon with a customer and meets specified criteria. In some cases, [ASC 606] requires an entity to combine contracts and account for them as one contract. [ASC 606] also provides requirements for the accounting for contract modifications.

Step 2: Identify the performance obligations in the contract

A contract includes promises to transfer goods or services to a customer. If those goods or services are distinct, the promises are performance obligations and are accounted for separately. A good or service is distinct if the customer can benefit from the good or service on its own or together with other resources that are readily available to the customer and the entity’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract.

Step 3: Determine the transaction price

The transaction price is the amount of consideration in a contract to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer. The transaction price can be a fixed amount of customer consideration, but it may sometimes include variable consideration or consideration in a form other than cash. The transaction price also is adjusted for the effects of the time value of money if the contract includes a significant financing component and for any consideration payable to the customer. If the consideration is variable, an entity estimates the amount of consideration to which it will be entitled in exchange for the promised goods or services. The estimated amount of variable consideration will be included in the transaction price only to the extent that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.

Step 4: Allocate the transaction price to the performance obligations in the contract

An entity typically allocates the transaction price to each performance obligation on the basis of the relative standalone selling prices of each distinct good or service promised in the contract. If a standalone selling price is not observable, an entity estimates it. Sometimes, the transaction price includes a discount or a variable amount of consideration that relates entirely to a part of the contract. The requirements specify when an entity allocates the discount or variable consideration to one or more, but not all, performance obligations (or distinct goods or services) in the contract.

Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation

An entity recognizes revenue when (or as) it satisfies a performance obligation by transferring a promised good or service to a customer (which is when the customer obtains control of that good or service). The amount of revenue recognized is the amount allocated to the satisfied performance obligation. A performance obligation may be satisfied at a point in time (typically for promises to transfer goods to a customer) or over time (typically for promises to transfer services to a customer). For performance obligations satisfied over time, an entity recognizes revenue over time by selecting an appropriate method for measuring the entity’s progress toward complete satisfaction of that performance obligation.[26]

2. ASC 606’s Application to Franchisor Revenue

First, and foremost, ASC 606 requires that a franchisor identify its major revenue streams. These revenue streams are identified based on review of the franchise agreement which is the contract governing business between the franchisor and franchisee. Although this list is not all-inclusive and revenue streams will vary among franchisors, the most common significant revenue streams for franchisors are initial franchise fees, royalties and advertising fees. The application of ASC 606 for each of these franchisor-specific revenue streams is described below.

(a) Initial Franchise Fee Revenue. For revenues associated with initial franchise fees:

Step 1 – Identifying the Contract: The contract utilized in assessing the revenue recognition process will be the franchise agreement. The franchise agreement provides the background information about the responsibilities of the franchisor and franchisee that is necessary to move forward with Steps 2 through 5.

Step 2 – Identifying the performance obligations in the contract: Step 2 requires significant analysis, and it is best practice to conduct interviews with executives involved with management and other department heads within the franchisor to properly identify the goods and services that are delivered to the franchisee under the franchise agreement. Generally speaking, however, the performance obligation in a franchise agreement is primarily the franchise right which transfers over time and, therefore, revenue from the initial franchise fee must be recognized over the life of the contract. But if any of the initial services that it provides to the franchisee are sufficiently “distinct” from the franchise right, they may be deemed separate performance obligations under ASC 606. If so, then a franchisor may be able to recognize a portion of the initial fee attributable to those services when those services are performed for, or, in the case of goods, when those goods are provided to the franchisee.

Under ASC 606-10-25-19, a good or service that is promised to a customer is “distinct” if both of the following criteria are met:

(1) The customer can benefit from the good or service either on its own or together with other resources that are readily available to the customer (that is, the good or service is capable of being distinct); and

(2) The entity’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract (that is, the promise to transfer the good or service is distinct within the context of the contract).[27]

As noted above, typically, the primary obligation under a franchise agreement is the grant of the license to use the franchisor’s intellectual property. Other common performance obligations include training, market research and site selection and the sale of equipment. Each of these performance obligations are analyzed below.

- Training. A franchisor must determine whether there are specific portions of the training that are distinct from the franchise right, and from which the franchisee can benefit from in a general business context. Franchisors typically provide business training on operational and administrative matters, in addition to training on proprietary and brand-specific aspects of the system. Generalized training on topics such as accounting, recordkeeping, banking, payroll, and purchasing procedures may be performance obligations which can be considered separate from the franchise. Training on brand standards and franchisor-specific operating processes are unlikely to be considered a distinct performance obligation. Training on customized computer technology and food preparation methods, for example, are probably not distinct, and, therefore, the value of the training (under Step 3) would be combined with the value of the intellectual property license granted to the franchisee for the purpose of recognizing revenue under ASC 606.

- Market Research and Site Selection. Site selection services might include market analysis and the review and assistance in the negotiation of a lease. These services are valuable services to many business owners, and a franchisor may conclude that these services are not specific to the brand. If so, under ASC 606, the transaction price (under Step 3) can be recognized when the site selection services are completed.

- Equipment. The franchisor’s promise to provide start-up equipment is a performance obligation that is identifiable from other promises in the contract. If the equipment is able to be used in other businesses, a franchisor may reasonably conclude that the equipment is another performance obligation that is distinct from the franchise right. If the nature of the equipment is specific to the franchisor (e.g., signage, menu boards or other branded or proprietary items) such that the franchisee cannot benefit from the equipment on its own, then the equipment value would be combined with the value of the intellectual property license granted to the franchisee for the purpose of recognizing revenue.

Step 3 – Determining the transaction price: Transaction price will vary based on the pricing structure of the franchise. In many cases, it is a flat fee, in others it will vary based on territory in which the franchisee will service its customers. This will be specifically identified within the franchise agreement.

Step 4 – Allocate the transaction price: Management is responsible for assigning values associated with the performance obligations of the franchisor based on the relative fair values of those performance obligations. In many cases, this involves a complicated analysis depending upon the sophistication of the franchisor and market data that is available to the franchisor. Determining some values will be more straight-forward than others. In order to determine values for the performance obligations noted above, a franchisor might take the following steps:

- Training − If the franchisor charges a standard rate for subsequent training of franchisees within their franchise agreement, it will use that same rate to determine the value of the training provided. If there is not a predetermined value, then the franchisor may need to do market research to assess the value associated with the training. Some franchisors look at the costs charged by local colleges for educating students to determine an average hourly value for training costs. Others may look at the cost of specialized seminars covering similar topics.

- Market Research and Site Selection – A good resource for this information might be local consultants that perform similar services to determine hourly rates, fees, etc. This will help the franchisor in determining the price associated with performing the service for the franchisee.

- Equipment costs – The value of the equipment would be the cost of the equipment to the franchisor, plus a reasonable mark-up.

Step 5 – Recognize revenue when (or as) the entity satisfies a performance obligation: Following the allocation of the transaction price, the franchisor will recognize the revenue as it fulfills its obligations. If the values assigned to the distinct performance obligations included within the initial franchise fee exceeds the value of the initial franchise fee itself, then the franchisor will recognize 100 percent of that initial franchise fee upon fulfilling the performance obligations. If the values assigned to the distinct performance obligations included within the initial franchise fees are less than the value of the initial franchise fee, the remaining amount of revenues is recognized ratably over the life of the franchise agreement.

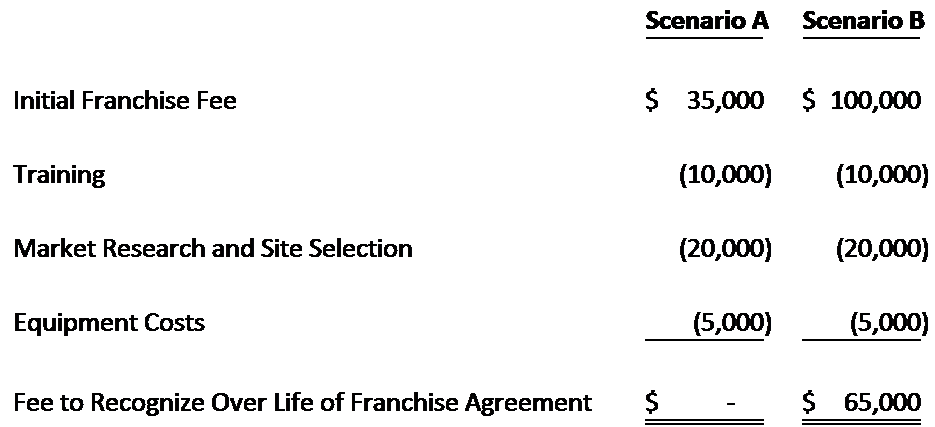

For the performance obligations identified above, let’s consider the two scenarios:

In Scenario A, the franchisor is in a situation where the value of the performance obligations equal the value of the initial franchise fee charged. Accordingly, there is no fee to recognize over the life of the franchise agreement.

In Scenario B, the initial franchise fees are less than the value of the performance obligations of the franchise agreement. In Scenario B, if we were to assume that all performance obligations were fulfilled by the franchisor on the last day of its fiscal year end, the franchisor would recognize $35,000 for the training, market research and site selection and equipment costs and the remaining $65,000 would remain on the balance sheet as a contract liability (deferred revenue) and recognized ratably over the life of the franchise agreement.

As mentioned previously, financial statement preparers are required to retrospectively apply this guidance to all contracts that are in place on the date of implementation. Accordingly, financial statement preparers must analyze the cumulative impact of this change with respect contracts that can be many years old, depending on how long the franchise system has been operating. This can result in a significant reduction in equity to create a contract liability to defer revenues that were previously recognized. This is another reason that this new revenue recognition model creates a new dynamic in financial reporting for franchisors. The impact of these changes on franchisors’ financial statements will be later discussed in greater detail.

(b) Royalties. When analyzing sales-based royalties and applying the five-steps above, the governing contract is the same as that for the initial franchise fee—the franchise agreement (Step 1). The performance obligation associated with the franchise agreement is the license conveyed to operate a franchise business (Step 2). In order to complete Steps 3 to 5 under ASC 606, the financial statement preparer must determine the amount of royalties that would be received over the term of the franchise agreement without a significant reversal.[28] Although royalty revenue recognition under ASC 606 is similar to ASC 605, one of the major changes under ASC 606 is that recording royalty revenues on a lag basis is no longer permitted. The variable nature of sales-based royalties resulted in in special guidance for sales-based royalties under ASC 606. ASC 606-10 states that an entity should recognize revenue for sales-based royalties at the later of (i) the subsequent sale, or (ii) the satisfaction of the performance obligation to which some or all of the sales-based royalty has been allocated.[29] The new guidelines require financial statement preparers to determine an estimate of royalties earned during the accounting period if enough information is not available.

(c) Advertising fees. Revenues from advertising fund contributions are treated very differently under the new revenue recognition rules. In general, under ASC 606, advertising fund contributions are recognized following the same approach as sales-based royalties.[30]

As described above, under ASC 605, advertising fund contributions were recorded as a liability against which the specified costs were charged assuming the relationship between the franchisor and the advertising fund was an agency relationship. Under ASC 606, however, a franchisor may record advertising fund contributions as revenue. In addition, under the former rule, where an agency relationship existed, the franchisor was required to record any surplus from year to year as a deferred revenue. However, under ASC 606, any surplus will be recognized as revenue. In this way, the new guidance potentially causes the advertising fund to become a source of profit for a franchisor despite it is contractually obligated to use the fund for the benefit of the franchise system.

3. Capitalization of Certain Costs to Obtain a Contract

In addition to analyzing the revenues associated with contracts with customers, another important change related to ASC 606 is the addition of subtopic ASC 340-40, which introduces changes relating to capitalization of certain costs of obtaining a contract with a customer.[31] Under this guidance, franchisors can identify costs that can be specifically tied to its contracts and capitalize those costs to be amortized over the life of the franchise agreement.[32] The analysis provided under ASC 340 may partially offset the impact of the revenues that must be deferred under ASC 606.

As noted within the guidance, sales commissions and broker fees that relate directly to the sale of a specific franchise can be capitalized and amortized over the period in which the costs are expected to be recovered.[33] For franchisors, this means that these costs may be amortized over the term of the franchise agreement.

As previously mentioned, the recognition of the contract asset (deferred costs) results in an offsetting impact to the equity of a franchisor once they have deferred revenues associated with contracts with customers. However, under ASC 340-40, a franchisor can only defer costs incurred on a contract to the extent they have the associated deferred revenues. This means that franchisor cannot defer costs that are in excess of the revenues deferred and inflate their equity position as a result of applying the guidance under ASC 340-40.[34]

III. The Impact of ASC 606 on Franchisor Financial Statements and Valuations

A. Example of ASC 606’s Impact on a Franchisor’s Balance Sheet, Income Statement, and Cash Flows Statement

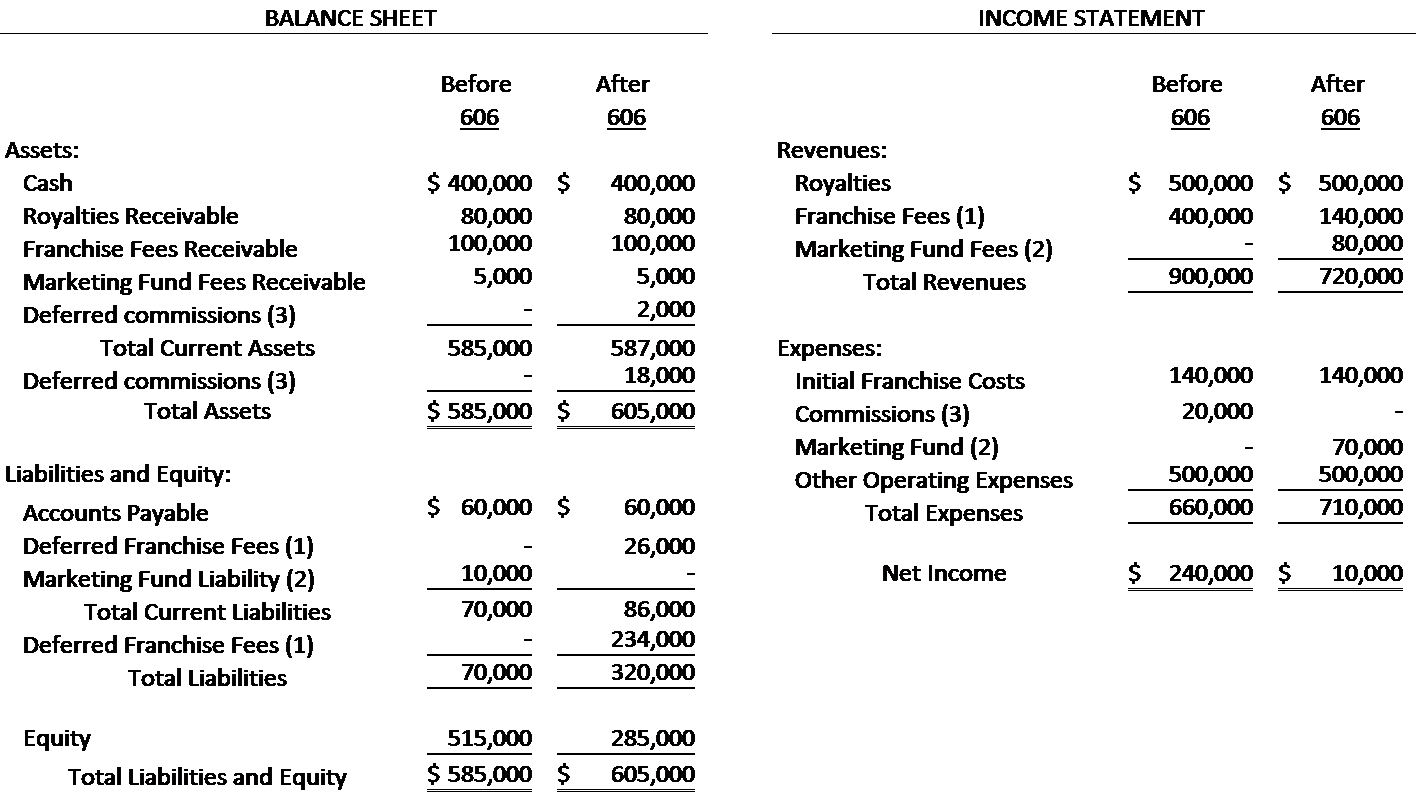

A franchisor’s balance sheet, income statement and cash flows statement are routinely analyzed by financial institutions, investors, state regulators and other readers of financial statements interested in determining the financial strength and profitability of a franchisor. Below is an example based on the franchisor described in Scenario B above that has been prepared to illustrate the impact of ASC 606 on these financial statements.

For this example, we’ll assume the franchisor from Scenario B sold four franchises with an initial franchise fee of $100,000 (4 × $100,000 = $400,000) during the year, fulfilled all obligations related to training, market research, site selection, incurred equipment costs with standalone selling prices totaling $35,000 (4 × $35,000 = $140,000) by the last day of the franchisor’s fiscal year, and paid a broker fee on each sale of $5,000 (4 × $5,000 = $20,000). Each franchise agreement has a ten-year term and, for simplicity, performance obligations are considered fulfilled on the last day of the entity’s fiscal year.

We’ll also assume the entity collects a percentage of franchisees’ sales as an advertising fund contribution as required by the franchise agreement.

Below is the balance sheet and income statement of the franchisor from Scenario B, reflecting the impact of the above assumptions both before ASC 606 and after ASC 606.

As noted above, the effect of adopting ASC 606 resulted in a decrease in total net income of $230,000. The driving factors of this change are (1) the deferral of a portion of the initial franchise fee that will be recognized over the franchise agreement term which decreased revenues by $260,000, (2) the required recognition of all advertising fees and expenditures resulting in a net increase of $10,000 to net income, and (3) the deferral of commission expenses which will be recognized over the franchise agreement term which decreased expenses by $20,000.

From a balance sheet perspective, total assets have increased by $20,000 as a direct result of the deferral of commissions expense. Liabilities have increased by a net amount of $250,000 due to (1) the recording of deferred franchise fees of $260,000, and (2) the elimination of the previously recorded advertising fund agency liability of $10,000 as all advertising fund activity is now required to be presented as part of normal operations.

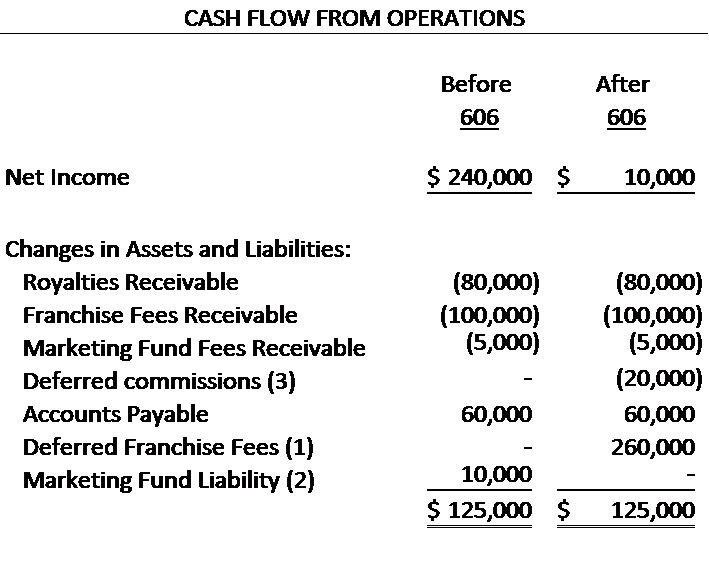

However, ASC 606 can have a significant impact on the results of operations and assets and liabilities of an entity, as noted below, this standard has no bearing on an entity’s ultimate cash flow, as illustrated in the excerpt from the statement of cash flows based on the Scenario B.

Based on this example, the negative consequences of ASC 606 are apparent. Under ASC 606, a franchisor’s total net income may decrease while liabilities increase. However, here, ASC 606 has no impact on cash flow. Therefore, under ASC 606, assessing cashflows from operations becomes an even more important benchmark to determining the financial strength and profitability of a franchisor, particularly with respect to newer systems. Franchise companies with strong growth in cash flow from operations most likely have more stable net income, and more opportunities to expand and weather downturns in the general economy or their industry.

B. Example of ASC 606’s Impact on Valuations

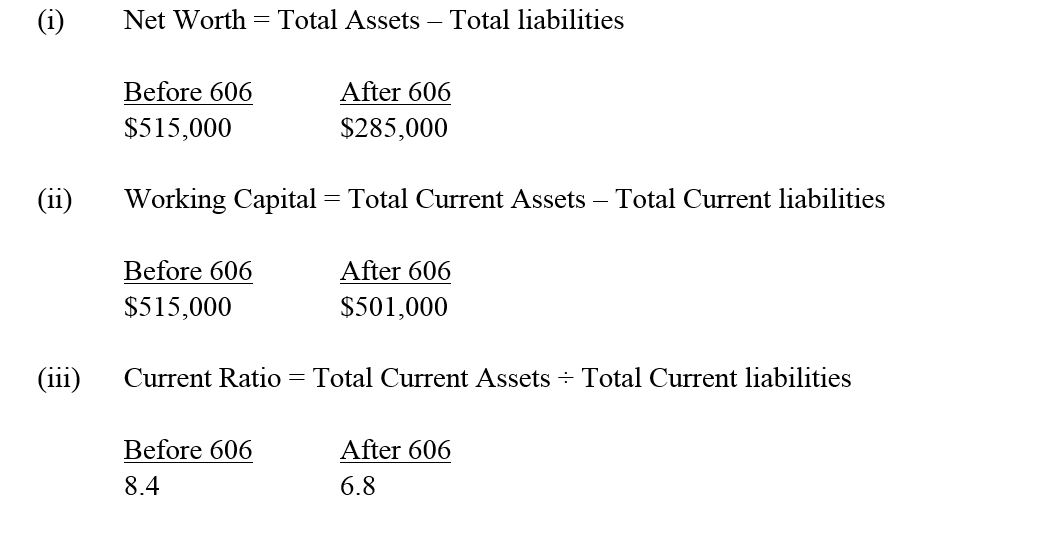

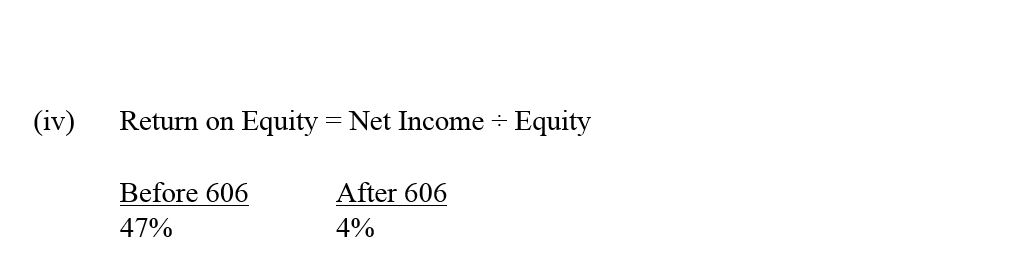

Common ratios analyzed by readers of financial statements include the following, shown before and after the adoption of ASC 606, using the previous example.

As the most substantial impact of ASC 606 is the deferral of a portion of initial fees over the franchise term creating a long-term liability, there were no drastic changes to the example entity’s current assets or current liabilities as noted with minimal deviations in the entity’s working capital and current ratios. However, the deferral of the initial franchise fees and related commissions resulted in a decrease in net income of approximately ninety-six percent and increased total liabilities of approximately 357 percent, thus significantly reducing total net worth and overall return on equity.

Another calculation commonly used by state regulators looks at ensuring the total cash and cash equivalents exceed the sum of:

- Current liabilities

- Cost to establish a franchisee times the number of projected opening during the coming fiscal year

- Cost to establish a franchisee times the number of franchisees signed but not yet open as of fiscal year end

For purposes of calculating this measure, readers of the financial statements must remove the current portion of deferred revenues calculated under ASC 606 from current liabilities. Conceptually, deferred revenues are not a liability that requires a cash outflow, as much as it is the obligation to perform services to a franchisee. This obligation is already considered, in part, with the calculation above of cost to establish a franchisee times the number of franchisees signed but not yet open as of fiscal year end.

The example above illustrates the impact to a franchisor that is relatively new. In the event the franchisor has revenues that have been recognized in previous years that are required to be deferred due to retrospective application of ASC 606, this could further reduce net worth and current ratio for the franchisor and impact the amount of the deferred revenue liability on the balance sheet.

Unfortunately, financial institutions, investors, state regulators and other readers of financial statements may not currently have a thorough understanding of how ASC 606 impacts valuation. As noted, the change in accounting standards has no impact on an entity’s cash flow from operations which represents an entity’s ability to generate cash from its core business activities and is an indicator of operational efficiency. The expression “cash is king” becomes especially true when evaluating a franchisor’s financial position under ASC 606. Regulators and other readers of financial statements should place more importance on liquidity-based ratios and measures, with consideration for how ASC 606 has impacted the inputs.

IV. The Practical Impact of ASC 606 on the Franchising Industry

As noted previously, the FASB delayed the required implementation of ASU 606 for private company franchisors in April 2020. Because a majority of franchisors had already completed their audited financials for 2019, we had the opportunity to interview several individuals including CPAs, CFOs and executives of franchise companies regarding the benefits and disadvantages of ASC 606, and gain insights into obstacles encountered by franchisors in implementing the new standard.

Most of the franchise executives we spoke with did not find that ASC 606 had a significant impact on their companies’ financial results, although in systems where there had been a significant number of new franchise sales, there was some impact.[35] Some expressed concern that the application of ASC 606 could have serious negative consequences for new franchisors that have not reached royalty self-sufficiency. Under ASC 606, a franchisor might change from being a "profitable" and growing franchisor to being an "unprofitable" but growing franchisor after application of ASC 606.[36]

A primary concern of CFOs and franchise executives involved the complexities and burdens associated with implementing ASC 606.[37] Most agreed that the implementation of ASC 606 significantly increased the workload of the franchisor’s accounting team and outside auditors. Franchise agreements had to be carefully reviewed and analyzed. The accounting staff built schedules to monitor and track revenues for the identified performance obligations over the life of the franchise agreement. In addition, past contracts were reviewed and revenue under those contracts that was previously recognized was reamortized. A few executives cautioned that engaging competent accounting personnel and auditor’s with experience with the preparation of financial statements for franchisors was paramount under ASC 606. They cautioned that the new rules involved a new and very complex accounting language that required translation by those with significant expertise in this area.[38]

One CFO commented that he believed that ASC 606 will result in the need to prepare and maintain two sets of books and accounting records. His company’s lender had insisted that the franchisors continue provide financials that are consistent with the way it had historically viewed the business. Going forward, he predicted that many franchisors will have “bank financial statements,” which show the franchisor’s financial position without application of ASC 606, and the “GAAP financial statements” that are prepared to be in compliance with ASC 606.[39]

Another CFO commented that he saw tremendous value in going through the exercise of determining all of the various performance obligations and assessing the franchisor’s direct costs of fulfilling its franchisor’s performance obligations. He believed that the analysis assisted the franchisor in understanding its true costs involved in assisting a franchise outlet to open, and could be helpful to justify the amount of the initial franchise fee to future prospective franchisees. However, he was strongly opposed to the treatment of advertising fees under the new rules. He explained that ASC 606 might result in a gross misstatement of a franchisor’s revenue position with respect to the advertising fund revenue, and potentially its profit position. Further, the ability to count an end-of-year surplus in the advertising fund in profit could result in franchisors spending less of the advertising fund to enhance profits, when the reality is that the franchisor has a contractual obligation to spend the advertising funds on behalf of the franchisees.[40]

V. What Further Changes and Provisions Are on the Horizon Associated with ASC 606 and the Franchising Industry?

Implementation of ASC 606 provides challenges for franchisors, both large and small. While attempting to implement in 2020, many franchisors were faced with the additional challenges associated with the coronavirus pandemic. In response, the FASB released ASU 2020-05 which deferred the effective date of ASC 606, specifically for franchisors, for an additional year. As a result, franchisors who have not already issued financial statements in accordance with ASC 606 are now required to implement ASC 606 for annual reporting periods beginning after December 15, 2019 (i.e., calendar year 2020).[41]

Another reason for this delayed effective date is that franchising lobbyists and other members of the franchising community have voiced their concerns regarding the cost and complexity of implementing ASC 606. The FASB met on July 22, 2020 to discuss a project to reduce the cost and complexity of implementing ASC 606. The tentative board decisions are as follows:

1. Add a project to its technical agenda to reduce the implementation costs related to applying ASC 606 to initial franchise fees for franchisors that are not public business entities. A franchisor that is not a public business entity may elect the practical expedient to account for initial services as a single performance obligation if:

(a) Those services are the same as those included in a pre-defined list of services.

(b) It is probable that the continuing fee will cover the cost of the continuing services provided by the franchisor with a reasonable profit.

2. Include the practical expedient for applying ASC 606 to initial franchise fees for franchisors that are not public business entities within Topic 952, Franchisors.

3. Require an entity that elects the practical expedient to disclose that fact.[42]

The intent of these tentative decisions is to ease the impact of implementation of ASC 606 by taking opening services included in the predetermined list (such as training, site selection, equipment purchases, etc.) and bundling it as one performance obligation to track as opposed to tracking each one individually. Preparers will still have to determine a standalone selling price for the value of that bundled obligation, but it is the FASB’s intention to ease the tracking process of fulfillment and recognition of the value of those performance obligations.[43]

The FASB issued an exposure draft in the September 2020 which includes full text regarding how this expedient is expected to be applied and how it will benefit franchisors. The FASB is providing a comment period of 45 days through November 5, 2020. Financial statement preparers, stakeholders and other readers of financial statements for franchisors are encouraged to review and provide a response on this expedient to assist the FASB in providing relief to the franchising community.[44]

If a franchisor chooses to apply this practical expedient, they will be allowed to apply it as part of implementation of ASC 606. If a franchisor has already implemented ASC 606, they will be allowed to do a full retrospective application of this expedient going back to the franchisor’s first reporting under ASC 606.[45]

VI. CONCLUSION

Since the release of ASU 2020-05 in April 2020, delaying the effective date of ASC 606 for non-public franchisors, the franchise industry has been hopeful that the FASB would adopt new guidance that would fundamentally change how the new revenue recognition rules apply to franchisor revenue. Some have speculated that the delayed effective date meant that the FASB had recognized the shortcomings of ASC 606 in the context of franchising, and that it would adopt industry-specific revenue recognition rules for the franchise industry similar to the former rules. However, the July 22, 2020 FASB meeting made it clear that the FASB is not abandoning its goal of providing a single comprehensive principle-based framework for revenue recognition. Although the FASB may attempt to simplify the process for revenue recognition under the practical expedient described in Part V, it is unlikely to implement substantive changes to the revenue recognition rules for franchisors. As a result, it appears that franchise industry and financial institutions, investors, state regulators and other readers of financial statements will need to adapt to ASC 606. Understanding ASC 606 and its impact on the financials and the valuation of franchise companies is a good first step.