Introduction:

The Ministry Corporate Affairs (MCA) has, since October 2017, notified Section 247 of the Companies Act, 2013 and introduced the Companies (Registered Valuers and Valuation) Rules, 2017 (RV Rules). In order to give the valuation industry some time for adopting the new regime, the MCA allowed time till 31 January 2019[1] for existing valuers to continue their valuation services and register themselves into a registered valuer. Now, from 31 January 2019 onwards, only a ‘registered valuer’ is permitted to undertake valuation required under the Companies Act and rules made thereunder. For the first time, the profession of valuers has received a statutory recognition similar to profession of Chartered Accountants, Company Secretary and Insolvency Resolution Professionals and has been subjected to various rules and regulations for governing it. The MCA has designated the Insolvency and Bankruptcy Board of India (IBBI) as the authority for implementing the new regime of registered valuers in addition to the insolvency resolution professionals.

Who can be a registered valuer?

A person, who aspire to be a registered valuer, is required to possess certain qualifications and experience, obtain membership of a recognised organisation of valuers and get itself registered as a valuer with IBBI. The RV Rules sets out in detail the eligibility criteria, educational qualifications (degree), experience, and procedure for registration of a valuer.

The RV Rules establish the foundation for setting up of registered valuer organisations (RVO). A RVO is a self-regulated organisation (similar to ICAI and ICSI) for imparting educational courses/ training and conducting professional examinations for persons, who aspire to become a registered valuer.

Till date, 11 RVOs have been granted recognition by IBBI and more than 1,000 professionals are enrolled as registered valuers with IBBI under three asset classes.

Impact on the valuation practice:

The valuation services are predominantly provided by chartered accountants and merchant bankers, who issue valuation certificates for compliance purposes under the Companies Act, 2013 and other laws such SEBI Regulations, FEMA Regulations or Income Tax Act. Now, the new registration requirements will also apply to such existing valuers as well, even though they have decades of experience in providing valuation services. Such chartered accountants and merchant bankers will have to get themselves enrolled as a registered valuer if they intend to continue the valuation practice after 31 January 2019.

The partnership firms and companies, who are providing valuation services, will also need to restructure their constitution to fulfil the eligibility criteria set in the RV Rules. For example, a company, which is a subsidiary, joint venture or associate of another company, is not eligible to be a registered valuer. This ineligibility is expected to impact the consultancy or advisory companies/ firms, which are set up as a body corporate.

The RV Rules also empowers the MCA to notify valuation standards to be followed by registered valuers for undertaking valuation. The MCA has constituted a committee to recommend the valuation standards and policies for compliance by companies and registered valuers. But given the need of the hour, the ICAI already established a Valuation Standard Board and formulated ICAI Valuation Standards in June 2018. These ICAI Valuation Standards will remain effective till valuation standards are notified by the MCA.

A registered valuer is now recognised as a professional like a chartered accountant, lawyer and company secretary and is responsible for any negligence or misconduct leading to disciplinary action by IBBI and regulatory penalties and fines.

All these developments are expected to create sea change in the valuation practice and bring governance in the valuer profession in India.

Adoption under other laws:

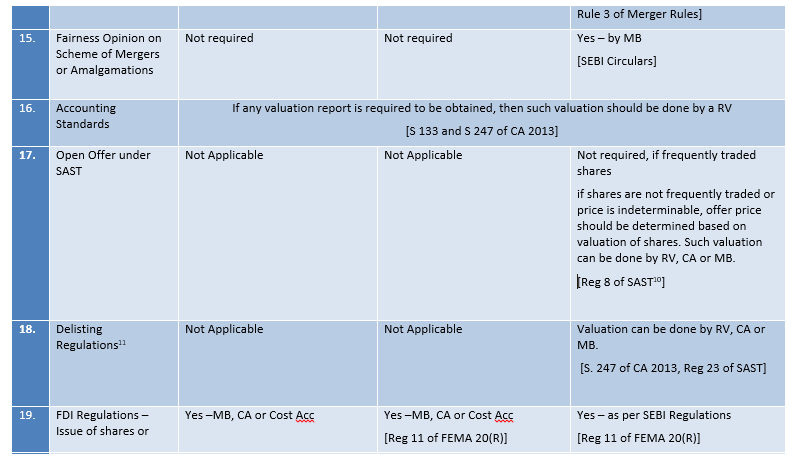

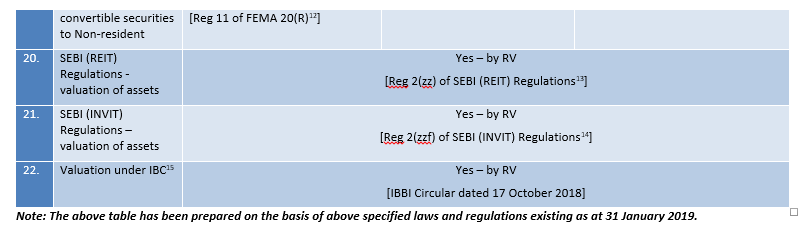

The valuation by a registered valuer applies to valuation of assets, liabilities, shares, etc required under the Companies Act, 2013 and the rules made thereunder. It does not apply to valuations required under other laws, unless the other laws mandate valuation by a registered valuer. On 17 October 2018, IBBI issued a circular stipulating that any valuation required under the Insolvency & Bankruptcy Code, 2016 should be done by a registered valuer with effect from 1 February 2019. Likewise, SEBI has also mandated valuation by a registered valuer under few SEBI regulations.

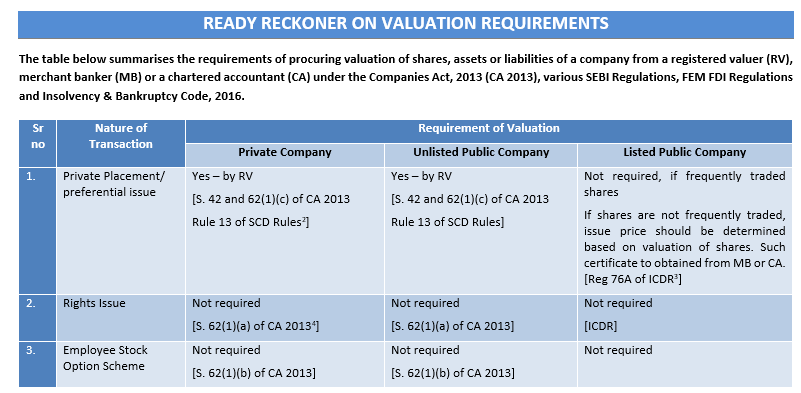

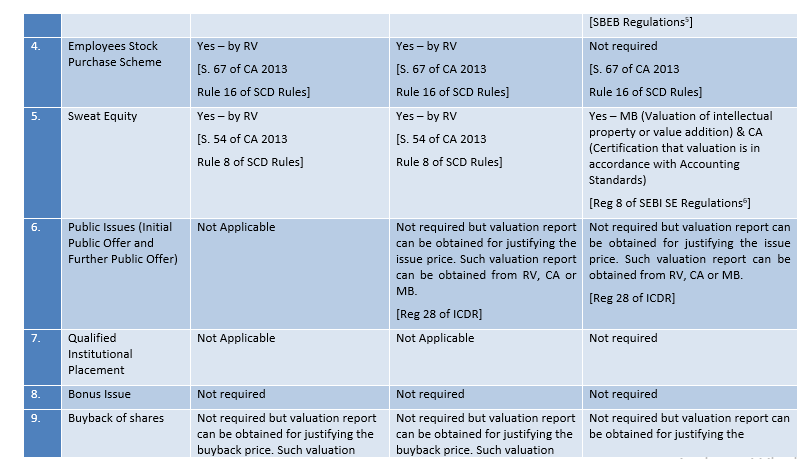

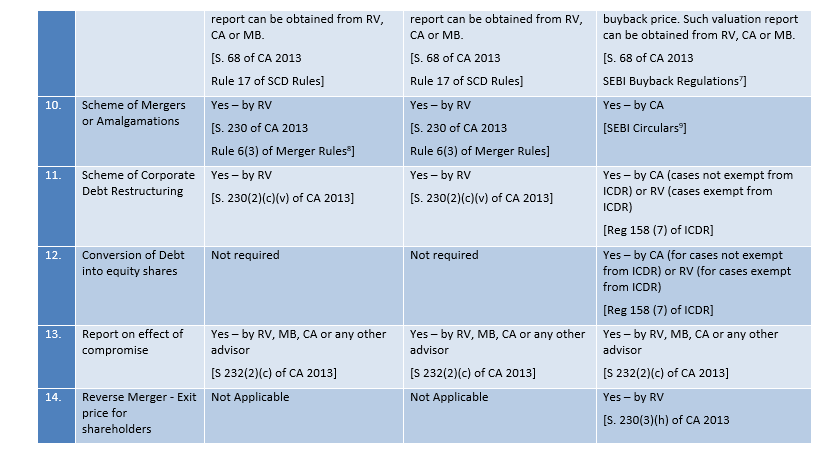

To give the gist of the valuation requirements under various laws, a ready reckoner is populated in the table below for easy reference.