The new law on Investment was promulgated on 15 October 2021 by virtue of Royal Kram No. NS/RKM/1021/014 ("Law on Investment") on an urgent basis and has been in force since 16 October 2021 throughout the country. The Law on Investment abrogates the old Law on Investment dated 5 August 1994 and its amendment dated 24 March 2003.

The Law on Investment consists of 12 chapters and 42 articles, and applies to all qualified investment projects ("QIPs"), expanded QIPs and guaranteed investment projects (collectively referred to as "Investment Projects") registered with the Council for the Development of Cambodia ("CDC") or the Provincial-Municipal Investment Sub-Committees ("Sub-Committees").

In this Update, we highlight the key features of Cambodia's new Law on Investment.

- Online Registration of Investment Projects

A person, including an individual and a legal entity, that intends to implement an Investment Project must submit online an application to CDC or the Sub-Committees via this link to the information technology platform. CDC or the Sub-Committees will issue a registration certificate ("Registration Certificate") within 20 working days if such proposed investment project is not listed in the "negative list" of prohibited or restricted business lines or sectors.

The Registration Certificate will be tied to a bar code or QR code, or other technology system that provides primary information in relation to the registered investment project. After obtaining the Registration Certificate, the investment project will be implemented automatically. The successful applicant is not exempted from obtaining other applicable permits in relation to the investment project.

- Certain Sectors and Investment Activities that are entitled to Investment Incentives

Any person whose sector/investment activity is certified as a QIP and not listed in the "negative list" are eligible to obtain basic tax and/or customs duties incentives in whole or in part. The sectors and investment activities that are eligible for investment incentives include:

- High-tech industries involving innovation or research and development;

- Innovative or highly competitive new industries or manufacturing with high added value;

- Industries supplying regional and global production chains;

- Industries supporting agriculture, tourism, manufacturing, regional and global production chains and supply chains;

- Electrical and electronic industries;

- Spare parts, assembly and installation industries;

- Mechanical and machinery industries;

- Agriculture, agro-industry, agro-processing industry and food processing industries serving the domestic market or export;

- Small and medium-sized enterprises in priority sectors and small and medium-sized enterprise cluster development, industrial parks, and science, technology and innovation parks;

- Tourism and tourism-related activities;

- Special economic zones;

- Digital industries;

- Education, vocational training and productivity promotion;

- Health;

- Physical infrastructure;

- Logistics;

- Environmental management and protection, and biodiversity conservation and the circular economy;

- Green energy, technology contributing to climate change adaptation and mitigation; and

- Other sectors and investment activities not listed above but are deemed to have potential for socio-economic development by the Royal Government of Cambodia.

- Types of Investment Incentives

An investment project registered as a QIP is entitled to basic incentives and additional incentives. Special incentives are also granted in specific circumstances.

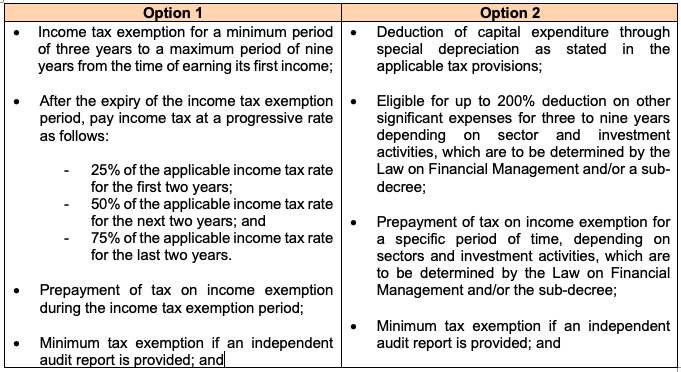

Basic Incentives

Any QIP is entitled to either of the two basic incentives below.

In addition to the above basic incentives:

- Export QIPs and Supporting Industry QIPs are entitled to customs duty, special tax and value-added tax ("VAT") exemptions for the import of construction materials, construction equipment, production equipment and production inputs.

- Domestically-oriented QIPs are entitled to customs duty, special tax and VAT exemptions for the import of construction materials, construction equipment, and production equipment. However, a domestically- oriented QIP’s incentives for production inputs is to be determined by the Law on Financial Management and/or the sub-decree.

Additional Incentives

In addition to the basic incentives provided above, a QIP also receives:

- VAT exemption for purchases of locally-produced production inputs for the implementation of the QIP; and

- Deduction of 150% from the tax base for any of following activities:

- Research, development and innovation;

- Human resource development through the provision of vocational training and skills to Cambodian workers/employees;

- Construction of accommodation, canteens or food courts where reasonably priced foods are sold, nurseries and other facilities for workers/employees;

- Upgrading of machinery to serve the production line; and

- Provision of welfare for Cambodian workers/employees such as: (i) comfortable means of transportation to enable the workers/employees to commute from their homes to the factories; (ii) accommodation; (iii) food courts or canteens where foods are sold at reasonable prices; (iv) nurseries; and (v) other facilities.

QIPs that have obtained income tax exemption approved by CDC before the enforcement of the Law on Investment are still entitled to its remaining income tax exemption period.

Special Incentives

Special incentives are granted to any sector/ investment activity that have high potential for national economic development. The special incentives are determined by the Law on Financial Management.

QIPs in Special Economic Zones

QIPs located in special economic zones are entitled to the same investment incentives, guarantees and protections as other QIPs.

- Investment Guarantees and Protection

The investors are protected from nationalisation and expropriation which may affect their assets or approved Investment Projects.

The investors have the right to freely purchase foreign currencies and repatriate these foreign currencies to settle financial obligations associated with their investments through authorised intermediary banks, in accordance with applicable laws and regulations. The transfers include:

- Capital contributions including initial capital contributions;

- Income, capital gains, dividends, royalties, license fees, management and technical assistance fees, interest and other income from investments;

- Income from total or partial sale or dissolution of the company implementing the Investment Project;

- Payment of import and repatriation of both principal and interest of the loan;

- Payment of compensation in case of civil disturbance, expropriation or confiscation by the State;

- Payment arising from the settlement of a dispute by any means including court decisions or arbitration awards; and

- Income and salary of employees.

The investors’ intellectual property is protected in accordance with the applicable laws and regulations in Cambodia.

- Miscellaneous

The Law on Investment also includes provisions concerning:

- the acquisition, sale or merger of investment projects;

- the nullification of investment projects; and

- reconciliation as a mode of resolving disputes between the investors involved in Investment Projects.

If you have any queries on the above, please feel free to contact our team members below who will be happy to assist.