Introduction

Complexity invites caution. The adage appropriately encapsulates the task of executing mergers and acquisitions that bear a nexus to China. Special challenge confronts M&A dealmakers when formulating and assigning appropriate valuations to Chinese enterprises. While conducting valuations in China generally involves the application of customary, time-tested methodologies, the task often necessitates more. Specifically, it is important for M&A dealmakers, senior management teams and corporate boards to understand, and base strategic decisions, in part, on, the idiosyncrasies of China’s market when evaluating M&A transactions that implicate the region. Unique characteristics innate to China have the potential of impacting directly the quality of M&A valuations of Chinese enterprises, often presenting a task of challenge for American and European acquirers.

M&A valuations in China generally necessitate the application of valuation methodologies customarily used in advanced industrialised economies (eg, the United States, Great Britain). Conventional methodologies include tools such as ratios of enterprise value/EBITDA and price/earnings per share, among other metrics. Valuation methodologies for China M&A transactions retain core similarities to methodologies used in the United States and in Europe. Likewise, financial valuation modelling for Chinese enterprises remains comparable to techniques used in other advanced markets.

And yet, differences abound. Considerations unique to China’s market often factor significantly in M&A valuations of Chinese enterprises. Those considerations include the company's market share position, the source of domestic financing, the location of the company’s headquarters, the quality of the local Chinese manager and the quality of outside advisers, among other factors. M&A dealmakers and senior management teams are wise to conduct due diligence around these considerations when undertaking M&A valuations of Chinese enterprises – whether privately held or listed entities.

In assigning M&A valuations to Chinese enterprises, M&A dealmakers tend to focus more significantly on future earnings prospects rather than on historical cash flows. A driving factor for this approach is that many Chinese enterprises – particularly those in more nascent phases of business development – generally lack demonstrable track records of free cash-flow generation and profitability. Consequently, M&A dealmakers must look to Chinese enterprises' projected earnings potential and probable growth scenarios and generate valuations utilising discounted cash flow (DCF) analyses and corresponding capital asset pricing calculations.

This chapter explores and analyses key aspects of M&A valuations in China, including discussions on valuations, methodologies and other important considerations. We discuss historical valuation trends in China M&A, including overviews of primary methodological tools in valuing Chinese enterprises listed on the Shanghai and Shenzhen exchanges. The chapter also explores customary valuation techniques and discusses the applicability of enterprise value/EBITDA multiples and other common metrics, including DCF analyses as they relate to China M&A transactions. In addition, we analyse key qualitative drivers of M&A valuations in China, including factors pertaining to market share concentration, sources of financing, the location of a domestic enterprise's headquarters and the role of outside advisers. Finally, the chapter provides an overview of new trends in China M&A valuations and explores several recent China M&A transactions of consequence.

Historical P/E valuation trends in China M&A

Within the China M&A landscape, the price to earnings per share (P/E) ratio constitutes the most common metric for valuing listed Chinese enterprises. The P/E ratio generally derives from the price of an enterprise's stock divided by its earnings per share for a given fiscal period. The P/E ratio generally constitutes an important indicator of a listed enterprise's valuation on either an historical or forward-looking basis. Because P/E ratios factor so prominently in valuations of listed Chinese enterprises, M&A dealmakers generally tend to consider more significantly listed Chinese enterprises' earnings growth and net income profitability as compared to its EBITDA potential.

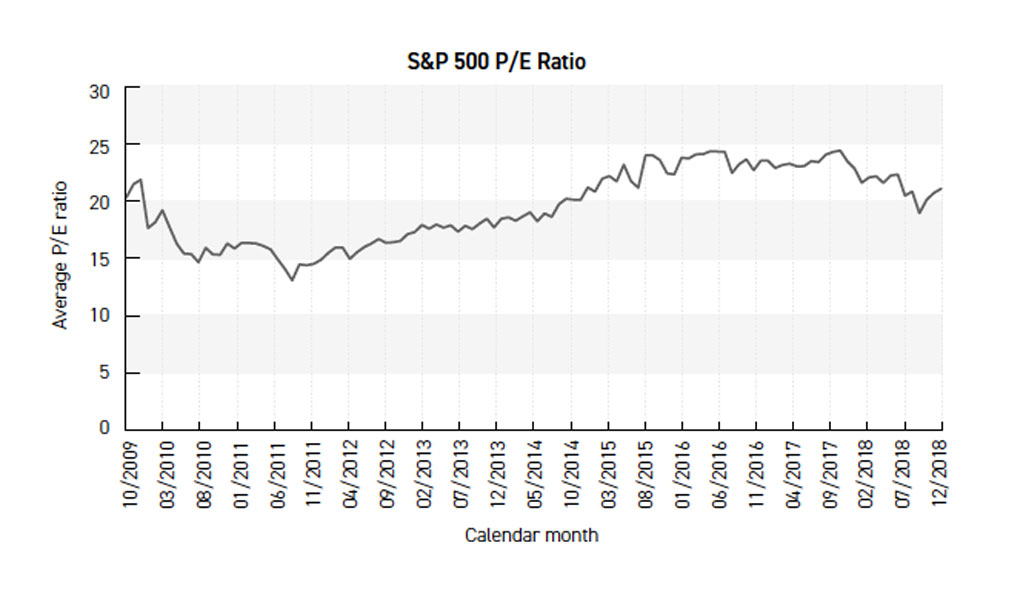

Most recently, as of January 2019, the average P/E ratio for China-listed enterprises was 22.2, which contrasts with an average P/E ratio of 26.9 for all US publicly traded businesses.2 During the past 10 years, the historical trend of P/E ratios for Chinese enterprises listed on the Shanghai Stock Exchange has demonstrated a relatively strong correlation to the trend of P/E ratios observed among comparable US-listed businesses. From October 2009 to March 2019, the average P/E ratio for the S&P 500 increased from 20.3 to 21.1, with the average ratio declining to 13 in September 2011 and rising steadily to 24.5 in January 2018.3

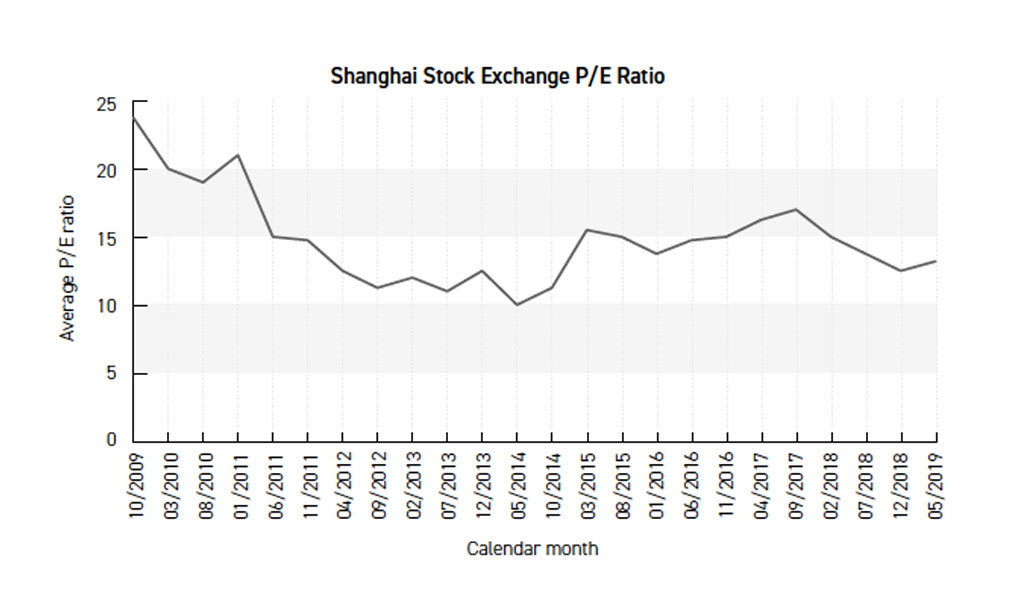

During the same time period in China, the average P/E ratio for the Shanghai Stock Exchange declined from approximately 23.8 in October 2009 to 13.2 in March 2019. The average P/E ratio decreased to approximately 9.5 in June 2014 and rose to approximately 25 in June 2015. In addition, the average P/E ratio declined approximately to 13.5 in March 2016 and then continued to rise steadily to approximately 20 in January 2018.4

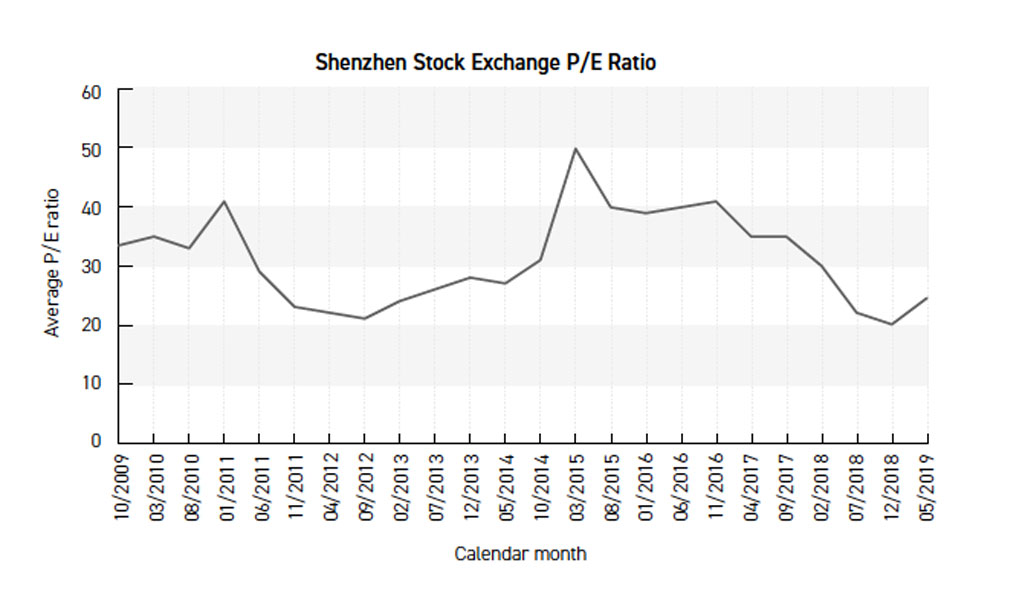

Beyond the Shanghai Stock Exchange, average P/E ratios on the Shenzhen Exchange reflect valuations that trend higher compared to levels observed in the United States. While both the Shanghai Stock Exchange and the Shenzhen Exchange formally opened in 1990, the two exchanges bear differences. Significantly, businesses listed on the Shanghai Stock Exchange collectively possess an approximate market capitalisation slightly over US$5 trillion and consist of most of China’s oldest companies and state-owned enterprises (SOEs). By contrast, enterprises listed on the Shenzhen Exchange collectively possess a smaller aggregate market capitalisation – approximately US$3.5 trillion. The Shenzhen Exchange consists of newer and more growth-oriented enterprises, including many software and technology businesses in China.

In China, during the 10-year period from 2009 to 2019 P/E ratios on the Shenzhen Exchange declined markedly. In October 2009, P/E ratios on the Shenzhen Exchange averaged approximately 33.5, while in March 2019, the P/E ratios averaged approximately 24.5, representing a total decrease of approximately 26.9 per cent. In addition, notably during this period, average P/E ratios on the Shenzhen Exchange fell to approximately 19 in October 2012 and rose to approximately 61 in June 2015, representing an increase of approximately 221 per cent. P/E ratios trended near 40 for much of CY2016 and CY2017 and have decreased steadily to their current levels in CY2019.5

Key valuation methodologies in China M&A

Several principal methodologies generally underpin valuations of Chinese enterprises. A common technique is to identify a series of precedent transactions within a given industry in China. By grouping deals and corresponding transactional financial data, M&A dealmakers and management teams may calculate average transaction multiples paid in connection the subject transactions. In precedent transactions analyses involving China M&A deals, transaction multiples typically derive from P/E ratios in the case of listed Chinese targets and enterprise value to EBITDA (EV/EBITDA) multiples in the case of privately held targets. In some cases in China M&A, transaction multiples derive from enterprise value to revenue (EV/revenue) multiples, but this approach generally is less common. M&A dealmakers and management teams may determine to aggregate precedent transaction multiples for a specific target enterprise for the purpose of calculating both average and median transaction multiples. Following this exercise, it is common to undertake comparable calculations for other target enterprises in China M&A transactions, thereby yielding a series of transaction multiples across a broad spectrum of deals in similarly situated industries or sectors.

By using this approach, M&A dealmakers and management teams can assess more holistically an approximate valuation for a potential target enterprise that may be ripe for acquisition in China. The approach is especially useful in the China M&A setting because it generally avoids reliance on a target enterprise's historical operating performance or profitability, which can be elusive for newer, less-established Chinese enterprises. Accordingly, precedent transactions analyses find a fitting home on the desks of M&A dealmakers and management teams seeking to undertake informed valuations of Chinese enterprises across industries.

In addition to precedent transactions analyses, methodologies focused on P/E ratios and EV/EBITDA multiples feature prominently in valuations of Chinese enterprises. P/E ratios – and less so EV/EBITDA multiples – apply to valuations of listed Chinese enterprises, while EV/EBITDA multiples – but not P/E ratios – apply to valuations of privately held Chinese businesses. A principal advantage of P/E ratios is their durability: assuming the stock of a Chinese enterprise continues to be listed, a P/E ratio may be derived from the enterprise's stock price and earnings per share, yielding a consistent measurement of the enterprise's valuation over time. EV/EBITDA multiples generally find most utility in valuations of privately held Chinese targets that do not hold publicly traded shares. Calculations of enterprise value for Chinese enterprises generally track conventional methodologies used in more advanced industrialised markets, with enterprise value calculations based on the sum of an enterprise's total debt and total equity capitalisation (number of fully diluted shares multiplied by a given price per share) less cash and cash equivalents held on the enterprise's balance sheet. As in other industrialised markets, EBITDA for Chinese enterprises generally serves as a proxy for cash flow and enables EV/EBITDA multiples to be derived for virtually any business – privately held or listed – in the country. It should be noted additionally that, while less common, EV/revenue multiples also find a home in valuations of both listed and privately held Chinese enterprises.

Added to valuations derived from P/E ratios, EV/EBITDA multiples and EV/revenue multiples are DCF analyses of Chinese enterprises. DCF analyses produce intrinsic – or fundamental – valuations of target businesses based on calculations rooted in projected future cash flows, a terminal year and an appropriately risk-adjusted weighted average cost of capital – or 'discount rate'. DCF analyses generally are undertaken in valuations for both listed and privately held Chinese enterprises. In the China M&A setting, DCF are less frequently used compared to other valuation methodologies. Driving this is partially a function of the financial profile of many Chinese enterprises: DCF analyses generally rely on relatively consistent operating performance and demonstrable track records of free cash-flow generation, which elude many Chinese businesses, particularly those in more growth-oriented sectors such as software and early-stage technology. Valuations derived from DCF analyses are undertaken with greater frequency when assessing the intrinsic value of Chinese enterprises with longer demonstrations of cash flows and a clearer line of sight into sustainable future earnings potential.

Additional valuation considerations in China M&A

Conventional valuation methodologies represent the principal tools underpinning M&A valuations in the US and European markets. They also factor prominently in conducting intrinsic valuations of Chinese enterprises. However, valuations of Chinese enterprises that derive solely from the use of conventional methodologies – and nothing more – generally are inadequate for purposes of discerning the full picture of an enterprise's underlying value. Additional considerations drive valuation in China M&A and, in the aggregate, can factor significantly in – and sometimes equally alongside – valuations derived from an enterprise's cash-flow generation, EBITDA margin, earnings growth and profitability. Here, we discuss salient valuation considerations that may be integrated into discussions among M&A dealmakers and senior management teams when seeking to execute M&A opportunities in China.

Market share

The market share held by a Chinese enterprise within a given industry can factor significantly in assessments of the enterprise's valuation. A company's market share expresses the company's revenues measured as a percentage of an industry's total revenues. In other words, an enterprise's market share typically is derived by dividing the total revenues of the enterprise by the industry's total revenues over a given fiscal period. While market share assessments are not singularly unique to the China market, they become especially salient in valuations of Chinese enterprises due to the general nature of industry in China.

Significantly, the market share of smaller, less-established Chinese enterprises is comparatively less stable relative to what generally is observed in the United States and other industrialised economies. Driving this are several factors. For one, sectors in China typically are more fragmented and dynamic within the lower-middle market in terms of the number of sector players and the relative market positioning held by a smaller Chinese enterprise. It is common for a given Chinese sector to oscillate drastically in terms of the sector's number of bona fide lower-middle market players. For example, the launch of a new Chinese consumer business touting innovative apparel often will be accompanied in China by the emergence of other small apparel businesses – some legitimately formed, many not – claiming identical or comparable branding and intellectual property. Aside from the substantial costs and reputational harm exacted by this phenomenon in China, it fosters a business environment within which hundreds, and sometimes even tens of thousands, of smaller Chinese enterprises – many with dubious legal footing – may be formed, operated and dissolved within short periods. This environment generally creates substantial variability and uncertainty with respect to the purported market share held by smaller Chinese enterprises for a given fiscal period. Amid such uncertainty and volatility within the lower end of sector activity in China, the market share of a smaller Chinese enterprise generally either is discounted or should weigh on the enterprise's valuation.

By contrast, the market share of larger or more dominant Chinese enterprises generally is more concentrated and stable relative to what is observed among the largest businesses in the United States and other industrialised economies. Several considerations underpin this phenomenon. While sector consolidation manifests itself in China, it occurs at a more measured pace among the largest and most established Chinese enterprises. China's lower levels of consolidation generally are attributable to the country's comparatively less-developed financial and capital markets, its lower levels of market liquidity and its less robust dispute resolution fora. Because of these attributes, once a Chinese enterprise achieves substantial market share (eg, 25 per cent) within a given sector, its market position is less prone to significant competitive disruption or takeover. As a result, a market-dominant player within a given sector in China generally can preserve market share more effectively. From a valuation standpoint, the practical effect is to weight such market share consideration more highly and elevate the valuation of the Chinese enterprise. Industry players that bear a formidable market share foothold in China generally should carry valuations above what is otherwise expressed through fundamental valuation analyses, all other considerations being equal.

Several sectors in China bear significant market share concentration. In these sectors, several Chinese enterprises capture a significant – sometimes a majority – share of the market. This is especially true in sectors with significant numbers of SOEs, which are supported more proactively with capital investment and other direct forms of endorsement from the Chinese government. Sectors with SOEs capturing a significant portion of market share include:

- civil engineering;

- forging pressing, stamping of metal;

- mining support;

- manufacture of railways;

- mining of coal and lignite;

- support activities for oil and gas extraction;

- professional services;

- transport equipment;

- petroleum and natural gas; and

- extraction of crude petroleum.

A fair assumption in valuation analyses of Chinese enterprises is that a privately owned business operating in a sector dominated by SOEs may experience substantial challenge in its attempts to achieve meaningful growth. In this way, sector concentration is correlated with market share: a new market entrant in an SOE-dominated sector likely will face headwinds in seeking to secure a greater market share, while state-buttressed SOEs generally are able to preserve – and even enhance – their share of the market.

Source of financing

While the business model, revenue, cost structure and free cash-flow profile generally constitute significant components of valuations of Chinese enterprises, in many instances, additional qualitative considerations around the enterprise's source of financing can weigh as significantly as conventional quantitative metrics. In executing M&A transactions bearing a nexus to China, M&A dealmakers and senior management teams – whether American, European, Chinese or otherwise – may determine that the most optimal acquisition structure necessitates the use of outside financing regarding debt, equity or other mutually agreed considerations. The source of financing – as well as the quality and integrity of the subject financing institutions – may feature prominently in discussions centred on evaluations of target Chinese enterprises. Financing due diligence generally constitutes an integral feature of M&A transactions in US and European settings, but it becomes especially salient to valuations where Chinese financing sources are in play. Rigorous due diligence of prospective financing sources is particularly apposite in China given the country's unique and broad panoply of domestic financing institutions, including equity syndicates, state-owned commercial banks, SOE consortia, government investment vehicles, trust structures, special purpose vehicles and lesser-known private investment vehicles.

The rationale for comprehensive financing due diligence for valuation purposes is straightforward enough: China's capital markets – both public and private – historically have been beleaguered by comparatively deficient financing protocols, high levels of opacity and other sub-optimal processes that fall short of 'best practices' observed in US and European markets and other advanced industrialised economies. These inherent risks in China's capital markets become magnified by pervasive 'shadow banking' practices that continue to occur outside of China's regulated financial system and pose increasing levels of systemic risk to the Chinese economy and to capital market and M&A participants. And while the Chinese government has acknowledged persistent problems with China's under-developed financial system and has implemented policy measures to attempt to eliminate China's shadow banking practices and other deficient protocols in institutional lending practices, the gravity of the problems still cannot be overstated. An all-too-common lack of transparency with respect to financing sources generally both hinders the execution of China M&A deals and complicates financing due diligence processes undertaken at all key stages of a transaction's life cycle. It is important for M&A dealmakers and senior management teams to focus closely on the prospective source of financing when executing China M&A transactions.

It is also important to integrate appropriately the source of financing into assessments of a target Chinese enterprise's valuation. Higher-quality debt or equity financing sponsored by known and regulated financial institutions in China generally bodes favourably for a target Chinese enterprise's valuation, while convoluted financing structures organised through opaque, unregulated individuals or entities generally will weigh on a target's valuation. The presence of a US or European financing source generally will mitigate some of these concerns and factor more positively in a target company's valuation. In addition, the use of escrow funding and target-level financing may also alleviate concerns over funding certainty. In the final analysis, M&A dealmakers and senior management teams are wise to factor in the source of financing into valuation considerations; doing so generally enables a more fulsome and accurate picture of fair consideration.

Outside advisers

The role of outside advisers can feature prominently in China M&A valuations. Perhaps more so than any other M&A market globally, China is singularly unique in both the overall complexity of its business landscape and its prerequisites for transacting successfully in the country. For M&A dealmakers and senior management teams, securing tailored strategic advice and robust China expertise from outside advisers generally is advisable. In addition to its complex economic environment, China's distinctive relational and cultural dynamics necessitate bespoke strategic and business advice when undertaking M&A transactions of scale in the country. Outside advisers can play a vital role in evaluating key industry dynamics in China, transaction processes, commercial and financial due diligence, negotiation dynamics, deal synergies and post-closing integration strategies, among other transaction considerations. Advisers with established track records and career expertise in China can add credibility to M&A processes and to the advice of other co-advisers during transactions, enabling more comprehensive valuations to be undertaken alongside senior management teams. By contrast, advisers with little or no experience in dealing with China often can overcomplicate China M&A processes, even impairing valuation assessments, whether on the buy-side or sell-side.

Additional qualities in outside advisers remain highly sought-after by senior management teams and corporate boards in the China M&A setting. Is the outside adviser proficient or fluent in Mandarin? Does the adviser possess a keen understanding of China's business landscape? Has the adviser cultivated a high level of acumen on China M&A through career work in China, language or cultural immersion programmes in China, travel throughout China or institutional relationships and affiliations with China-focused professional organisations? Factoring these considerations generally is advisable for senior management teams and corporate boards when determining the selection of outside advisers for China M&A transactions.

Headquarters

An additional consideration underpinning valuations of Chinese enterprises centres on the location of the target company's headquarters. Typically the province of management executives and other senior decision-makers within Chinese enterprises, the location of a target company's headquarters often factors significantly in China M&A valuations. This is largely because the proximity of a headquarters to key stakeholders generally signals an enterprise's capacity to undertake value-creating strategic initiatives with speed and agility. For example, the proximity of a Chinese enterprise's headquarters to stakeholders such key customers, suppliers, advisers, employees and investors often strengthens the company's ability to execute consequential decisions expeditiously. Likewise, the closeness of headquarters to domestic financing sources – whether institutional or otherwise – can reinforce the company's relationships with debt capital providers, yielding more productive periodic credit committee discussions and enabling swifter resolution of financing-related negotiations or disputes. Similarly, the nearness of headquarters to key transportation systems – including airports, waterways and major highways – generally enhances business efficiencies of Chinese enterprises and generates more effective execution of important corporate initiatives that touch upon key customer relationships, supply chain management and distribution network optimisation.

Generally, the proximity of an enterprise's headquarters to major urban centres in China – for example, Shanghai, Beijing, Hong Kong and Shenzhen – bears positively on the enterprise's valuation. Conversely, in the absence of significant mitigating factors, a company's headquarters located in commercially less developed regions of China – and far removed from China's principal centres of financial and capital markets, key transportation systems and digital networks – generally weighs on the company's valuation. Finally, while exceptions abound, it is generally the case that Chinese enterprises located in commercially more developed urban centres adhere more strictly to robust internal controls, established accounting standards and, in the case of listed enterprises, best practices in financial reporting. These considerations generally buttress a Chinese enterprise's valuation or at least combat other mitigating negative factors that might weigh on valuation.

Recent valuation trends in China M&A

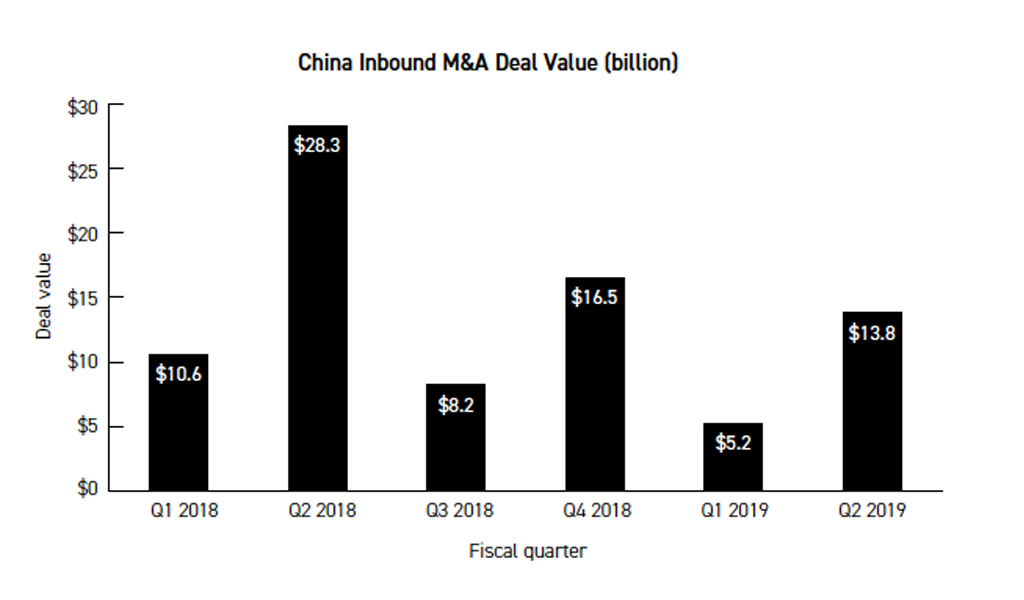

Inbound China M&A transactions

In H1 2019, a total of 89 inbound China M&A transactions materialised, yielding an aggregate deal value of US$19 billion. The adjusted EV/revenue multiples for those H1 2019 transactions averaged 4.9, while EV/EBITDA averaged 13.1. During H1 2018, a total of 119 inbound China M&A transactions materialised, yielding an aggregate deal value of US$38.9 billion. For those transactions in H1 2018, the adjusted EV/revenue multiples averaged 17.9, while EV/EBITDA multiples averaged 28.7.6

With respect to inbound M&A transactions into China, 20 such transactions materialised during H1 2019, reflecting an aggregate deal value of US$9.6 billion. In terms of valuation, those transactions reflected an average adjusted EV/EBITDA multiple of 13.0 and an adjusted EV/revenue multiple of 2.4. By comparison, during H1 2018, 25 inbound China M&A transactions materialised, with an aggregate deal value of US$21.8 billion. Those inbound transactions in H1 2018 reflected an average EV/EBITDA multiple of 51.7 and an average adjusted EV/revenue multiple of 35.3. The recent general trend with inbound China M&A transactions accordingly reflects a decrease in the total number of such transactions, a precipitous drop in the aggregate deal value and substantial declines in the target valuations as measured by conventional EV/EBITDA and EV/revenue multiples.

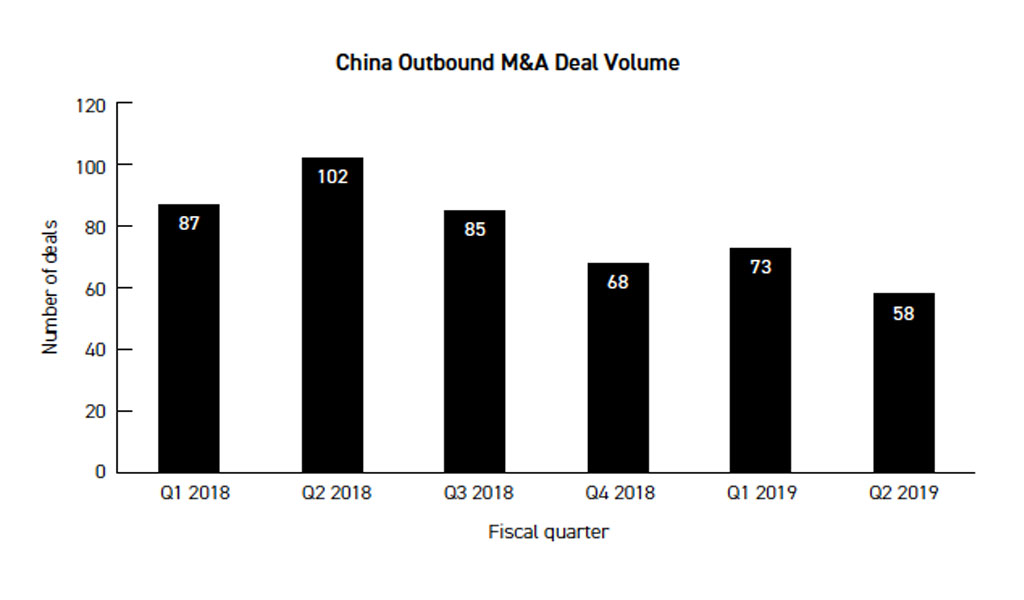

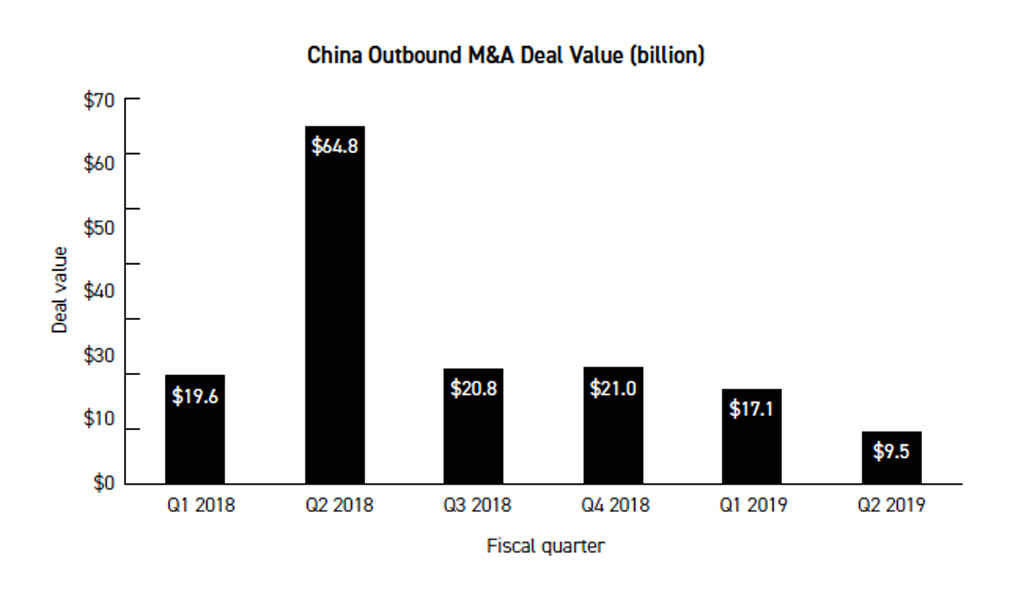

Outbound China M&A transactions

In H1 2019, a total of 131 outbound China M&A transactions materialised, yielding an aggregate deal value of US$26.6 billion. The adjusted EV/revenue multiple for those H1 2019 transactions averaged 2.9, while EV/EBITDA multiples averaged 33.1. This contrasts starkly with higher figures observed during H1 2018 in which 189 outbound China M&A transactions materialised, yielding an aggregate deal value of US$84.4 billion. For those transaction in H1 2018, the adjusted EV/revenue multiple averaged 8.5, while EV/EBITDA multiples averaged 12.1.

For CY 2018, the number of 'mega' China M&A transactions (ie, transactions exceeding US$1 billion in total enterprise value) remained flat relative to volumes observed In CY 2017. The relatively stable deal volumes were attributable largely to fewer mega outbound China M&A transactions – with a 29 per cent decrease from levels observed in CY 2017 and a 60 per cent decrease from levels observed in CY 2016 – offset by a moderate increase in the number of mega M&A transactions undertaken by financial sponsors and domestic strategic players.

Valuation trends by industry in China

M&A valuations of target Chinese enterprises in H1 2019 reflected an average adjusted EV/EBITDA multiple of 26.3.7 During the same period, the average adjusted EV/EBITDA multiple for US targets was 18.5.8 As shown in the table further below, differences in EV/EBITDA multiples between US and Chinese businesses with respect to certain sectors during CY 2018 generally reflected higher valuation multiples for Chinese businesses. While the composite average EV/EBITDA multiple for Chinese businesses of 13.4 was lower compared to a composite average EV/EBITDA multiple of 14.8 for US businesses, the higher composite multiple for the US market was driven principally by outlier EV/EBITDA multiples attributable to US real estate market.

|

Industry |

EV/EBITDA (China) |

EV/EBITDA (US) |

China % difference |

|---|---|---|---|

|

Total market |

13.39 |

14.77 |

-10.3 |

|

Machinery |

14.75 |

10.79 |

26.8 |

|

Electronics (general) |

12.41 |

10.46 |

15.7 |

|

Drugs (pharmaceutical) |

13.91 |

13.46 |

3.2 |

|

Real estate (development) |

8.85 |

33.80 |

-281.9 |

|

Apparel |

10.86 |

10.08 |

7.2 |

|

Auto parts |

10.87 |

5.20 |

52.2 |

|

Construction supplies |

6.82 |

9.07 |

-33.0 |

|

Metals and mining |

9.54 |

4.09 |

57.1 |

|

Software (system and application) |

26.21 |

20.21 |

22.9 |

Notable China M&A transactions

Several notable China M&A transactions materialised in CY 2019, especially in the sectors of real estate, technology, cloud computing, artificial intelligence and car sharing. For example, on 27 February 2019, an investor group led by SK Hynix Inc, a South Korea-based manufacturer of semiconductors, purchased for US$600 million an undisclosed stake in Beijing Horizon Robotics Technology Development Co, Ltd, a China-based company engaged in research and development of AI chip and algorithm software for smart driving, city and retail operations.

On 28 February 2019, Softbank Group, the Japan-based company focused on telecommunications and technology innovation, purchased the Chehaoduo Used Car Agency, the China-based consumer-to-consumer used-car trading platform, for US$1.5 billion, consummating the acquisition through Softbank’s Vision Fund. On 1 March 2019, an investor group led by Tiger Global Management, LLC, the international investment firm, purchased for US$500 million an undisclosed stake in Ziwutong (Beijing) Asset Management Co, Ltd, the China-based real estate company engaged in long-term rental apartments. On 8 May 2019, a consortium of bidders acquired for US$750 million an undisclosed stake in Megvii Technology Limited, a China-based company engaged in developing cloud-based facial recognition and AI technology. The consortium included Macquarie Group Limited, Abu Dhabi Investment Authority, Alibaba Group Holding Co, Ltd, Bank of China Group Investment Limited, the Hong Kong-based investment arm of Bank of China Limited, and ICBC Asset Management (Global) Company Limited, the Hong Kong-based investment arm of the Industrial and Commercial Bank of China Group. The total deal consideration of US$750 million reflected an EV/revenue multiple of 15.1.

On 15 May 2019, City Developments Limited, the Singapore-based real estate development and investment company, purchased for US$800 million a 23.9 per cent stake in Xiexin Holding Group Co, Ltd, the China-based real estate developer. On 29 May 2019, Bain Capital, LP, the American private equity firm, purchased for US$570 million an undisclosed stake in Beijing Stack Data Co, Ltd, the China-based cloud computing business. On 23 June 2019, Carrefour SA, the French supermarket giant, sold an 80 per cent stake of its Carrefour China Holdings NV to Suning.com Co, Ltd, the China-based home appliance retail business, with the purchase price reflecting an EV/revenue multiple of 0.4.

Conclusion

Producing valuations in China M&A transactions generally involves a bespoke process combining the use of conventional valuation methodologies and selected integration of supplemental considerations unique to China's economy and business landscape. It is advisable for M&A dealmakers, senior management teams and corporate boards to understand, and base strategic decisions, in part, on, the idiosyncrasies of China’s market when evaluating M&A transactions that implicate the region. Unique characteristics innate to China have the potential of impacting directly the quality of M&A valuations of Chinese enterprises. M&A valuations in China generally require the use of valuation methodologies customarily used in advanced industrialised economies, including precedent transaction analyses, P/E ratios, EV/EBITDA multiples, EV/revenue multiples and DCF analyses. Additional considerations unique to China’s market can factor significantly in M&A valuations of Chinese enterprises. Those considerations include the company's market share position, the source of domestic financing and quality of the local Chinese manager, the location of the company’s headquarters, the quality of the outside advisers, among other factors. Finally, China M&A transactions during CY 2019 underscore continued appetite for M&A dealmaking in China, notwithstanding sustained US–China trade tensions impacting negatively overall capital flows and commercial activity bearing a nexus to the region.