Headwinds are blowing in capital markets globally. IPO and other equity capital markets (ECM) deal volumes are down more than 70%. As capital becomes harder to access, we explore the issues that are challenging markets and businesses. What can issuers do to put themselves in the best position to raise money or see themselves through until conditions improve?

Key takeouts

- Volatile macroeconomic conditions have caused equity capital markets to cool. Growth stocks have been hit hardest. The markets are looking for these companies to conserve cash, manage the impact of inflation and remain (or become) profitable.

- Capital raisings remain possible. For distressed companies, existing shareholders may participate in raisings to protect their investment. Raisings to fund accretive M&A continue to garner shareholder support. Companies can look to private markets for funds and dual track IPOs can provide pricing tension.

- Falls in activity are overstated as 2021 was a record year. Sentiment can change quickly (as it did after the initial COVID-19 downturn). It will be important to ensure that regulatory settings in Australia remain supportive of capital raisings.

Equity capital markets are facing a time of volatility and uncertainty. As Australian companies rebuild from COVID-19, some are seeking to raise capital to mitigate the impact of current conditions. Others may wish to acquire assets or finance new operations to continue a trajectory of growth. Yet all these ambitions are currently constrained by the broader macroeconomic environment and capital markets conditions.

Many factors are causing uncertainty and hampering the activity of equity capital markets. Chief among these are higher inflation and the reaction from central banks to tighten monetary policy. The war in Ukraine has disrupted global supply chains and energy supplies, just as many companies transition to renewable energy and increase their focus on environmental, social and corporate governance (ESG) outcomes. As rising interest rates prompt recession fears in the United States (US) and potentially Australia, these pressures are impacting on company valuations and institutional investor support.

In June 2022, MinterEllison Capital Markets partners Daniel Scotti, James Hutton and Nicole Sloggett assembled a group of seasoned capital markets experts for an inaugural Capital Markets Roundtable in Sydney. The session discussed trends and the outlook ahead. The group comprised (in alphabetical order):

- Blair Beaton, Acting Group Executive Listings and CSO, ASX

- Anthony Brown, CEO, NobleOak Life

- Stuart Dettman, Managing Director, Rothschild & Co

- Amelia Hill, Managing Director, MA Moelis

- Bing Jiang, Partner, Next Capital

- Calvin Kwok, General Counsel, Pinnacle Investment Management

- Will Lawrence, Director, Wilsons

- Andrew Lockhart, Managing Director, Metrics Credit Partners

- Michael Ryan, Managing Director, Brookfield Asset Management

- Greg West, Non-Executive Director, IDP Education

Speakers expressed longer-term confidence in the Australian market’s distinctive ability to rebound, even as the pipeline of initial public offerings (IPOs) dries up and secondary capital raisings are limited. The roundtable participants noted that while fundraising had become more difficult, it was a reflection of the cyclicality of markets and prevailing macroeconomic conditions. In fact, investor support for recent raisings indicates that quality businesses will continue to raise funds. This bodes well for a broad-based recovery once sentiments turns. Other reasons for optimism include a broadly benign regulatory environment and the need for superannuation funds to invest their ever-increasing capital base. (Super funds' assets are expected to triple to more than $9 trillion by 2041, according to Deloitte’s Dynamics of the Australian Superannuation System report).

The impact of volatility

Partner Daniel Scotti began the session, noting that the day’s conversation was occurring amidst a significant decline in equity capital market activity worldwide.

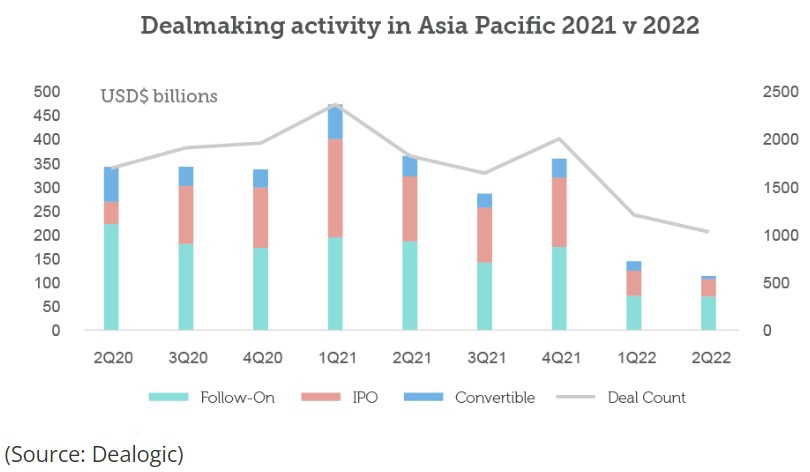

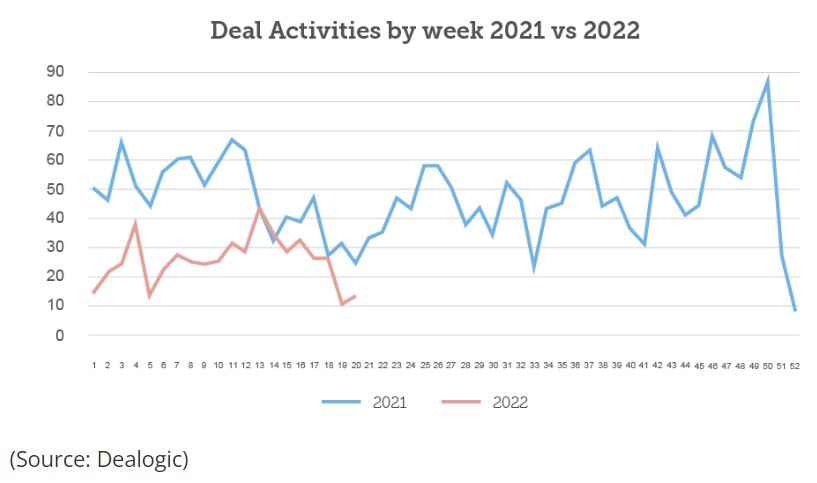

The US$115 billion worth of global equity capital market issuance in the second quarter of 2022 was the worst quarterly tally in more than a decade, according to Dealogic. Global IPO issuance fell 73% compared to the same period last year, with US deal value down 92%, Europe down 92% and the Asia-Pacific region down 80%.

Investors have also retreated, causing steep falls in the S&P/ASX 200 in Australia and US S&P 500 since last year’s peaks.

Contributing to the extent of these declines is the fact that 2021 was a record year for IPOs, with almost 2,400 deals raising more than US$450 billion globally. Some hangover was always inevitable, notwithstanding economic and geopolitical developments.

Speakers agreed that surviving current macroeconomic uncertainties was the key to improving investor sentiment for IPOs. This is particularly important as central banks in advanced economies from Australia to the US aggressively raise interest rates to combat inflation.

As Rothschild & Co’s Stuart Dettman observed, the resultant market volatility “isn’t the friend of capital markets” and directly correlates with a reduction in IPO activity. Investors were waiting to see how these central bank interventions might impact economic growth, corporate profitability and market valuations. And, as the window narrows for IPOs to be completed in 2022, fund managers would likely continue to maintain their current positions rather than consider new opportunities. “It’s going to be a tricky period to navigate,” Dettman said. “On the capital markets side, I think investors will be cautious. What develops over the course of the next few months on the economic front is going to be a real driver for what the final quarter of the year looks like for IPO activity.”

Greg West of IDP Education noted that he had just returned from New York on (non-IDP) listed company business. This involved preparing companies for future fundraising, as well as introducing them to investment banks and other market participants. In many sectors, including fintech and biotech, the sentiment is that US capital markets have effectively “shut up shop” until the outlook is more certain.

Andrew Lockhart of Metrics noted that the Australian Government’s recent changes to benchmark the investment performance of superannuation funds had prompted re-allocations across a range of investment strategies. “Volatility is always a concern to us because it flows into nervousness around investments. People start switching,” he said. Calvin Kwok of Pinnacle added: “This is the time to invest with active managers. We’ve seen the shift from growth to value. Obviously, everyone is trying to navigate around the volatility quite carefully.”

Meeting urgent capital needs

Australian companies currently have limited options to raise capital, particularly as the major banks reduce liquidity. Yet in some situations the need to raise capital has increased.

Amelia Hill of MA Moelis noted that businesses may have invested heavily in inventory, potentially at high freight rates, as supply chain disruptions hit. Unable to pass the costs onto customers given the weaker macro environment, they now face increased margin pressure. Bing Jiang of Next Capital added that many companies are also having to deal with wage pressures and workforce shortages. These factors could reduce earnings, placing pressure on their ability to comply with debt covenants. These are all reasons companies may need to come to market to raise fresh funds.

Some private businesses have raised shorter-term capital in the pre-IPO market in recent years, typically issuing investors with debt that only converts to equity once public listing occurs. However, if an IPO cannot be executed before the near-term maturity of this debt, capital must be raised relatively urgently to repay it, or other arrangements negotiated.

On the plus side, publicly listed businesses are generally significantly less leveraged today than during the Global Financial Crisis (GFC). In addition, debt markets remain open, also unlike the GFC (although they are tighter). This has reduced the likelihood of a significant increase in emergency raisings to shore up over-extended balance sheets, according to Will Lawrence of Wilsons.

Where emergency raisings are required, roundtable participants did expect affected companies would be more likely to find support from existing shareholders looking to protect their existing investment. Garnering demand from new investors would likely prove difficult for companies in or near distress.

When the tourism industry experienced extreme difficulties during the pandemic, it was noted that Flight Centre and Webjet both issued convertible bonds to aid their post-pandemic recovery. While such structures can be complicated (and therefore, not appropriate in all instances), they represent an option where investors perceive value but are not tempted by the current share price.

The roundtable agreed it seemed highly unlikely current conditions would spur interest in vanilla bonds. Despite federal government reforms in 2014, a meaningful market has not eventuated, with raisings arguably still more costly for issuers relative to traditional bank finance.

Strategic capital raises

A key theme in equity capital markets is the switch in market power, from companies raising money to those providing it. Many institutional investors are flexing their muscles, seeking discounted share prices and greater liquidity in stocks.

Lockhart recounted how Metrics pursued an entitlement offer in early 2022. The initial plan to keep the offer open for several weeks was paused due to market volatility in January. An eventual two-week capital raising in February was completed with a separate wholesale investor placement subsequently arranged over a couple of days in May. Sometimes, he added, the decision to launch is purely driven by the market: “If investors are coming to us saying that they’d like to have the opportunity to participate in a capital raising – we’re responsive.”

Successful capital raises are also occurring where funds are needed to pursue accretive mergers or acquisitions. Dettman described a recent transaction in which insurer AUB Group undertook a $350 million equity raising to purchase a business in the United Kingdom (UK). AUB Group had a market capitalisation of $1.7 billion and the acquisition cost of the UK business was about $1 billion. The process was structured to minimise market risk, with the bulk of equity proceeds raised quickly. “This transaction illustrates that despite current market volatility, investors will support companies doing sizeable strategic acquisitions,” Dettman said. In subsequent weeks, this has further proven to be the case, with Carsales executing a very large capital raising to fund a well-received acquisition.

Prospects for growth stocks

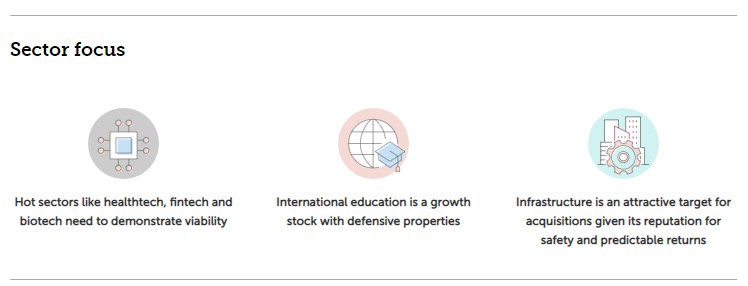

The roundtable heard how even promising companies looking to raise capital suddenly face renewed challenges to demonstrate viability – particularly in once ‘hot’ sectors such as healthcare, fintech and biotech.

Even promising companies looking to raise capital suddenly face renewed challenges to demonstrate viability.”

Until the markets recently cooled, sectors such as technology and biotechnology relied on capital markets to pursue growth objectives in areas such as research and development, capital expenditure and market share. Loss-making companies within these sectors will likely need additional capital to fund operating cash requirements. “The question will be whether existing shareholders and new investors see long-term opportunity in these companies,” said Lawrence.

Investors in growth stocks are now looking for financial discipline and positive cashflows. Anthony Brown of NobleOak Life, a growth-oriented life insurance company which listed on the ASX in July 2021, said that managing cost inflation was now the company’s biggest challenge. The war for talent and other labour supply shortages had made it difficult to find call centre and claims staff. “Investors want to know that we can still generate the right profit and manage inflation going forward.” Less profitable companies, which were gearing up for expansion, may find it challenging to adjust to the new circumstances and could struggle to access capital.

West added that international education occupies a unique position as a growth stock with some defensive properties. This is because international student mobility tends to maintain a steady rate of increase, despite economic shocks. Parents often save money for their children to get into overseas universities well in advance. Even when student demand drops, as previously seen during the GFC, it can catch up. Far from being deterred by the pandemic, some young people are eager to move forward, he added. As a result, even growth companies in this sector (and other growth sectors with defensive properties) should retain a level of capital market access, despite difficult conditions.

Public versus private equity

A major point of discussion at the roundtable was the shift to private asset classes, including private debt, private equity, venture capital and real estate. Speakers also discussed the consequent increase in both the availability of capital to companies from the private markets and the number of companies being taken off exchanges through take-privates. This trend is most advanced in the UK and US, where one participant observed that the number of publicly listed companies has fallen by about 40% over the last 20 years.

In Australia, the public markets are materially larger than the pools of private capital. However, the balance is starting to shift, and domestic pools of private capital are deeper than ever before. This is particularly as super funds start to deploy capital directly into private transactions, including M&As, and large stake investments in publicly listed companies. Examples include private equity bids in the large market capitalisation space, for companies such as Ramsay and Sydney Airport. Private raisings may also offer smaller to mid-size companies a funding option until public capital markets conditions improve.

The flight to infrastructure

Infrastructure assets are an attractive target for acquisitions given their reputation for safety and predictable returns. Taking publicly listed assets and making them private can be a good strategy for investors with long-term horizons, such as super funds. The corollary is there are now very few listed infrastructure plays on ASX, meaning that equity fund managers may be underweight in this class. This might lead to increased demand for assets of this nature, giving rise to IPO opportunities, and opening a way for sponsors and asset managers to make a clean exit.

One roundtable participant recounted how their company was initially involved in a private trade sale of an asset. Investor reluctance encouraged them to run a “dual track” process in which an IPO served as an alternative sale path, helping to maintain price competition. When the markets reopened after the first wave of the pandemic, the trade sale was abandoned altogether. “With an IPO sale, it’s easier,” this speaker remarked. “You’re not going to get pulled into a Takeovers Panel or have problems with the Australian Competition and Consumer Commission. With the assets that we deal in, there’s always going to be a place for alternative options such as an IPO because of those advantages.”

An increasing regulatory burden?

Regulation affecting equity capital markets was the final topic discussed at the roundtable. While Australia has traditionally been known for a more permissive capital raising regime than the US, MinterEllison’s Scotti noted that the ASX has significantly rewritten listings rules in recent years. Of course, many changes are sensible reforms, including those aimed at eliminating discredited practices or clarifying ambiguities. ASX is now proposing further changes that would result in greater regulation, including disclosure of how capital raisings are allocated.

Speakers noted that any disclosure requirements in relation to allocation should strike a balance between the need to provide useful information to the market and the preservation of a company’s flexibility in relation to allocations. Requirements which create artificial incentives to allocate to one group of investors over another may not be a positive evolution of the rules.

Several participants agreed that increasing listing rule regulation might have unintended consequences for listed companies, including where the discretion of boards is diminished. The roundtable participants discussed the pros and cons of the proposed changes to the listing rules. On the one hand, it was noted that increased disclosure may improve investors’ confidence that large placements are allocated fairly and appropriately. The counterview was that the disclosure requirement may act as a curb on directors’ discretion (and, therefore, their ability to fulfil their duties).

Looking ahead

Overall, there was confidence that equity capital markets will bounce back despite macroeconomic challenges and geopolitical uncertainty. Hill observed that cycles shift quickly, and a period of “consolidation and digestion” is inevitable after any shock. It took one to two years for the IPO market to rebound after the GFC. Even in March 2020, following the initial market dislocation caused by COVID-19, “we were all tearing up our IPO pipelines and shutting up shop for the year”, she said. Yet once governments had acted to stabilise the economy following lockdowns, investor education roadshows recommenced two months later.

“It’s a momentum game,” added Lawrence. He noted that once equity market conditions stabilise and some initial IPOs are successfully executed and trade well, "institutional managers will make returns and investors will get confident in the IPO market again.”

Institutional managers will make returns and investors will get confident in the IPO market again.”

In particular, Australia’s large superannuation holdings mean that considerable funds will continue to pour into listed equities. Just back from a venture capital conference in the US, ASX’s Beaton felt the story about the ASX was a very good one.

“From a speed and cost point of view, if you’re a company worth anywhere from $200 million to $2 billion, your ability to get access to an index here is significantly higher than the US,” he noted. “On a longer-term basis, I feel comfortable we're going to have a very active market here that continues to provide attractive capital for companies.”

Next steps

For now, the general observation seems to be that companies are waiting for volatility to settle before resuming activity. However, organisations could use this period productively to work on maintaining their ‘investor readiness’ through regular dialogue with potential investors and financial advisors.

Our Equity Capital Markets roundtable lunches will continue to run in the 2022/23 financial year in Melbourne and Sydney.