Foreign direct investment (FDI) into China has slowed over the past several years. The country logged US$10 billion of inbound FDI in September, down by more than a third compared to September 2022 and the fourth consecutive month of double-digit declines.

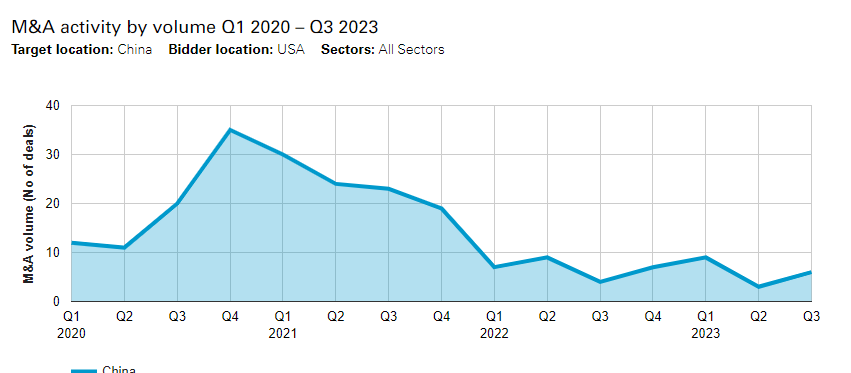

Inbound M&A figures reflect this subdued reality, with the volume of bids for Chinese assets led by US dealmakers trending down conspicuously since Q4 2020, when 35 such transactions were announced—at the time, the highest quarterly sum in nearly a decade.

By contrast, there were 18 US outbound M&A deals targeting Chinese assets announced through the first three quarters of 2023, down 10 percent from the same period in 2022 and representing a precipitous decline of 76.6 percent from Q1 to Q3 2021.

Effective July 1, 2023, the underlying Mergermarket data supporting the M&A Explorer was consolidated with Dealogic data to produce an even more complete picture of the M&A marketplace. M&A Explorer commentary published before July 1, 2023 may reference data that does not reflect this consolidation.

For more details on the criteria behind deal inclusion, click here.

As China’s labor costs rise, global investment flows are rerouting to Southeast Asian countries such as Vietnam, Indonesia and Thailand, and some companies are reshoring their manufacturing capacity. Meanwhile, the Biden administration announced further restrictions in August on US investment in China’s quantum computing, advanced chips and AI sectors.

With these factors in the backdrop, US dealmakers are pivoting some of their transactions away from China and toward Japan and South Korea, both advanced economies with which the US has enjoyed strong bilateral relations for decades.

TMT, business services and healthcare lead the way

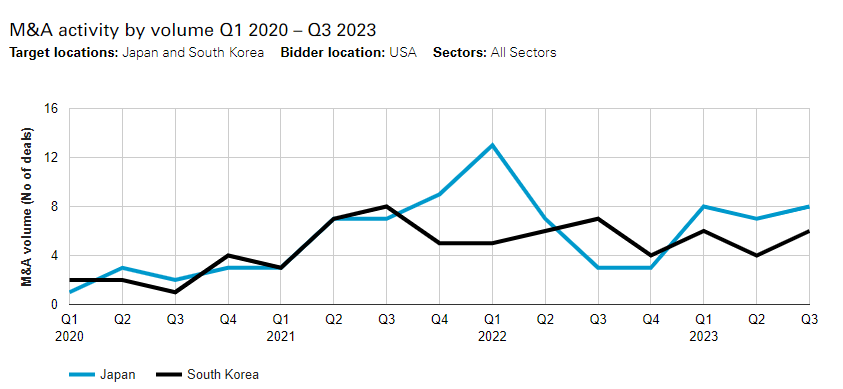

The volume of US outbound M&A into Japan and South Korea has trended up for the last few years, albeit from a low base. In 2020 US bidders targeted a total of 18 assets in these nations, rising to 49 in 2021 and 48 in 2022. Through the first three quarters of this year, US dealmakers targeted 16 South Korean and 23 Japanese assets, versus 18 instances of US originated M&A transactions into China—the first time since 2016 that volume in Japan surpassed that of China.

If the market keeps up the pace, approximately 50 US-led deals will have been announced in Japan and South Korea by the end of this year, with the bulk coming in the TMT and business services sectors, which have seen 12 and 11 deals, respectively, in the last three quarters.

The largest of these transactions, worth an estimated US$1.2 billion, saw Hawaii-based and NASDAQ-listed Pono Capital Two—a special purpose acquisition company—and SBC Medical Group announce a definitive merger agreement. SBC, headquartered in Tokyo, is a marketing consultancy for medical companies, focusing on cosmetic surgery, infertility treatment, dental work and orthopedics.

The biggest US-South Korean deal announced so far in 2023 also relates to healthcare services. In May, Minnesota-based Medtronic moved to acquire EOFlow, a Seoul-based company that manufactures tubeless, disposable insulin pumps fitted to patches, for US$738 million.

With the EOFlow deal set to close in late 2023 and having received federal approval for its MiniMed 780G insulin pump in April, Medtronic is better placed to compete with companies such as Insulet and Tandem Diabetes Care in the hotly contested US diabetes treatment market. According to Mergermarket, Medtronic is the only one of these companies to have struck deals in Asia. Its three previous transactions in the region, from 2021, 2012 and 2008, all concerned Chinese assets, meaning its pivot to Korea could prove illustrative of a sea change in US outbound M&A into the region.

Discover Japan

In Q2 2023, Japan’s Ministry of Economy, Trade and Industry published a series of case studies citing accelerated corporate growth, improved management know-how, and expanded global sales channels as key benefits of cross-border dealmaking. In the studies, Japanese parties to recent deals explicitly commended the business input of multiple US investment firms, including KKR, Bain Capital and the Carlyle Group.

To date this year, KKR has struck four deals in Japan and South Korea, Bain five, and Carlyle two. The largest of these was KKR’s acquisition, with Hong Kong-based Gaw Capital, of the Hyatt Regency Tokyo in March for around US$1 billion—the US firm’s first hotel asset in Japan. The seller, Odakyu Electric Railway, divested itself of this non-core asset after coming under significant pressure during the pandemic due to the sharp fall in commuter traffic.

International investment in Japan’s hotel and hospitality space has boomed in recent years. Blackrock, for instance, acquired eight hotels and resorts around the country in early 2021, also from a railway group—Kintetsu Group Holdings—that was contending with the pandemic-induced impact of declining rail passenger numbers. Besides operating train stations, rail groups in Japan typically own prime retail and office assets in and around these transport hubs, which international PE firms with substantial dry powder, such as Blackrock and KKR, may continue to eye.

According to MSCI Real Assets, foreign investors have spent at least US$2 billion on hotel deals in Japan in 2023, easily eclipsing the US$1.4 billion they expended across 2022 and accounting for the most investment across all Asian commercial property sectors. According to Japan National Tourism Organization, after Japan lifted the last of its COVID-19 travel restrictions in May 2023, the country welcomed almost 2.2 million international travelers in August—an increase of more than 1,000 percent compared to August 2022. Further, a relatively weak yen is one of many selling points to tourists and inbound strategic business acquirers alike.