Economies across the Nordic region are posting steady growth despite geopolitical headwinds. Denmark has had a relatively strong year, with its economy set to grow 2 percent in 2025. Underlying factors such as healthy industrial production, renewed North Sea gas extraction and demand for pharmaceutical exports are all contributing to this expansion.

Sweden’s GDP growth was negatively impacted by geopolitical turbulence in the first half of 2025, but the market is now showing signs of recovery. Real GDP is predicted to increase from 1.5 percent in 2025 to 2.6 percent in 2026—a significant rebound driven by easing inflation, rising consumer confidence and a boost in private consumption.

Norway’s GDP is projected to increase by 1.7 percent in 2025, with solid income growth and supportive fiscal policy both driving things. As the US accounts for just 3 percent of its exports, Norway is less impacted than its regional peers by the US administration’s steep tariff hike. Yet declining oil prices could pose a concern due to a potential reduction in exports.

Finland’s economy experienced limited growth in 2024. The economy is predicted to resume growth over the next few years, but high unemployment and a government deficit remain a challenge.

Firm foundations

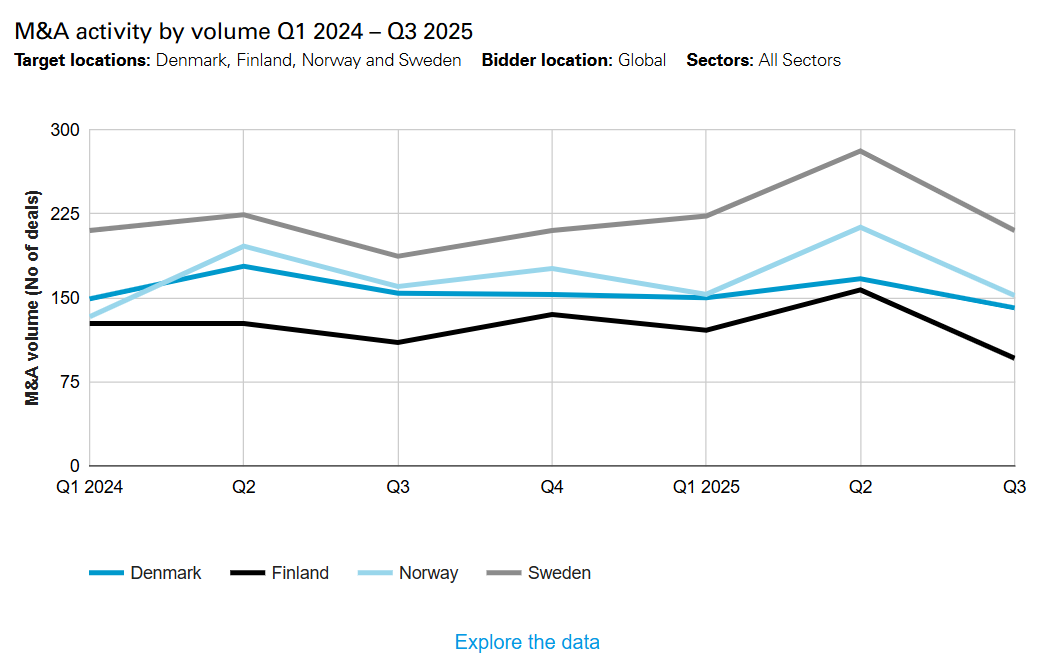

This generally positive economic performance is providing a firm foundation for M&A across the region. In the first three quarters of 2025, the volume total of 2,064 deals across Denmark, Finland, Norway and Sweden is already well ahead of the 1,955 recorded in the same period in 2024. Meanwhile, aggregate deal value of US$77.3 billion over the period has already surpassed last year’s total annual value (US$73.2 billion) with over a month of dealmaking left in the year. At the time of writing (December 15), that figure had risen to US$90.5 billion, from 2,473 deals.

Sweden is leading the way in terms of deal activity, securing the most deals in the first three quarters of the year. Swedish assets also attracted the highest deal values, with a total of US$31.1 billion (rising to US$34.3 billion at the time of writing), followed by Denmark at US$24.8 billion (up to US$26.4 billion at the time of writing). Marking a shift toward larger deals, Sweden and Denmark have both overtaken their respective 2024 values.

Despite Sweden’s dominance, it was Denmark that attracted the biggest deal across the region: Roche’s US$5.3 billion takeover of Zealand Pharma. The Swiss pharma giant reached an agreement with the Danish biotech company to develop its obesity drug, petrelintide, with the goal of expanding into the US and Europe.

The Nordic region continues to be sought after by international investors pursuing high-growth assets. In November, autonomous EV trucking company Einride announced a planned IPO through a SPAC deal with US-based Legato Merger Corp. III, which valued the Swedish company at US$1.8 billion. Einride is a key disruptor in the US’s carbon-intensive freight market, which is valued at an estimated US$4.6 trillion. The startup’s carbon-reducing freight solutions have already been piloted by large corporations such as PepsiCo.

PE powers ahead

PE activity has been a key driver of dealmaking across Denmark, Finland, Norway and Sweden. Sponsor deals (buyouts, secondary buyouts and exits) totaled US$32.1 billion in the first three quarters of this year—already surpassing 2024’s full-year total of US$19.2 billion. At the time of writing (December 15), that figure had risen to US$34.5 billion.

As a subset of total PE activity, primary buyouts have been particularly strong across the region, with the value figure of US$12.9 billion for the first nine months of 2025, outstripping the deal total for the whole of both 2024 (US$12.2 billion) and 2023 (US$10.8 billion). At the time of writing, this year’s primary buyout value had increased to US$15 billion.

Regional giant EQT and First Kraft’s US$4.5 billion bid for Fortnox, a local cloud-based accounting software company, marks the largest buyout of the year. Nordic software as a service (SaaS) providers have been highly sought after in recent years, elevating valuations across the sector. Another deal predicated on the region’s SaaS strength saw Goldman Sachs Alternatives acquire a majority stake in Trackunit, a Danish SaaS and internet of things (IoT) platform provider for the construction industry, from Hg and GRO Capital for US$1.4 billion.

Consolidation across the industry should continue to generate a healthy pipeline of deals moving forward.

Meanwhile, and in line with the largest strategic deal of the year so far, the life sciences sector has also proved a significant draw for PE players. In April, KKR acquired Karo Healthcare, one of Europe’s leading consumer health platforms, from EQT for more than €2.5 billion. And in the same month, US firm Hellman & Friedman joined CVC as a significant investor in Mehiläinen, Finland’s largest healthcare and social care provider. The financing round, in excess of €2 billion, is reportedly one of the largest ever in Finland.

More activity in the space is expected in the Nordics, according to reports from Mergermarket.

Deal drivers

Diverse sectoral strength is proving a key driver for M&A dealmaking in the four biggest Nordic economies. Healthcare, tech, transport and industrials have all provided ample M&A opportunities over the course of the year.

The life sciences industry has been particularly active, delivering the highest-valued deal of the year, namely the Roche-Zealand tie-up. At the time of writing (December 15), the pharma, medical and biotech sector had posted the highest deal value across all industries in 2025, at US$18.9 billion.

Medtech assets are being increasingly sought after by dealmakers. According to Ion Analytics, assets in the pipeline include Hermes Medical Solutions, a Swedish, Amplio-backed provider of medical imaging software for nuclear medicine, and Serres, a Finnish, Paree Group-owned surgical fluid solutions developer.

The Norwegian oil and gas sector is also open for business, with new entrants reportedly eyeing the space. Local oil and gas company DNO’s agreement to acquire rival Sval Energi for US$1.6 billion is set to quadruple its North Sea production, elevating it to top-tier status among Norway’s oil and gas producers. Lower oil prices have heightened interest in the Norwegian continental shelf, although high prices could put off prospective buyers.

The PE sector is also set to continue its increased investment in the region. Sectoral strengths—particularly in life sciences, technology and business services—relative economic and political stability, and the region’s reputation as a “safe haven” are all likely to drive further buyouts for the remainder of the year and beyond. Indeed, Swedish PE giant EQT noted in late October that it is looking to more than double its European investments, to €250 billion (US$292 billion), over the next five years.

Challenges on the horizon

The impact of the US’s “Liberation Day” tariff announcements on global markets has been widely publicized, with a heightened level of risk now surrounding deal negotiations. The Nordic region is particularly at risk. Its relatively small and open economies are exposed to fluctuations in market dynamics.

Sweden’s export-oriented economy is taking a hit. The finance ministry recently lowered its 2025 growth forecast due to uncertainty surrounding the US tariff policy. The impact is already being felt in the M&A market, particularly for deals involving the sale of companies with direct exposure to the US market. Finance Minister Elisabeth Svantesson acknowledged this issue in an interview with CNBC: "We are very dependent on exports,” she said. “With this uncertainty, companies are holding back, waiting for investments, because they don’t know what will happen. Will the tariff be 10 or 20 percent, or something else?”

Market ambiguity is also directly impacting due diligence processes. This is particularly true for companies with a global presence. In the past, having exposure to the US markets was seen as an asset, but it now carries potential risks to be assessed. The result is more lengthy and complex due diligence on deals, which could dampen M&A appetite moving forward.

Meanwhile, rising valuations could prove a barrier for dealmakers. Assets in the region’s high-growth sectors are proving increasingly attractive, driving up prices. According to Mergermarket data, the median EV/EBITDA multiple for deals announced in the Nordics so far this year is 12.9x, compared to 8.35x in 2024.

Outlook

The Nordic region as a whole is set for positive economic growth over the coming year, despite challenges surrounding the impact of the US’s tariff policy. Dealmaking appetite remains strong across a broad range of sectors, with strategic buyers and PE sponsors readying themselves for a busy year ahead. While companies with US exposure may potentially come under more scrutiny, this is unlikely to deter investors over the longer term.