Employee Share Schemes (ESS) are used by high growth companies to attract, retain and motivate staff by aligning their interests with founders and institutional investors.

These equity schemes have historically been subject to complex regulation, which made them difficult and costly to implement. Fortunately, the Federal Parliament has passed long overdue amendments to the tax rules relating to ESS interests as well as other changes to remove regulatory barriers to establishing Employee Share Schemes.

The changes are important for high growth companies and their investors as they provide:

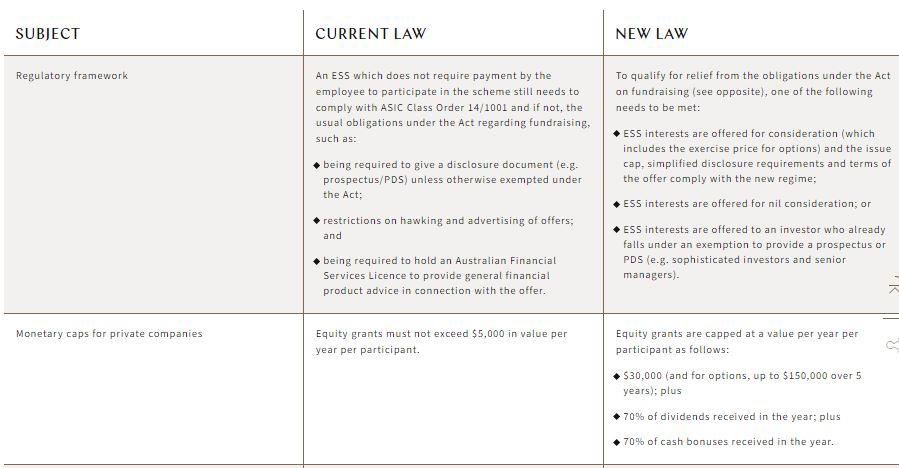

- the ability to offer of more meaningful amounts of equity with a new maximum cap of $30,000 per year per participant (up from $5,000 per year currently);

- relaxed disclosure and regulatory requirements;

- a broader pool of participants who may be offered equity; and

- a simplified regulatory regime where the equity is offered at no cost to the participant.

Changes to extend corporate law relief

Parliament has recently passed amendments to remove the regulatory barriers in offering Employee Share Schemes under the Corporations Act 2001 (Cth) (Act). These changes aim to make it easier to establish an Employee Share Scheme compared to the current regulatory regime under ASIC Class Orders 14/1000 and 14/1001. These changes take effect on 1 October 2022.

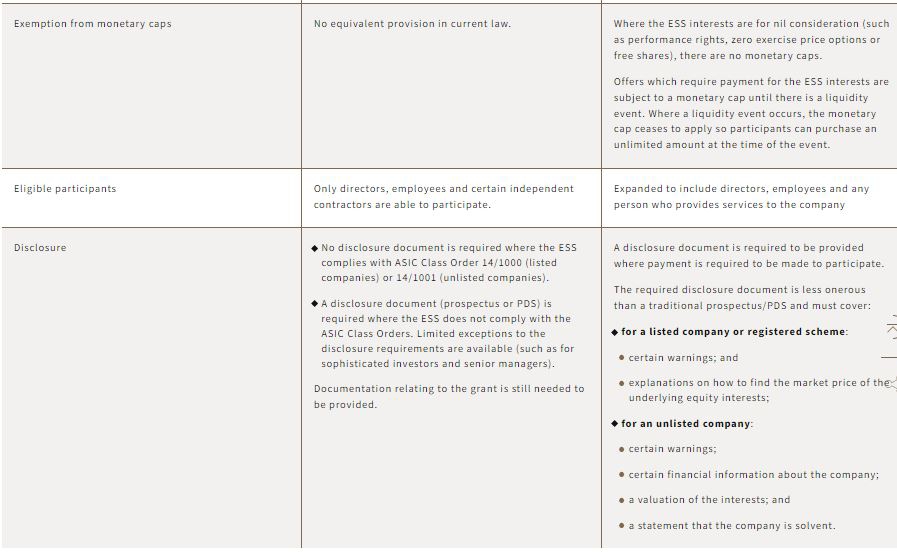

The key aspects of the changes are summarised in the table below.

Tax changes

Changes to the tax rules governing Employee Share Schemes have been passed in Parliament (which commence on 1 July 2022) to remove the taxing point when a holder ceases employment. Prior to these changes, employees would usually have to sell their ESS interests (such as options) to fund the tax payable on the original equity grant. The changes will apply for taxing points which occur after 1 July 2022, so employees with grants received before 1 July 2022 are able to take advantage of the changes. More detail on these changes can be found here.

Where to from here?

The amendments to the ESS rules are welcome and provide flexibility for start-ups and scale-ups to offer more meaningful amounts of equity with simpler legal obligations. It is a dramatic change to the current regime which has been too rigid from a regulatory perspective to allow equity grants to a broad range of employees, directors and other service providers. The current $5,000 cap and requirement to provide a disclosure document (unless limited exceptions were met) often resulted in the exclusion of more junior employees from these equity plans.

As most early-stage businesses are cash intensive, finding and attracting talented individuals is difficult without generous equity grants. The amendments are likely to make this less challenging.