Turkey introduced Digital Service Tax, Accommodation Tax, Luxury Residence Tax for the first time in the history, changed income tax tariffs and brought restrictions on company car expenses and some other important amendments under the law numbered 7194 which was published on the official gazette dated December 7, 2019 (the "Law").

1. Digital Service Tax

A new tax called the "Digital Service Tax" ("DST") will be applicable to the revenue generated from Turkish users from advertising services on digital interfaces; services offered in the digital environment for listening to, viewing, playing or recording on electronic devices of audio, visual or any digital content and their sale on a digital basis, and services which allow users to interact with others, including for the delivery of goods or services between users which will be effective from April 1,2020.

The DST will be applied at 7.5% on the revenue generated by service providers. The law grants the President the authority to decrease the tax down to 1% and increase the tax rate up to two times the 7.5%.

In case the service provider does not have a fixed place of business or permanent representative in Turkey, such tax will be declared and paid by the parties who act as intermediary for the service provider's services. As a result, the revenues generated from digital services by Turkish residents and nonresidents will be in the scope of this taxation provided that those revenues are generated from Turkish activities.

However, a tax exemption is provided for service providers inside and outside of Turkey if (i) the service provider generates less than 20 million Turkish Lira revenue from Turkey or (ii) the service provider's worldwide revenues are less than 750 million Euros. The President has the authority to increase the thresholds up to three fold and reduce to zero.

DST will be declared and paid on a monthly basis.

The following services are exempt from DST: (i) the services that GSM companies pays treasury fees out from it, (ii) the services that are subject to Special Communication Tax, (iii) services that in the scope of Banking Law, (iv) sale of products produced by a research and development activity in R&D Centers, and (v) services subject to Payment Services and Electronic Money Institutions Law.

2. Accommodation Tax

Accommodation services provided at hotels, motels, holiday villages, pensions, and other accommodation places and other services such as eating, drinking, entertainment and use of the pool, beach, thermal and similar services provided within such accommodation places will be subject to a 2% Accommodation Tax effective from April 1, 2020.

The law gives the President the authority to decrease the tax down to 1% and increase the tax rate up to 4%.

The accommodation tax will be declared on a monthly basis. The monthly tax declaration will be made and paid until 26th of the following month.

The Accommodation Tax will not be included into the VAT base.

3. Banking and Insurance Transaction Tax ("BITT") Rate on Foreign Exchange Transactions

The BITT rate to be imposed to foreign exchange transactions has been increased from 0.1% to 0.2% to be effective as of December 7, 2019. In addition, the President is authorized to increase the BITT rate on foreign exchange transactions up to tenfold.

4. Restriction regarding Company Car Expenses

The Law introduces some restrictions on expenses incurred for the acquisition of company cars, amortization, maintenance and leasing expenses pursuant to the amendment to the Income Tax Law which will become effective as of January 1, 2020. The restrictions are as follows:

a) Leasing payments up to 5,500 Turkish Lira for company car can be deducted from income or corporate tax base;

b) Sums up to 115,000 Turkish Lira of special consumption tax and value-added taxes paid for the acquisition of company cars can be deducted from income or corporate tax base;

c) 70% of the repair, maintenance and other expenses related to company cars can be deducted from the income or corporate tax base; and

d) Amortization expense of the purchase price of each company car (excluding special consumption tax and VAT) up to up to TL 135,000 can be deducted from the tax base. In case the company cars are acquired as second hand (special consumption tax and VAT is included into the acquisition price); the acquisition value up to TL 250,000 will be subject to tax-deductible amortization expense.

5. Changes in Income Tax Rates and Taxation of Wages

a) Changes in Income Tax Tariff

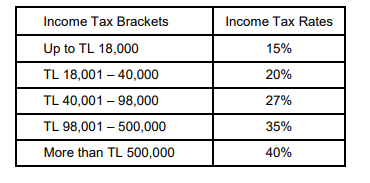

Effective from January 1, 2019, a new tax rate of 40% is introduced for the annual income exceeding TL 500,000 and income tax brackets increased from four to five.

With regard to wage incomes, the new tariff will be effective from January 1, 2020.

The new regulation determines the income tax tariff to be applied to the incomes other than wage income earned in 2019 as follows:

b) Changes in Taxation of Wage Incomes

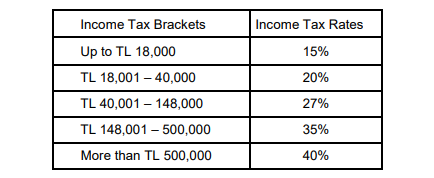

As of January 1, 2020, wage incomes exceeding the fourth tax bracket will be subject to a 40% income tax. The below stated income tax tariff will be updated in 2020 and be applicable to the salary income:

Before the amendment of the Law, employees who earn wage income only from a single employer in a calendar year were not subject to annual income tax return submission. With the new regulation, employees with more than TL 500,000 gross wage income in 2020 and onward must submit annual income tax return even if the income is obtained from a single employer.

The existing annual income tax submission obligation for those who earn wage income from more than one employer due to job change or other reason continue still continues if the wage income obtained from the second employee exceeds the second bracket of the income tax tariff in a calendar.

6. Luxury Residence Tax

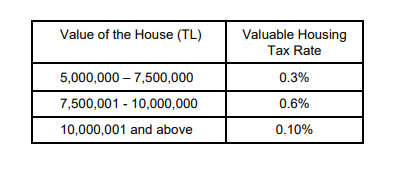

Luxury residences will be subject to Luxury Residence Tax effective from 2020 if the either value determined by the General Directorate of Land Registry and Cadaster or the value determined for the real estate tax exceeds TL 5,000,000. The luxury residences will be subject to below stated tax tariff:

The Luxury Residence Tax is declared until 20th February of the year following in which the residence becomes taxable. The calculated tax is paid in two equal installments in February and August of the relevant year.