Effective January 1, 2018, franchisors that wish to help their franchisees qualify for loans backed by the U.S. Small Business Administration (SBA) must be listed on the SBA’s new “Franchise Directory.” SBA-guaranteed small business loans have long been a routine way for franchisees to fund the acquisition and development of new franchises.

What’s the SBA’s role in franchising?

The SBA guarantees conventional bank loans to independent small businesses. A franchisee will not qualify as a small business if the SBA finds the franchisor retains too much control over the franchisee as the SBA treats the franchisor and franchisee in this case as “affiliates.” The Franchise Agreement provisions that tip the SBA’s “affiliation” scale and render a franchisee ineligible for an SBA-backed loan include common provisions like those giving the franchisor a right of first refusal upon a franchisee change of ownership or a right to buy franchise assets upon termination of the Franchise Agreement.

Why the change?

For years, franchisors resolved the SBA’s affiliation concerns by adding a pre-negotiated amendment to their Franchise Agreement and getting their franchise brand listed on a Franchise Registry maintained by a third-party vendor, FranData. The FranData process, while not inexpensive, worked relatively well in reducing SBA-backed loan processing times … until recently.

What is changing?

The new SBA Franchise Directory (“Franchise Directory”) represents the SBA’s effort to streamline loan processing for franchisees. It replaces the former Franchise Registry and provides a centralized list of all franchisors whose franchisees are eligible to obtain SBA-backed loans.

When does this change take effect?

Starting January 1, 2018, a franchisee’s application for an SBA-backed loan will not be processed by a bank unless the franchise system it is buying into is on the Franchise Directory.

What information appears on the SBA Franchise Directory?

The Franchise Directory lists the following information for each franchise brand that meets the FTC Rule’s definition of a franchise:

- The franchise brand’s SBA Franchise Identifier Code

- If the franchisee must sign an addendum to the franchisor’s Franchise Agreement and, if so, whether it is the SBA’s standard addendum (SBA Form 2462) or a negotiated addendum

- Any additional issues a lender should consider in reviewing loan applications from franchisees of the franchise brand

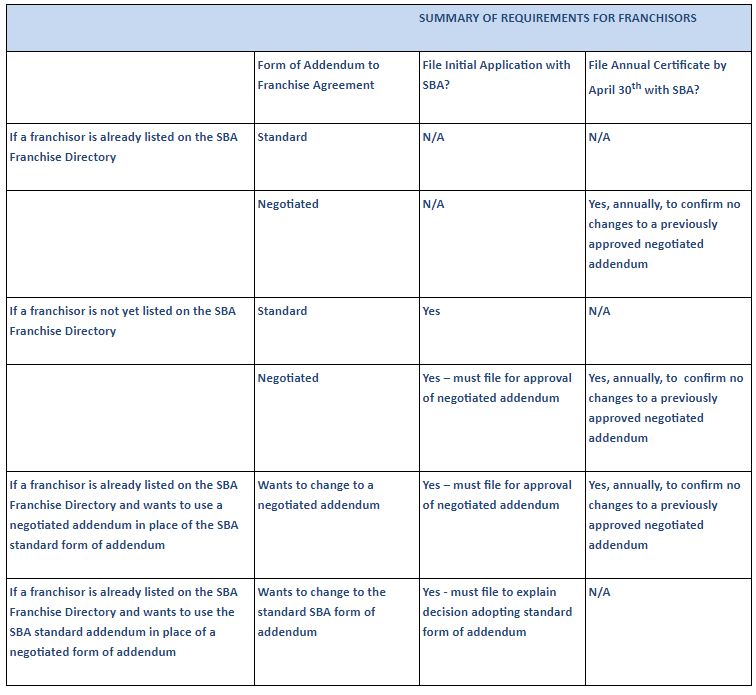

What must franchisors do to help their franchisees secure SBA-backed financing?

- First confirm if the franchise brand is listed on the Franchise Directory and if the information is accurate. The SBA lists many franchise brands that were formerly eligible. To check, follow this link.

- If a franchisor wants to be added to the Franchise Directory, it must submit its Franchise Disclosure Document with all exhibits to [email protected]. To make an initial filing, follow this link.

- Depending on whether a franchisor is willing to accept the SBA’s standard form of Addendum to Franchise Agreement (SBA Form 2464) or prefers negotiating its own addendum with the SBA, a franchisor will have additional requirements:

Why should a franchisor consider using the SBA’s standard form of Addendum?

Franchisors that agree to use the SBA’s standard addendum to Franchise Agreement are presumed to satisfy the SBA’s affiliation requirements and excused from having to file an annual certification. Franchisors that prefer using their own form of addendum must submit the addendum to the SBA for review and approval and file a certificate by April 30th of each year representing that (i) the terms of their Franchise Agreement that affect “affiliation” (i.e., certain controls) have not changed; and (ii) the form of negotiated addendum is unchanged. There is no filing fee for the annual certification.

What does the SBA’s Standard form of Addendum look like?

The addendum amends any Franchise Agreement to the contrary in the following ways:

- Events of Transfer: The franchisor will not unreasonably withhold its approval to events constituting a “transfer” or change of ownership of the franchisee. Furthermore, a right of first refusal will not be exercised if it would prevent a current owner or family member from acquiring the selling owner/franchisee’s interest in the franchise. Finally, a seller will not be liable to the franchisor for post-sale liabilities.

- Forced sale of assets: A neutral third party appraiser must determine the value of franchise assets if the Franchise Agreement gives the franchisor an option to buy them upon termination or expiration of the Franchise Agreement and the parties cannot agree to a price. The franchisor’s option to buy franchise assets must exclude any real estate that the franchisee owns and uses to operate the franchise business.

- Covenants: When a franchisee owns the real estate where the franchise business operates, the franchisor may not record restrictions that affect land use or transfer.

- Employment: A franchisor may not directly control (hire, fire, discipline, schedule, or set pay or other employment benefits or conditions) its franchisees' employees.

Why would a franchisor not want to use the SBA’s standard form of Addendum to Franchise Agreement?

- The SBA’s Standard form of addendum uses imprecise terms.

- Many franchisors prefer using their own Franchise Agreement addendum to avoid overbreadth issues with the SBA’s standard form.